- Member Newsletter

- News Centre

- Pay Your Fees

This website uses cookies. For more information, click here .

Municipal and Regional District Tax

The Municipal and Regional District Tax (MRDT) is a tax of up to three per cent (3%) on the purchase of short-term tourist accommodation imposed in specific geographic areas of British Columbia (designated accommodation areas) on behalf of municipalities, regional districts or eligible entities.

The MRDT program – sometimes referred to as the Hotel Tax - was originally introduced by the Provincial Government in 1987 to raise revenues for local tourism marketing, programs, and projects. MRDT is paid by visitors (not residents or Members) when they book accommodation and it is collected by the accommodation sector.

In Whistler, the MRDT funds are received by the Resort Municipality of Whistler (RMOW) and then shared with Tourism Whistler based on a number of agreements. Revenues are reinvested by both organizations on behalf of the destination. Expenditures are approved by, and reported back to, the Province to ensure ongoing alignment with the prescribed purposes of the tax as outlined in the Provincial Sales Tax Act.

More information about how MRDT is collected and invested in Whistler is available on the RMOW’s website at whistler.ca/mrdt .

- Review the 2023-2027 MRDT Whistler Five-Year Strategic Plan

- Review the 2018-2022 MRDT Whistler Five-Year Strategic Plan

Additional information about the provincial MRDT program is available on Destination BC’s website .

How are the MRDT funds spent in Whistler?

In Whistler, the MRDT funds are primarily invested into a mix of product reinvestment and enhancement, service delivery and leisure marketing and sales initiatives. Investment examples in 2022 include:

Marketing Campaigns

- Summer 2022 Golf Campaign

- Festival & Events Campaign (e.g. Gran Fondo, Cornucopia, Whistler Film Festival)

Conference Centre Initiatives

- Attendance at industry-related events

- Execution of familiarization trips for meeting planners

- Targeted sales initiatives directed at filling midweek and shoulder season periods

Investment in Affordable Housing Initiatives

- Construction of employee-restricted housing in Cheakamus Crossing

Planning, Investing & Development of Whistler

- Park and amenity upkeep and signage

- Valley Trail enhancements and connections

- Parks Masterplan Project

- Bylaw support and Goose Management

- Investments in third-party festivals and events

Investment in the Workforce Who Deliver the Visitor Experience

- Village Host Program

- Whistler Experience Guest Service Training (in partnership with the Whistler Chamber of Commerce)

- Visitor Information Centre Support

- Park and Trail Ambassador Program

- About Tourism Whistler

- Manage Your Membership

- Member Tools & Resources

- Visitor Servicing

- Research & Insights

- Whistler Inside Scoop

- Health & Safety Information

- Value of Tourism

- Whistler's Place Brand

- Destination Stewardship

- Planning, Strategy & Results

- Board of Directors

- Annual General Meeting

- Corporate Documents

- Membership Overview

- Become A Member

- Pay Membership Fees

- Maintain Your Business Listing

- List Your Rental Property

- Member Forms

- Fee Information Request

- Real Estate & Clients

- Underused Housing Tax

- Member Opportunities

- Member Meetings

- Seasonal Marketing Campaigns

- Promotional Tools

- Messaging Toolkits

- Business Planning

- Destination Experience & Opportunities

- Emergency Preparedness

- Submit Member Feedback

- Visitor Servicing Information

- Whistler Business Directory

- Online Interactive Map

- Ask Whistler

- Go Whistler Tours

- Submit Visitor Feedback

- Research Overview

- Performance & Forecasting Data

- Survey & Visitor Insights

- Wine Program

- Local Flavours Program

- Outdoor Trail Guide

- Meetings & Conferences Sales

- Arts & Culture Program

- Digital Display Advertising

- Visitor Centre Display Advertising

- Brochure Racking

- Monthly Newsletter Sponsored Placement

- Online Advertising

- Relocation Guide

- How Can You Participate?

