The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

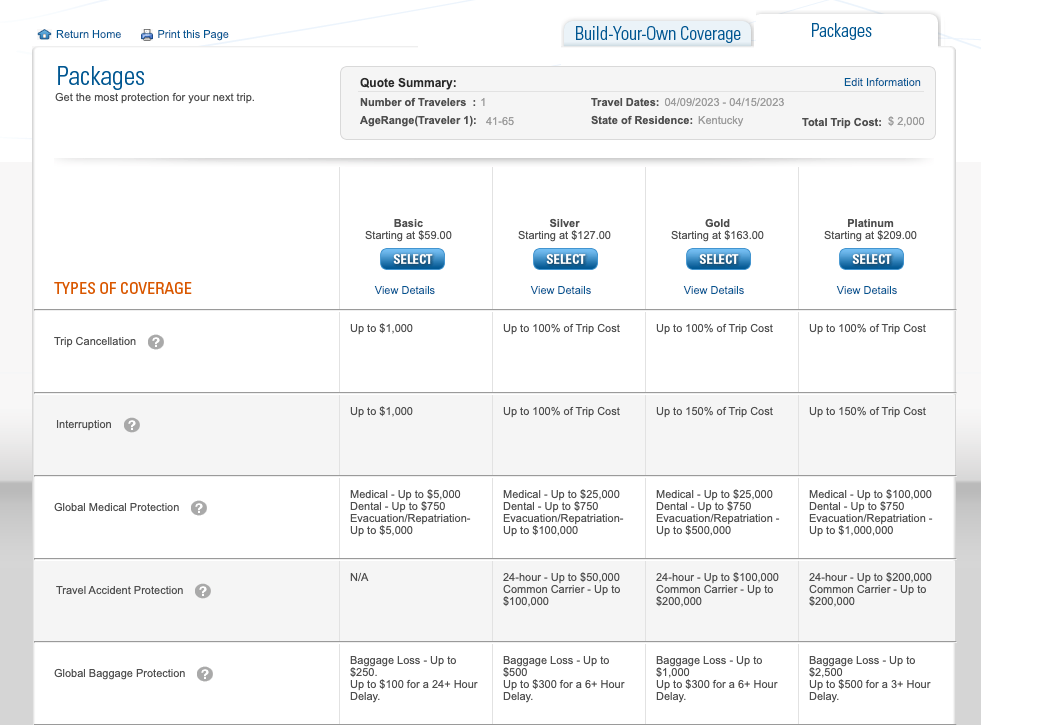

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

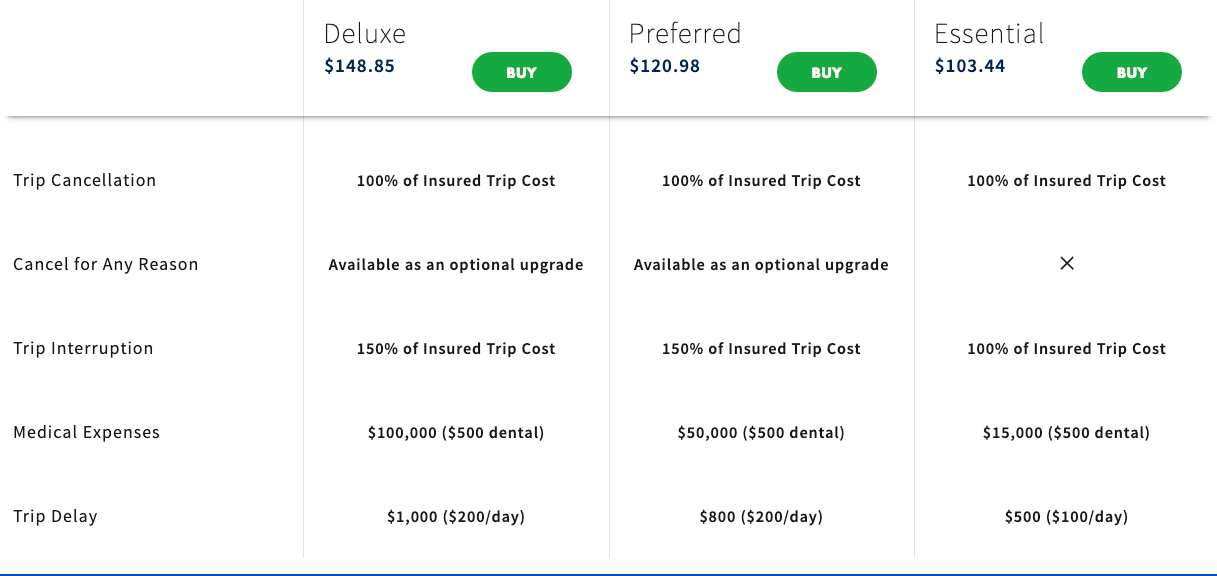

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