- Biosphere Committed Businesses

- Safety & Emergency Preparedness

- Partner Portal Login

- Digital Assets Requests

- Subscribe to Receive Updates

- Report to the Community

- Tourism Research

- Virtual Backgrounds

- Economic Sector Strategy

- Cycle & Savour

- Wine & Culinary

- Wellness & Outdoor

- Meetings Facilities

- Quick Facts

- Virtual Experiences

- #meetinKelowna Blog

- Accommodations

- Transportation Services

- Weddings & Events

- Wine & Food Tours

- Outdoor Itineraries

- Urban Adventures

- Family Itineraries

- Meetings & Groups

- Arts & Culture

- Familiarization Tours

- Promo Video

- Kelowna Photos

- Virtual Destination Showcase

- Sports Facilities

- How We Can Help

- 2025 Montana's Brier

- Media Requests

- Work With Us

- Story Ideas

- Hosting Policy

- Writer Application Form

- Non-Local Creators

- Local Creators

- Creator Guidelines

- Photo & Video Requests

- About Kelowna & Region

- Destination Copy

- #exploreKelowna Blog

- Events Calendar

- Indigenous Heritage

- #exploreKelowna Creators

- Realtors & Services

- Value of Tourism

- Visitor Centre

- Volunteer with Tourism Kelowna

- Board of Directors

- Destination Development

- Sustainability Indicators

- Online Retail Store

- Events Happening Today

- Events Happening this Weekend

- Submit an Event

- Subscribe to our Newsletters

- Spring Break in Kelowna

- Why Spring is a Great Time to Visit Kelowna

- Blossoms in Kelowna

- Why Spring Wine Touring in Kelowna is Incredible

- Golf Couples Getaway

- Spring Hikes to Check Out

- 5 Ways to Enjoy Summer in Kelowna

- Family-Friendly Activities to Add to Your Summer Checklist

- Fruit Picking

- Must Visit Restaurant Patios

- Loving Lake Life with the Family

- Perfect Long Weekend Itinerary

- Meet me on Bernard

- Ultimate Kelowna Itinerary for Your Summer Road Trip

- Why Fall Wine Touring is the Best

- Taste Kelowna's Fall Bounty

- Fall Hiking

- Multi-day Itinerary to Build Your Own Adventure

- Golden Larch Season is a Photographer's Dream

- Family Fall Adventures

- Delectable Farm-to-Table Restaurants

- Valentine's Day

- Family Day Weekend

- Hiking & Snowshoeing

- Nordic Skiing

- Ski Resorts

- Winter in Wine Country

- Winter Weekend in Kelowna with Kids

- Winter Holidays

- Local Flavours

- Attractions

- Festivals & Associations

- Galleries & Studios

- Movie Theatres

- Performing Arts

- Uptown Rutland Murals Pass

- 10 Family Friendly Activities

- Spending a Day at the Lake with the Kids

- Indoor Activities with Kids

- 48 Hours in Kelowna for Families

- Farm to Table Tours

- Blossom & Harvest Dates

- Local Flavours Pass

- Golf Courses

- Build Your Golf Packages

- Off The Course

- Golf Events

- Golf Kelowna Guide

- Guided Wine Tours

- Guided Tours

- Health & Beauty

- Urban Adventure

- Bike Rentals & Services

- All Biking Trails

- Crawford Trails

- Rose Valley Regional Park

- Dog Friendly Patios

- All Hiking Trails

- Family Hikes

- Picnic Hikes

- Spring Hikes

- Waterfall Hikes

- Winter Hikes

- Beaches & Parks

- Boating & Marinas

- Boat Launches

- Kelowna Paddle Trail

- Scuba Diving

- Motorbiking

- Myra Canyon Trestles

- Okanagan Rail Trail

- Rock Climbing & Bouldering

- All Wineries

- Dog Friendly Wineries

- Tour by Glass

- Wine Touring 101

- Kelowna Wineries

- West Kelowna Wineries

- Lake Country Wineries

- All Restaurants

- Delicious Desserts

- Farm to Table Dining

- Food Trucks

- Local Favourites

- Vegan Dining

- All Craft Beverages

- Distilleries in Kelowna

- What Makes Okanagan Cider So Special

- Local Flavours & Wine Trails Passes

- Packages & Promotions

- Hotels, Motels & Resorts

- B&B & Specialty Lodging

- Cabins & Cottages

- Vacation Rentals

- Camping & RV Parks

- Dog-Friendly Accommodations

- Current Conditions

- About Kelowna

- Downtown Kelowna

- Kelowna's North End

- Pandosy Village

- West Kelowna

- Westbank First Nation

- Lake Country

- Farms & Orchards

- Land as Heritage and Home

- Historic Sites

- Historic Westside Road

- Interesting Facts

- Electric Car Charging Stations

- Kelowna Maps

- Public Transit

- Transportation

- Public Restrooms

- Wine & Food

- Family Friendly Accessible Adventures

- Adaptive Ski & Snowboard Lessons

- Tips for Enjoying Kelowna Responsibly

- Wellness Travel

- Outdoor Safety

- Lake & Boating Safety

- Ways to Explore Safely in Kelowna

- COVID Health & Safety Information

- Laws & Regulations

- Currency & Taxes

- Gratuities & Tipping

- Entry Regulations

- Visitor Guide

- Family Friendly Itinerary

- Wine & Food Itinerary

- Urban Adventure Itinerary

- Golf Kelowna Itinerary

- Build Your Own Itinerary

- Additional Resources

- Blog Homepage

- Latest Blog Posts

- Membership & Advertising

- Marketing Programs

- Additional Opportunities

- Biosphere Commitment Program

- Industry News Centre

- Meetings & Conferences

- Incentive Travel

- Travel Trade

- Sports & Events

- Content Creators & Influencers

- Media Resources

- Relocation Information

- Hotel Guest Tax (MRDT) Information

Municipal & Regional District Tax (MRDT)

Frequently asked questions, what is the municipal & regional district tax or mrdt.

The Municipal and Regional District Tax program (MRDT) is a provincial program jointly administered by the BC Ministry of Finance, BC Ministry of Tourism, Arts & Culture and Destination BC, the crown corporation providing tourism services for the province.

The MRDT is an accommodation tax collected under the provincial sales tax legislation to fund tourism marketing, programs and projects. Agreements between the province and communities are for 5-year terms.

What is the current tax rate?

In Kelowna, the MRDT tax level is 3% of gross room sales. It is collected by the accommodators and remitted with their Provincial Sales Tax to the Ministry of Finance.

How are the funds used?

MRDT revenue remitted by Kelowna hotels is allocated to Tourism Kelowna for destination marketing; MRDT revenue remitted by Kelowna Short Term Rentals (STRs) is allocated to help address the city’s affordable housing issues.

MRDT funds are intended to augment current funding and cannot be used to replace existing sources of funding in a community such as annual grants.

What role does the City of Kelowna play in the collection and allocation of MRDT?

The City of Kelowna is the “designated recipient” of the MRDT funds , the city is the applicant , the agreement holder with the province and is ultimately responsible for all compliance and reporting requirements. Kelowna’s current MRDT agreement with the province is for 2022- 2026.

What role does Tourism Kelowna play in the collection and allocation of MRDT?

Tourism Kelowna is the “eligible entity”, Tourism Kelowna is the service provider, administering the MRDT funds on behalf of the City of Kelowna to deliver tourism marketing, programs and projects. Tourism Kelowna also provides the city with the annual strategic plan, tactical plan, performance report and financial reports required under the MRDT agreement.

What does Kelowna contribute to the Tourism Events Program (TEP)?

The province holds back a small percentage of the remitted tax for administration costs in addition to 2% to fund the provincial Tourism Events Program, a funding source to help communities attract new, major events to the province.

How much revenue is collected?

In Kelowna, MRDT revenue makes up approximately 60% of Tourism Kelowna’s total annual budget. In 2019, $2.8M in MRDT was collected.

- Privacy Policy

English | Français

Tourism Kelowna would like to thank Westbank First Nation and Okanagan Indian Band for the privilege to live, work, and play on the tm̓xʷúlaʔxʷ (land), that is the unceded and traditional territory of syilx Okanagan peoples, the original stewards of these lands and to whom we give thanks to as our hosts

Kelowna Visitor Centre:

238 Queensway

Kelowna, B.C. V1Y 6S4 Canada

1-800-663-4345

© 2024 Tourism Kelowna

BC Government News: Additional Major Events Municipal and Regional District Tax (MRDT) Consultation

Details from the BC Government news release:

A new Major Events Municipal and Regional District Tax (MRDT) of up to 2.5% on short-term accommodation sales may be available to communities.

The purpose of this tax is to help cover the cost of planning, staging and hosting eligible major international tourism events that generate significant international visitation and help bolster provincial tourism and the economy. The Major Events MRDT program applies to:

- Municipalities

- Regional districts, and

- Eligible entities (non-profit organizations actively engaged in tourism marketing, programs or projects, or affordable housing initiatives)

Under the Provincial Sales Tax Act, there are certain requirements to be eligible for the Major Events MRDT, namely:

- The Minister of Finance is satisfied that there is to be a major international tourism event intended to generate significant international visitation and help bolster provincial tourism and the economy in or near the proposed designated major event accommodation area; and

- The Minister charged with the administration of the Tourism Act has, on behalf of the government, entered into an agreement with the municipality, regional district or eligible entity respecting the tax.

The province is currently developing the program requirements and application process that will be applicable to the new Major Events MRDT program, namely:

- Defining what is an eligible major international tourism event

- How the revenues can be spent, and

- Reporting requirements

The program requirements and application process will be developed by the Ministry of Finance, Ministry of Tourism, Arts, Culture and Sport, and Destination BC in consultation with local governments and the tourism and accommodation industry.

Learn more and read the full government program details : https://www2.gov.bc.ca/gov/content/taxes/tax-updates/spotlight-on-tax-and-benefit-programs/additional-major-events-mrdt-consultation

Destination BC

Official websites.

HelloBC.com

Be inspired to start planning your BC Vacation.

Travel Media

Information for journalists, editors and broadcasters.

Tourism Business Portal

Online, self-service business listings system for tourism industry.

Subscribe to our newsletter

- Meetings & Conventions

- Travel Trade

(0) items in your itinerary

Vancouver's Tax & Fee Structure

- Helpful Tips & Resources

- Vancouver's Tax Structure

Vancouver's Tax & Fee Structure

Tax on short-term accomodation in vancouver.

Short-term accommodation in the City of Vancouver includes hotels, as well as to Airbnb, VRBO and all online marketplace facilitators.

The total rate in Vancouver (as of February 2023) is 20% of the room rate, consisting of:

8% Provincial Sales Tax (PST)

3% Municipal & Regional District Tax (MRDT), which most major cities in BC collect.

2.5% Major Event MRDT. On Feb 1, 2023, a temporary Major Events MRDT over seven years was introduced and in effect until Jan 31, 2030.

1.5% Destination Marketing Fee (DMF) . Most downtown Vancouver hotels collect this fee to assist with the marketing of Vancouver as a destination.

5% Goods & Services Tax (GST) on the total purchase price

Airbnb, VRBO and all online marketplace facilitators

2.5% Major Event MRDT. On Feb 1, 2023, a temporary Major Events MRDT over seven years was introduced and in effect until Jan 31, 2030.

Additional charges may include guest services fees and guest cleaning fees.

SALES TAX IN BRITISH COLUMBIA

Most goods and services in British Columbia are subject to a sales tax totaling 12% of the purchase price (7% PST + 5% GST). Please note that alcohol is taxed at 15% (10% PST + 5% GST).

visit gov.bc.ca for more information [link to https://www2.gov.bc.ca/gov/content/taxes]

Customs Brokers

Visa and entry requirements, weather in vancouver.

Municipal and Regional District Tax

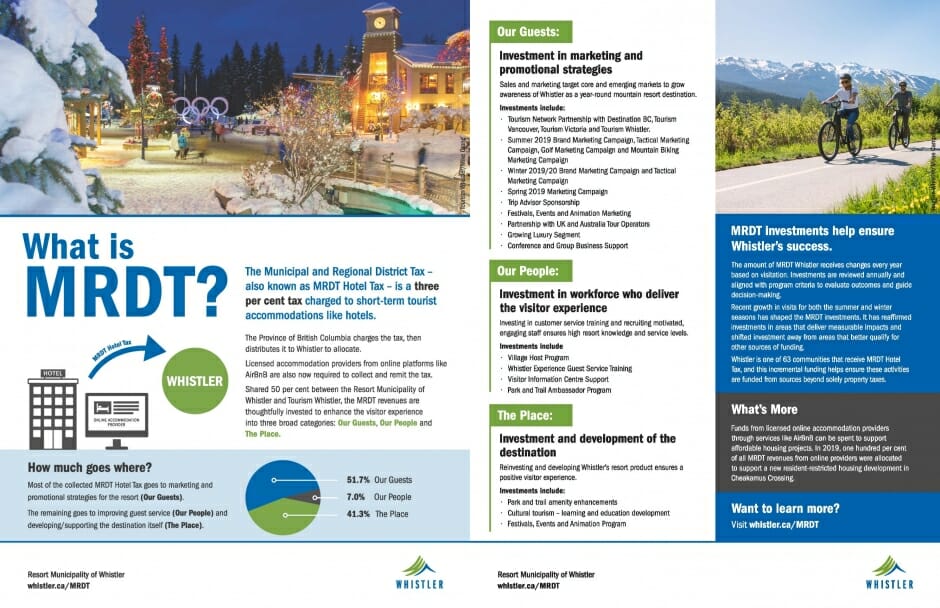

MRDT – also known as Hotel Tax – applies to short-term tourist accommodation, including hotel rooms. This 3% hotel tax is in addition to the eight per cent Provincial Sales Tax (PST).

The MRDT tax program was originally established by the Province in 1987 to support the financing and operations of incremental tourist related facilities as well as ongoing funding of tourism marketing and associated programs.

In Whistler, MRDT revenues are received by the RMOW and shared equally with Tourism Whistler based on a number of agreements. Revenues are reinvested by both organizations on behalf of the community. Expenditures are approved by, and reported back to, the Province to ensure ongoing alignment with the prescribed purposes of the tax as outlined in the Provincial Sales Tax Act.

In 2021, the RMOW’s share was budgeted for $2.6 million. These funds are leveraged to enhance the tourism experience and encourage travel in shoulder seasons and mid-week.

MRDT (along with the Resort Municipality Initiative ) has been critical for Whistler to supplement property tax revenues and ensure a revenue stream directly from, and reinvested back into, the tourism economy.

Increase to three per cent

The Province of B.C. increased the amount of MRDT that Whistler receives from two to three per cent on November 2018.

Changes to online accommodation

Airbnb and other online accommodation providers are legally required to submit PST and MRDT on short-term accommodation of less than 27 days.

The Province started collecting MRDT on tourist rentals listed on online accommodation providers on October 1, 2018. Compliance is legal requirement, and fines are in place for non-compliance, late filings or remittances.

Incremental funds collected through online accommodation providers are also eligible to be invested in affordable housing. The Province requires interested communities to submit an additional annual proposal to the Province. The RMOW has invested 100 per cent of its share of online accommodation provider revenues into the Cheakamus Crossing Phase II (Lot 1) affordable housing project since 2019.

I want to...

- Activities and classes

- Permits or licences

- Home Owner Grants

- MyWhistler account

- Parking pass

- E-newsletter subscription

- Council meetings and minutes

- Recreation facilities, parks and trails

- Career opportunities

- Bus schedules and information

- Parking information

- Permits and licences

- Bylaws and regulations

- Waste disposal information

- News Releases

- Bid opportunities

- Community monitoring indicators

- Parking (day rates and passes)

- Parking ticket

- Violation tickets

- Dog licence

- Business licence

- Property tax

- Recreation activity registration

- Parking passes

- Parking ticket payment

- Property taxes

- Report a concern

- All Online Services

- Meadow Park Sports Centre

- Notices and closures

- Rates: admission and passes

- Recreation activity schedules

- Login to MyRecreation

- Registration information

- Fitness Classes

- Nordic skiing/snowshoeing

- View all services

Section Quick Links

Our community vision.

Whistler: A place where our community thrives, nature is protected and guests are inspired. Learn More

Development

Sign up for the RMOW mailing List

Get the latest community news, upcoming events and programs and important updates from Council conveniently delivered straight to your inbox. Opt in or out anytime.

- Municipal Hall

- 4325 Blackcomb Way,

- Whistler, B.C. V8E 0X5

- Tel: 604-932-5535

- Fax: 604-935-8109

- Toll-Free: 1-866-932-5535

- [email protected]

- About the Resort Municipality of Whistler

- Accessibility

- Facts and Figures

- Privacy Policy

- Stay informed

- Newsletter subscription

- Submit website feedback

- Media contact

- Submit media inquiry

- Latest news

- Mayor and Council

- Departments

Whistler: A place where our community thrives, nature is protected and guests are inspired. More Info

- EN FRANÇAIS

News + Updates

- No Comments

GENERAL INFORMATION: As announced in British Columbia’s Budget 2022 on February 22, 2022, effective July 1, 2022, certain marketplace facilitators must charge and collect provincial sales tax (PST) and the municipal and regional district tax (MRDT) on taxable sales and leases that they facilitate through an online marketplace. This includes taxable sales of accommodation facilitated through an online marketplace by an online marketplace facilitator.

A marketplace facilitator is a person who:

- operates, owns or controls (solely or jointly) an online marketplace,

- through the online marketplace, facilitates a marketplace seller’s retail sales of goods, software or taxable services, and

- collects payment in respect of the retail sales of goods, software or taxable services.

Marketplace facilitators must register to collect and remit PST effective July 1, 2022, if they facilitate a marketplace seller’s retail sale of:

- goods that at the time of sale are located within Canada and are sold to a person in BC,

- software for use on or with an electronic device ordinarily situated in BC,

- accommodation in BC, or

- taxable services, other than accommodation, to a person in BC

However, marketplace facilitators are not required to register if:

- the gross value of retail sales of goods, software and taxable services that the marketplace facilitator made or facilitated in the preceding 12 months was $10,000 or less, or

- the reasonable estimate of the gross value of retail sales of goods, software and taxable services that the marketplace facilitator will make or facilitate in the next 12 months is $10,000 or less, or

- There are two or more marketplace facilitators who jointly operate, own or control an online marketplace and at least one of the other marketplace facilitators is registered for PST and will collect all PST payable for those taxable sales made through the online marketplace.

A marketplace seller is a person who, through an online marketplace, sells goods, software or taxable services (including accommodation). Additional information on the new rules is available in the Ministry of Finance’s Bulletin 142, Marketplace Facilitators, Marketplace Sellers, and Online Marketplace Services , available at: https://www2.gov.bc.ca/assets/gov/taxes/sales-taxes/publications/pst-142-marketplace-facilitators.pdf . In addition, Bulletin 120, Accommodation , has been updated with information on the new rules and is available at: https://www2.gov.bc.ca/assets/gov/taxes/sales-taxes/publications/pst-120-accommodation.pdf . SPECIFIC QUESTIONS: 1. Is the municipal and regional district tax (MRDT) and provincial sales tax (PST) exempt for all prepaid online travel agency (OTA) bookings?

These prepaid bookings are still subject to PST and MRDT (where applicable) as sales of accommodation in BC, unless a specific exemption applies. However, effective July 1, 2022, online marketplace facilitators are required to collect and remit the PST and MRDT where they facilitate retail sales of accommodation in BC made by an online marketplace seller through an online marketplace. Online marketplace facilitators are also generally required to register to collect and remit PST where they facilitate retail sales of accommodation in BC.

When it comes to online travel agency bookings, the online travel agency is considered an online marketplace facilitator and the accommodation provider is considered an online marketplace seller. Therefore, for prepaid bookings made through the online travel agency website, the online travel agency is required to collect and remit the applicable PST and MRDT on the facilitated accommodation sale. The accommodation provider does not collect and remit the PST and MRDT on these sales. Nevertheless, the accommodation provider remains jointly and severally liable for any PST and/or MRDT not collected and remitted by the marketplace facilitator.

Also, accommodation providers themselves are still required to collect and remit PST and MRDT on sales of accommodation in BC where they do not sell the accommodation through an online marketplace facilitator (e.g. the accommodation provider sells it over the phone or through their own website).

2. This does not apply for Fit and Tour bookings, only online travel agencies?

Where “Fit” and “Tour” bookings refer to purchases of tourism services from a tourism agent where accommodation has been packaged into that tourism service.

If a marketplace facilitator is required to be registered, then they must collect and remit PST and MRDT, when applicable, on all taxable sales of accommodation that they facilitate through their online marketplace.

However, where accommodation is purchased by a tourism agent and is packaged into a tourism service that the tourism agent sells to their customer through an online marketplace, the tourism agent is not considered to be making a sale of accommodation. Therefore, if a marketplace facilitator facilitates the sale of tourism service (that includes accommodation) by a tourism agent through the facilitator’s online marketplace, the marketplace facilitator does not charge PST or MRDT on the sale. No taxable sale of accommodation has taken place.

If the “Fit” or “Tour” booking does not involve purchasing a packaged tourism service from a tourism agent, then the booking does involve the taxable sale of accommodation. If a marketplace facilitator facilitates the sale of accommodation through the facilitator’s online marketplace, the marketplace facilitator must charge PST and MRDT on that taxable sale of accommodation.

3. Do OTA bookings that pay at the hotel still pay all taxes (GST, PST, MRDT)?

The Ministry cannot provide advice on the taxes of other jurisdictions, or the application of the Goods and Services Tax (GST)/Harmonized Sales Tax (HST), as that is a federal tax on sales of goods and services. The Canada Revenue Agency (CRA) is responsible for administering the GST/HST. For questions concerning the application of the GST/HST, your members may visit the CRA’s dedicated GST/HST web pages at or call the CRA at 1-800-959-5525.

PST and MRDT apply to all sales of accommodation in BC (unless a specific exemption applies) regardless of how and when the purchase of accommodation is made.

Who is responsible for collecting and remitting the PST and MRDT on a taxable accommodation sale depends on who is collecting the payment for the accommodation. If an individual books accommodation through an online marketplace but pays the accommodation provider directly, then PST and MRDT must be levied by the accommodation provider. In this situation, the online marketplace is not acting as an online marketplace facilitator because they are not collecting payment in respect of the accommodation. The accommodation provider is directly collecting the payment.

If an individual books accommodation through an online marketplace and payment for the accommodation is collected by the online marketplace, then the online marketplace is acting as an online marketplace facilitator and is required to collect and remit the PST and MRDT on the accommodation sale.

4. They are not GST exempt, only provincial taxes?

As mentioned above, the Ministry cannot comment on the taxes of other jurisdictions, or the application of the Goods and Services Tax (GST)/Harmonized Sales Tax (HST), as that is a federal tax on sales of goods and services. The Canada Revenue Agency (CRA) is responsible for administering the GST/HST. For questions concerning the application of the GST/HST, your members may visit the CRA’s dedicated GST/HST web pages at or call the CRA at 1-800-959-5525. We assume that the reference to “only provincial taxes” refers to accommodation providers who sell their accommodation on an online marketplace are not required to levy and collect PST and MRDT on that accommodation because the online marketplace facilitator will. If so, then that is correct.

5. Is there anything that the hotels should be doing to change their collection and remittance of taxes? Accommodation providers do not collect and remit PST and MRDT on sales of accommodation that are sold through an online marketplace facilitator that is required to be registered for PST. If an accommodation provider is unsure of whether a marketplace facilitator will be collecting and remitting PST and MRDT on accommodation sales made through the facilitator’s online marketplace, they should contact the facilitator as soon as possible to verify that the facilitator will be collecting and remitting the PST and MRDT. If the marketplace facilitator does not levy PST and MRDT as required on accommodation sales made through the online marketplace, the accommodation provider cannot charge PST and MRDT directly to the guest. The guest is required to self-assess and pay any PST and MRDT directly to government. 6. How is my business protected if I stop charging PST on July 1 assuming it will be remitted by the marketplace facilitator (e.g. Expedia, Booking.com)? If the PST and MRDT is for some reason not paid on these bookings and I am audited in the following year, I have no recourse to collect PST from the guest. Is this correct?

While the marketplace facilitator is required to register, levy and collect PST and MRDT on accommodation sales that are facilitated through the online marketplace, the accommodation provider remains jointly and severally liable for any PST and MRDT not collected and remitted by the marketplace facilitator if the marketplace facilitator is later assessed for the outstanding PST and MRDT.

As noted in our answer to #5, if the marketplace facilitator does not levy PST and MRDT as required on accommodation sales made through the online marketplace, the accommodation provider cannot charge PST and MRDT directly to the guest. The guest is required to self-assess and pay any PST and MRDT directly to government.

7. I am assuming the tax consequence to be triggered by the payment, for example, an Expedia Prepaid booking attracts tax to be levied by Expedia. However, if someone uses Expedia, but just as a booking tool and then pays us directly when they get to the hotel, does that extinguish Expedia’s role as tax collector and put it back on the hotelier? Yes, as noted in answer to #3, this is correct. Who is responsible for collecting and remitting the PST and MRDT on a taxable accommodation sale depends on who is collecting the payment for the accommodation. If an individual books accommodation through an online marketplace (e.g. Expedia) but pays the accommodation provider directly, then PST and MRDT must be levied by the accommodation provider. In this situation, the online marketplace is not acting as an online marketplace facilitator because they are not collecting payment in respect of the accommodation. The accommodation provider is directly collecting the payment.

If an individual books accommodation through an online marketplace and payment for the accommodation is collected by the online marketplace (e.g. Expedia), then the online marketplace is acting as an online marketplace facilitator and is required to collect and remit the PST and MRDT on the accommodation sale. FURTHER INFORMATION For more information on British Columbia’s PST, including registration, and collecting and remitting the PST, can be found in a series of PST Bulletins and Notices , and the Small Business Guide to PST . Our Forms Page contains exemptions certificates and forms related to registration, applying for a refund, and self-assessing the PST. For additional information, including free interactive webinars, informational videos and upcoming events, you may be interested in visiting the Government’s PST Outreach webpage. To receive updates about legislative changes and new public information, click “Subscribe To Receive Updates.” To share any additional questions – reach out to [email protected] .

Leave a Reply Cancel reply

You must be logged in to post a comment.

- February 2024

- January 2024

- December 2023

- September 2023

- August 2023

- February 2023

- January 2023

- December 2022

- November 2022

- September 2022

- August 2022

- February 2022

- January 2022

- Advocacy Win

- BC Tourism Hospitality Conference

- Government Relations

- Hotel Cyber Awareness

- IT Partners

- Message From Ingrid Jarrett

- Rapid Tests

- Recruitment

- Restrictions

- Road Closures

- Safety Plan

- State of Emergency

- Tip Our Hat

- Uncategorized

Copyright © 2023 All Rights Reserved BC Hotel Association

Tourism Commission

The Bellingham Tourism Commission makes recommendations to the City for allocations to local organizations as part of the Tourism Promotion grant program. The 2024 Tourism Grant Application submittal window has CLOSED. Visit the Tourism Promotion webpage for grant and funding information.

The Tourism Commission typically meets on the fourth Tuesday of each month. Meetings can be attended either in-person (see meeting agenda for location), or virtually via Zoom Webinar. If attending via Zoom, attendees are required to register prior to joining the meeting. Once registered, an email with pertinent meeting information will be sent to you.

No registration is required for the May 10th Meeting

Tourism Commission Meeting

- Meeting Materials

Visit meetings.cob.org to view meeting agendas and supporting materials, which are posted approximately one week prior to the meeting date. If you are interested in meetings held prior to March, 2023 – visit the Tourism Commission Meeting Materials archive page.

Meetings are typically held the fourth Tuesday of each month in the Mayor’s Board Room at City Hall (although a few meetings are often held at an offsite location). Meetings begin at 3:30 p.m. and last approximately one to two hours. Time spent outside of meetings may be as much as two hours a week depending on involvement in the Commission.

The Commission consists of thirteen members appointed by the Mayor. Terms of office are three years, and no compensation is paid to members of this Commission. Fifty percent of the commission’s membership can be residents of Whatcom County; the other 50% must have lived in Bellingham for at least two years. The Lodging Tax Advisory Board, a sub-committee of the Tourism Commission, makes recommendations to the City for allocations to local organizations as part of the Tourism Promotion grant program.

Current Boards & Commission Vacancy List (PDF)

- Roster (PDF)

Main Office Planning & Community Development Department 210 Lottie Street Bellingham, WA 98225

Phone: (360) 778-8300 Email: [email protected] Map

- Municipal Code 2.80

- Tourism Commission Meeting Materials through Feb 2023

As B.C.'s carbon tax goes up, here's how you qualify for a rebate

Metro Vancouver gas pump price hits almost $2.09 a litre after B.C. carbon tax increase April 1.

You can save this article by registering for free here . Or sign-in if you have an account.

Article content

The price at the gas pump went up again this week, hitting $2.09 a litre around Metro Vancouver.

As B.C.'s carbon tax goes up, here's how you qualify for a rebate Back to video

While the cost of gas is calculated based on a number of factors, the increase to the B.C. carbon tax that came into effect April 1 certainly didn’t help.

Here’s what to know about B.C.’s carbon tax.

What is the carbon tax?

B.C.’s carbon tax is a tax on carbon pollution, meant to encourage companies and consumers to shift from fossil fuels to greener forms of energy. The tax is collected at the point of retail.

Subscribe now to read the latest news in your city and across Canada.

- Unlimited online access to articles from across Canada with one account.

- Get exclusive access to the Vancouver Sun ePaper, an electronic replica of the print edition that you can share, download and comment on.

- Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

- Support local journalists and the next generation of journalists.

- Daily puzzles including the New York Times Crossword.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

Sign In or Create an Account

The province’s carbon tax has been in place for 16 years and was first implemented by the B.C. United party, then known as the B.C. Liberals, in 2008.

How much did the carbon tax go up on April 1 and how much did it impact gas prices?

On Monday, B.C. raised its carbon tax by 23 per cent, to $80 a tonne from $65 a tonne, an amount that the B.C. NDP government said represents an increase of about three cents a litre.

Gas prices across Metro Vancouver jumped to almost $2.09 a litre on Monday as the carbon tax increase came into effect, although there were a few stations charging a few cents below the high of that price.

Why is there a rebate?

The carbon tax was designed to be returned to taxpayers in the form of a rebate: the climate action tax credit. The credit is a quarterly payment meant to offset the tax for lower income earners and households.

How do I know if I’m eligible for the rebate?

It’s estimated that around 65 per cent of people in B.C. will qualify for the climate action tax credits aimed at low- to middle-income earners. Your eligibility is automatically calculated based on your tax return. You don’t need to apply for the rebate, and only one person can receive the credit on behalf of a family.

Start your day with a roundup of B.C.-focused news and opinion.

- There was an error, please provide a valid email address.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

A welcome email is on its way. If you don't see it, please check your junk folder.

The next issue of Sunrise will soon be in your inbox.

We encountered an issue signing you up. Please try again

How much is the rebate?

For those who qualify for the tax credit , the amount received is based on household size and net income.

Currently, a single person with a take-home income of less than $39,000 gets a maximum credit of $447 this year, which is divided into quarterly payments made in July, October, January and April. The payments get smaller the more a single person makes until $61,000 a year, at which the credit is zero.

These rebates and thresholds will increase in July, so that a single person will get $504 if they make less than $41,000 a year.

A family of five with two parents and three children with take-home pay of less than $50,000 a year currently qualifies for about double the amount of the tax credit a single person, at about $1,003 a year. The payments get smaller as the family’s household income increases until $100,420 a year, at which the credit is zero.

To see the income thresholds for your specific family situation, visit the B.C. government’s website here for details.

When does the eligibility change?

The eligibility thresholds will change in July. The new thresholds for the maximum net income a year a single person or a household of five can make before the tax credit is zero haven’t yet been published, said Kathryn Harris, a University of B.C. political science professor, who specializes in environmental, climate and energy policy.

She is expecting they will be in the ballpark of in the low $60,000 range for a single person and to just above $100,000 a year for a household of one or two income-earners and three dependents, which is about median income.

Do other provinces have a carbon tax too?

B.C.’s carbon tax rebate program is separate and different from the federal carbon rebate, which is new in 2024 and active in eight provinces: Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, P.E.I., and Newfoundland and Labrador.

The main distinction between the carbon tax rebates being issued by the federal government to these eight provinces and B.C.’s system is that B.C. assesses income and household size while Ottawa gives rebates based on the amount collected in each province and, from there, only looks at household size, according to Harris.

She said that the federal government distributes 90 per cent of carbon tax revenues it takes in through its rebate.

Even though the federal program doesn’t overtly put emphasis on giving rebates based on income, some 80 per cent of households get more from the rebates than they pay out in carbon tax. This happens because the 20 per cent of households at the top of the range by income pay the most in carbon taxes because they use more fuel, said Harris.

Harris said it’s not straightforward to compare B.C.’s carbon tax rebates with the federal program. If a government doesn’t return carbon taxes collected through rebates, it may be spending it in other areas such as education and health care.

Bookmark our website and support our journalism: Don’t miss the news you need to know — add VancouverSun.com and TheProvince.com to your bookmarks and sign up for our newsletters here .

You can also support our journalism by becoming a digital subscriber: For just $14 a month, you can get unlimited access to The Vancouver Sun, The Province, National Post and 13 other Canadian news sites. Support us by subscribing today: The Vancouver Sun | The Province .

Postmedia is committed to maintaining a lively but civil forum for discussion. Please keep comments relevant and respectful. Comments may take up to an hour to appear on the site. You will receive an email if there is a reply to your comment, an update to a thread you follow or if a user you follow comments. Visit our Community Guidelines for more information.

AMBER ALERT: Langley RCMP searching for three-month-old boy

Metro vancouver gas prices explained: here's a breakdown of the price at the pump.

Illicit drug use in Island Health hospitals sparks WorkSafeBC investigation

Alleged gunman killed the wrong target in 2020 Richmond murder, prosecutor says

13-year-old driver totals high-powered lamborghini huracan in west vancouver.

This website uses cookies to personalize your content (including ads), and allows us to analyze our traffic. Read more about cookies here . By continuing to use our site, you agree to our Terms of Service and Privacy Policy .

You've reached the 20 article limit.

You can manage saved articles in your account.

and save up to 100 articles!

Looks like you've reached your saved article limit!

You can manage your saved articles in your account and clicking the X located at the bottom right of the article.

- Your Profile

- Your Subscriptions

- Your Business

- Support Local News

- Payment History

- Sign up for Daily Headlines

- Sign up for Notifications

Some Canadian tourists in Mexico must pay a new fee before they leave. Here's what to know

- Share by Email

- Share on Facebook

- Share on LinkedIn

- Share via Text Message

If you are looking to get your dose of Vitamin D in Mexico during the extended rainy season in Vancouver, you are far from alone.

But you might want to be aware of a couple of relatively recent tourism updates before you head down.

First and foremost, you need to heed the Canadian government's travel advisory for the country.

While the lion's share of residents from the Great White North will likely enjoy a relaxing holiday, there have been some tragic incidents that may give prospective visitors pause.

Mexico's powerful drug cartels commonly use local gangs to defend their territory and carry out their vendettas. Tourists from Canada and the United States have been victims of kidnappings. They have also been caught in the crossfire of shootings between rival gangs.

Due to the levels of violence, the Canadian government advises travellers to exercise a high degree of caution in Mexico . The U.S. Department of State also recently warned travellers about increased levels of violence in Mexico and updated its advisory.

- Get a complete picture of what to be aware of with the travel advisories for Mexico in our guide.

Travel from Vancouver to Mexico in 2022

Are you looking to visit Quintana Roo?

If you aren't sure exactly where that is, you may be more familiar with some of the names of the state's most popular tourist spots, including Cancun, Playa del Carmen, and Tulum.

Quintana Roo is Mexico's most frequented tourist state, and home to the breathtaking Mayan Riviera. Millions of visitors flock to its beaches and resorts annually, making Cancun International Airport the tenth busiest in the world with international travellers, according to the airport's website.

But there have been a couple of changes for air passengers arriving at the airport from foreign countries (and for those heading home, too).

Whether you choose a Mexico all-inclusive stay or a self-guided adventure, you'll have to pay a new fee as part of your stay. Luckily, it doesn't cost that much and the process for paying it isn't very complicated.

Visatax is described as "the payment of contributions from foreign tourists" to Quintana Roo state. To complete the payment process, you need to provide the government with the requested information and make the required payment. It came into effect on April 1, 2021 - a time when many Canadians were not contemplating their next visit to Mexico.

The application form asks for your departure date, the number of visitors, your full name, your passport number, and your age. Finally, you'll be asked to pay about 241 Mexican pesos, which converts to roughly $15.81 CAD.

You can view the Visatax portal online and you may complete the process before you visit Mexico or just before your departure flight out of the country. You can also pay in person at the airport but this can get a little chaotic at times; it is best to pay in advance. Also, if you try to pay online at the airport be forewarned that the airport's internet is very hit and miss.

And the good news about visiting Cancun in 2022

Aside from the fact that Mexico has very few travel rules for entry at this time, the government has introduced a pilot that will make it even easier to visit Quintana Roo this year.

Now, air passengers arriving at Cancun International Airport do not have to fill out the Forma Multipla Migratoria (FMM) as part of the immigration process. Now, Canadian tourists arriving at the airport will be granted a 180-day stay in Mexico. If you've ever ventured through the airport, filling out the paperwork could slow down the process dramatically, particularly in Cancun. Even if you had filled it out beforehand, you might be caught waiting in sprawling lines filled with travellers who hadn't already done so.

While some of the websites haven't been updated to reflect this information, travellers arriving at the airport have passed through without issue, which has sped up the immigration process dramatically. That said, this rule doesn't apply nationally: it is a pilot in Cancun and you should still fill out the form if you plan on arriving at other Mexican airports.

- Oldest Newest

This has been shared 0 times

Featured Flyer

Carbon tax, increases to hydro, B.C. Ferries to kick in April 1

Public venue rental and bike-share fees also set to go up on april fool's day.

Social Sharing

At a time when the cost of living remains top of mind for many British Columbians, some things are set to cost more on Monday.

Here are some of the things British Columbians can expect to pay more for starting on April Fool's Day.

An increase to the carbon tax is set to come into effect on April 1. The carbon price is scheduled to rise from $65 to $80 per tonne.

B.C. introduced North America's first broad-based carbon tax in 2008, and will administer the coming tax increase on behalf of the federal government.

Canadians living in the eight provinces with the federal carbon tax receive quarterly rebate payments, which vary depending on the province and the size of household.

'There will be a carbon tax election,' Poilievre tells supporters in B.C.

B.C., Quebec and the Northwest Territories follow their own carbon-pricing mechanisms that meet federal standards and are exempt from the federal program.

Opposition Conservative Leader Pierre Poilievre recently sent a letter to B.C. Premier David Eby asking him to join seven other premiers in opposing the April 1 tax increase, saying the 23 per cent hike amounts to an extra 18 cents on a litre of fuel and people in B.C. and Canadians can't afford it.

- Analysis Is the carbon tax suffering from a failure to communicate?

- Premier David Eby mocks Pierre Poilievre's letter asking B.C. to join carbon tax fight

Eby responded by saying B.C. would end up with less money returned to the province if it accepted Poilievre's request.

"I don't live in the Pierre Poilievre campaign office and baloney factory," said Eby. "I live in B.C., am the premier and decisions have consequences.

"The fact we face is that if we followed Mr. Poilievre's suggestion there would be less money returned to British Columbians after April 1 than there would be if the federal government administered this increase directly."

PM fires back at carbon tax opponents amid protests and carbon price hike

B.c. hydro (but there is a credit).

B.C. Hydro rates will go up 2.3 per cent on April 1, following approval from the B.C. Utilities Commission.

Following the application back in October, B.C.'s Energy Ministry said it marked the sixth year in a row that the Crown utility has applied for an increase below the rate of inflation.

In February, the province announced the B.C. electricity affordability credit for eligible customers.

B.C. Hydro says the credit "will more than offset this increase." Customers don't need to apply for the credit, which will be applied automatically.

- B.C. Hydro requests 2.3% rate increase for spring 2024

The credit amount will be automatically calculated based on a customer's electricity consumption over the past year, the Crown utility says, with the average residential customer seeing around $100 in savings.

FortisBC, which provides power to some parts of the province, raised rates on Jan. 1.

B.C. Ferries

Starting April 1, B.C. Ferries fare prices will increase by an average of 3.2 per cent each year for the next four years.

The Ministry of Transportation and Infrastructure announced in October that provincial funding pledged earlier in the year minimized the fare increase, which would have been approximately 9.2 per cent per year without the funding.

B.C. Ferries says customers will have more opportunities to book discounted fares with increased savings for those who carpool and book in advance, as well as foot passengers who book ahead.

Park board fees

Back in November, the Vancouver Park Board approved a number of fee increases for 2024 recommended by park board staff.

Staff recommended an average increase of six per cent for most fees and charges.

- Vancouver Park Board votes to hike service fees by average of 6% in 2024

Most fees changed on Jan. 1 while some go into effect on April 1, including recreation rental permits for venues such as arenas, pools, sports fields, courts, and the Burrard Civic Marina.

Beer and alcohol

The federal government will cap the annual alcohol excise tax increase on beer, spirits and wine at two per cent for an additional two years.

The alcohol excise tax had been set to rise on April 1 by 4.7 per cent, tied to inflation, but Finance Minister Chrystia Freeland announced in March that the increase is being capped at the lower rate until 2026.

- 'Beer tax' increase capped at 2 per cent until 2026, Freeland announces

Other increases

People who use Vancouver's Mobi bike share service will see per-minute rates go from 25 cents to 29 cents for a standard bike and 35 cents to 39 cents a minute for an e-bike starting Tuesday.

Looking ahead, transit fares for TransLink users will go up about 2.3 per cent this summer.

On July 1, single-zone fares will increase five cents, from $3.15 to $3.20. Two-zone fares will increase by 10 cents, to $4.65 and three-zone fares will go up 15 cents, up to $6.35.

Day passes, discounted tickets and monthly passes will also see slight increases.

With files from Renée Lukacs and The Canadian Press

Related Stories

- Top stories from British Columbia

- Vancouver raises the bar for alcohol-free drinks

- Photos Residents stroll riverbed in Prince George amid drought

- B.C. group pushes for greater buffer between boats, killer whales

- Skip to main content

- Skip to main navigation

- Accessibility Statement

More topics

- Terms and definitions

Exemptions from the BC home flipping tax

The proposed BC home flipping tax applies to income from the sale of a property, including presale contracts, in British Columbia if the property was owned for less than 730 days, unless an exemption applies.

The tax is imposed under the Residential Property (Short-Term Holding) Profit Tax Act , which takes effect starting January 1, 2025, subject to approval by the legislature.

Exemptions can be based on the property location, the entity that sells the property, certain life circumstances or other exemptions.

Stay up to date

Subscribe to receive email notifications when we update our website.

On this page

Exempt property locations, exempt entities, life circumstance exemptions, additional exemptions.

Residential property located in any of the following locations is exempt from filing a return and paying the BC home flipping tax:

- A reserve as defined in section 2(1) of the Indian Act (Canada)

- Nisga’a Lands

- Nisga’a Fee Simple Lands as defined in the Definitions Chapter of the Nisga’a Final Agreement

- shíshálh lands as defined in section 2(1) of the shíshálh Nation Self-Government Act (Canada)

- Treaty lands of a Treaty First Nation

- Maa-nulth First Nation Lands as defined in the Definitions Chapter of the Maa-nulth First Nations Final Agreement

- Tla’amin Lands as defined in the Definitions Chapter of the Tla’amin Final Agreement

- Tsawwassen lands as defined in the Definitions Chapter of the Tsawwassen First Nation Final Agreement

If you qualify as one of the following entities on the date of the sale of the property, you are exempt from the BC home flipping tax:

- A registered charity as defined in section 248(1) of the Income Tax Act (Canada)

- An association as defined in section 1(1) of the Cooperative Association Act

- The government

- An agent of the government

- An Indigenous Nation

- An organization included in the government reporting entity as defined in section 1(1) of the Budget Transparency and Accountability Act

- A government body as defined in section 1 of the Financial Administration Act

- A local public body as defined in Schedule 1 of the Freedom of Information and Protection of Privacy Act

- A public body referred to in Schedule 2 of the Freedom of Information and Protection of Privacy Act

- A corporation owned by a municipality

- A corporation owned by a regional district

- A corporation owned by an Indigenous Nation

- Certain housing corporations which are exempt from tax under section 149(1)(i) of the Income Tax Act (Canada)

- A non-profit organization described in section 149(1)(l) of the Income Tax Act (Canada)

- A limited-dividend housing company described in section 149(1)(n) of the Income Tax Act (Canada)

You will still have to file a BC home flipping tax return, but may not have to pay the BC home flipping tax if you experience any of the following life circumstances and they are considered to lead to the sale of a property.

The following exemptions apply to individuals if the sale reasonably occurred due to, or in anticipation of, at least one of these events.

Death of a related individual

If you receive a residential property due to the death of a related individual, you may either sell the new property you received or sell your own property to move into the new property and not pay the BC home flipping tax.

Serious illness or disability

If you or a related individual suffers from a serious illness or disability.

Eligible relocation

If you or your spouse or common-law partner make an eligible relocation for one of the following reasons:

- To carry on a business or to be employed at a particular location

- To be a student enrolled full-time in a program at a post-secondary level at a particular location of a university, college, or other educational institution

To qualify for the eligible relocation exemption to sell your primary residence, your primary residence must be 40 kilometres (km) farther from your new job or school than your new primary residence.

To qualify for the eligible relocation exemption to sell a secondary property that is not your primary residence, the secondary property must be 100 km farther from your new primary residence than it was from your current primary residence.

Change in household membership

If there’s a change in household membership that results in a property sale, that property sale is exempt from tax. A change in household membership can include a person related to you moving in with you, you moving in with a related person, and having or expecting a child.

The following exemptions apply to individuals if the sale is reasonably considered to have occurred due to at least one of the following events.

Breakdown of marriage or common-law partnership

If there is a breakdown of your marriage or common-law partnership and you have been living separate and apart from your spouse or common-law partner for at least 90 days prior to the sale.

Involuntary termination of employment

If you or your spouse or common-law partner experience an involuntary termination of employment and have to sell your property, you are exempt from the BC home flipping tax.

This exemption does not apply to self-employed individuals.

Threat to personal safety

If you or a related person who lives with you experiences a threat to personal safety and you sell your property, you are exempt from the BC home flipping tax.

The following list of additional exemptions are available if the sale can reasonably be considered to occur due to one or more of the following events having occurred before the sale. Unlike the other life circumstance exemptions, these additional exemptions are also available to corporations, partnerships, and trusts.

Bankruptcy and insolvency

- Made an assignment in bankruptcy

- Filed a notice of intention to make a proposal with the official receiver, or

- Made a proposal under Division 1 of Part III of that Act

- Has had a bankruptcy order made against them

- The taxpayer is a corporation and has obtained a court order granting a stay of proceedings under section 11.02 of the Companies’ Creditors Arrangement Act (Canada)

- The taxpayer has had a winding-up order made against them under the Winding-Up and Restructuring Act (Canada) based in whole or in part on the person being insolvent

- The taxpayer has made an application to the administrator under section 5 of the Farm Debt Mediation Act (Canada) and has been found by the administration to be eligible to make that application

- The taxpayer is a corporation and the only shareholder of the corporation is a person who is described above

Housing unit was destroyed

If a residential property is sold because a housing unit is uninhabitable because it was destroyed by, or couldn’t be rebuilt because of damage caused by:

- An earthquake

- A landslide

- A spill or leakage of oil, gas or another poisonous or dangerous substance

- Any other natural disaster or dangerous event

Expropriation of the residential property

If you experience the expropriation of your residential property, you are exempt from the BC home flipping tax.

Property acquired through lottery

If you acquire residential property through a lottery and sell that property, you are exempt from the BC home flipping tax.

Death of an unrelated individual

If you receive a residential property as a direct consequence of the distribution of the property of a deceased person, you may sell that residential property and not pay the BC home flipping tax.

Foreclosure

You are exempt from the BC home flipping tax if the sale of your residential property is due to:

- The exercise of a power of sale by the registered owner of a charge on the residential property

- An order absolute of foreclosure

- Any other order of a court ordering a sale of the residential property

Estimated completion date delayed more than 365 days

You are exempt from the BC home flipping tax if all of the following are met:

- You enter into an agreement to purchase a new housing unit that’s going to be constructed or placed on the residential property, and

- You are given a new estimated completion date and that date is more than 365 days later than the original estimated completion date given to you when you entered into the agreement, and

- The original and new estimated completion dates were provided to you in writing by the developer

Related party transactions

Related party transactions are exempt from the BC home flipping tax. Related party transactions are sales between related persons .

Exemption for builders and developers

A person is exempt from the home flipping tax if:

- In the ordinary course of business, the person ordinarily buys and sells property for the purpose of constructing or placing buildings on the property (developers) or constructs or places buildings on property held for that purpose (builders); and

- The taxable property was held by the person for the purposes above.

These activities do not have to occur on the residential property to qualify for this exemption.

Exemption for exclusive commercial use

You are exempt from the home flipping tax if you used a residential property exclusively for a commercial purpose for the entire time that you held that property.

Building activity on land without a housing unit

If building activity occurs on a residential property that does not contain a housing unit at the time of purchase, the taxpayer will be exempt from the BC home flipping tax in respect of the construction or placement of a housing unit.

Building activity means:

- Completion of clearing or excavating the site in preparation for a house

- Constructing or placing the housing unit on the residential property

- Any other prescribed activity necessary for the construction or placement of the housing unit

Exemption for renovations and construction of additional housing units

If there is a substantial renovation of a housing unit, the property will be exempt from the BC home flipping tax.

If a housing unit is demolished and a new housing unit is constructed or placed on that property, the property will be exempt.

If there is an additional housing unit added to either an existing housing unit (in other words, a basement suite) or constructed or placed on the residential property with an existing housing unit, the property will be exempt from the BC home flipping tax.

The renovation, addition, construction, or placement of the housing unit must be in accordance with a bylaw of a local government with jurisdiction over the property or a British Columbia Building Code established under the Building Act.

Contact information

The B.C. Public Service acknowledges the territories of First Nations around B.C. and is grateful to carry out our work on these lands. We acknowledge the rights, interests, priorities, and concerns of all Indigenous Peoples - First Nations, Métis, and Inuit - respecting and acknowledging their distinct cultures, histories, rights, laws, and governments.

IMAGES

COMMENTS

The Municipal and Regional District Tax (MRDT) was introduced in 1987, by the Provincial Government, to provide funding for local tourism marketing, programs, and projects. The tax is intended to help grow BC revenues, visitation, and jobs, and amplify BC's tourism marketing efforts in an increasingly competitive marketplace.

The tax applies to sales of short-term accommodation provided in the City of Vancouver, effective February 1, 2023 until January 31, 2030, at the rate of 2.5%. The Major Events MRDT applies in addition to the 8% PST and 3% MRDT for the City of Vancouver, and applies in the same manner as the MRDT. Each tax must be listed separately on invoices.

Tourism funding sources. Indigenous Tourism COVID-19 tourism supports - Indigenous Tourism British Columbia offers comprehensive and frequent updates on credit and financing options, income and employee support, and Provincial and Federal funding programs.. Municipal and Regional District Tax - This tax program for communities provides funding for local tourism marketing, programs and ...

Consumer Taxes in British Columbia Goods and Services Tax (GST) - a 5% federal tax on goods and services. Provincial Sales Tax (PST) - a 7% provincial tax on goods and services. Some Exemptions apply. Hotel Room Tax (HRT) - a 4.15% provincial tax on short-term accommodation. More information about the various

British Columbia is introducing a new tax on hotels and other short-term accommodations that communities can tap to offset the cost of hosting major tourism events. The idea for the surtax, called ...

A new Major Events Municipal and Regional District Tax (MRDT) of up to 2.5% on short-term accommodation sales would help communities cover the cost of hosting major international tourism events that help bolster provincial tourism and the economy. The Major Events MRDT is a time-limited, dedicated funding tool that communities can apply for ...

The Municipal and Regional District Tax (MRDT) is a tax of up to three per cent (3%) on the purchase of short-term tourist accommodation imposed in specific geographic areas of British Columbia (designated accommodation areas) on behalf of municipalities, regional districts or eligible entities. The MRDT program - sometimes referred to as the ...

The Municipal and Regional District Tax program (MRDT) is a provincial program jointly administered by the BC Ministry of Finance, BC Ministry of Tourism, Arts & Culture and Destination BC, the crown corporation providing tourism services for the province. The MRDT is an accommodation tax collected under the provincial sales tax legislation to ...

The purpose of this tax is to help cover the cost of planning, staging and hosting eligible major international tourism events that generate significant international visitation and help bolster provincial tourism and the economy. The Major Events MRDT program applies to: Municipalities; Regional districts, and

The total rate in Vancouver (as of February 2023) is 20% of the room rate, consisting of: 3% Municipal & Regional District Tax (MRDT), which most major cities in BC collect. 2.5% Major Event MRDT. On Feb 1, 2023, a temporary Major Events MRDT over seven years was introduced and in effect until Jan 31, 2030. 1.5% Destination Marketing Fee (DMF).

Tourism businesses employed 154,366 people. There were 16,910 tourism businesses in operation. Tourism generated $18.5 billion in revenue. Tourism contributed $2.2 billion in provincial taxes. Tourism contributed $7.2 billion (2.4%) to the provincial economy, as measured through gross domestic product (in 2017 constant dollars).

Municipal and Regional District Tax. MRDT - also known as Hotel Tax - applies to short-term tourist accommodation, including hotel rooms. This 3% hotel tax is in addition to the eight per cent Provincial Sales Tax (PST). The MRDT tax program was originally established by the Province in 1987 to support the financing and operations of ...

Vancouver and Toronto are among 16 North American host cities and will hold 10 of the event's 70 matches. Vancouver seeks 2.5% tax on short-term accommodation to raise revenue for hosting FIFA ...

In British Columbia an 8% Provincial Sales Tax (PST) is charged on all short-term room rentals by hotels, motels, cottages, inns, resorts and other roofed accommodations. Campsite and RV site bookings are exempt from any PST. The PST for other goods and services is set at 7%. Some items such as food and books are exempt this tax.

Important Update On Changes Re. Ota Taxation. As announced in British Columbia's Budget 2022 on February 22, 2022, effective July 1, 2022, certain marketplace facilitators must charge and collect provincial sales tax (PST) and the municipal and regional district tax (MRDT) on taxable sales and leases that they facilitate through an online ...

Fifty percent of the commission's membership can be residents of Whatcom County; the other 50% must have lived in Bellingham for at least two years. The Lodging Tax Advisory Board, a sub-committee of the Tourism Commission, makes recommendations to the City for allocations to local organizations as part of the Tourism Promotion grant program.

It's estimated that around 65 per cent of people in B.C. will qualify for the climate action tax credits aimed at low- to middle-income earners. On Monday, B.C. raised its carbon tax by 23 per ...

Training & Finding Jobs in B.C.'s Tourism Sector. Tourism in B.C. supported over 46,400 jobs in 2020. This includes $2.4 billion in GDP (in 2012 constant dollars) contributed to B.C.'s economy and $1.8 billion in tourism wages & salaries. There are many different jobs available in the tourism sector. Use these resources to find tourism jobs and ...

It came into effect on April 1, 2021 - a time when many Canadians were not contemplating their next visit to Mexico. The application form asks for your departure date, the number of visitors, your full name, your passport number, and your age. Finally, you'll be asked to pay about 241 Mexican pesos, which converts to roughly $15.81 CAD.

An increase to the carbon tax is set to come into effect on April 1. The carbon price is scheduled to rise from $65 to $80 per tonne. B.C. introduced North America's first broad-based carbon tax ...

BC has proposed increasing the tax credit amounts, effective July 1. This would mean $504 for individuals, $252 for spouses, and $126 for each child. The threshold will also increase to $41,071 for individuals and $57,288 for families. Starting this July, over 2 million people will see a boost to their quarterly Climate Action Tax Credit.

Contact information. Please send your questions and service requests to BC Stats here. Mail to: BC Stats, Box 9410 Stn Prov Govt, Victoria BC V8W 9V1. Location: 563 Superior Street, Victoria BC. Place to find data and analysis related to tourism.

Starting April 1, 2024, qualifying individuals buying homes up to $835,000 now receive an exemption on the property transfer tax on the first $500,000 of the home's value. Qualifying individuals can get a reduced exemption for qualifying homes valued between $835,000 and $860,000. An estimated 14,500 people, twice as many as previously, will ...

Exemptions from the BC home flipping tax. The proposed BC home flipping tax applies to income from the sale of a property, including presale contracts, in British Columbia if the property was owned for less than 730 days, unless an exemption applies. The tax is imposed under the Residential Property (Short-Term Holding) Profit Tax Act, which ...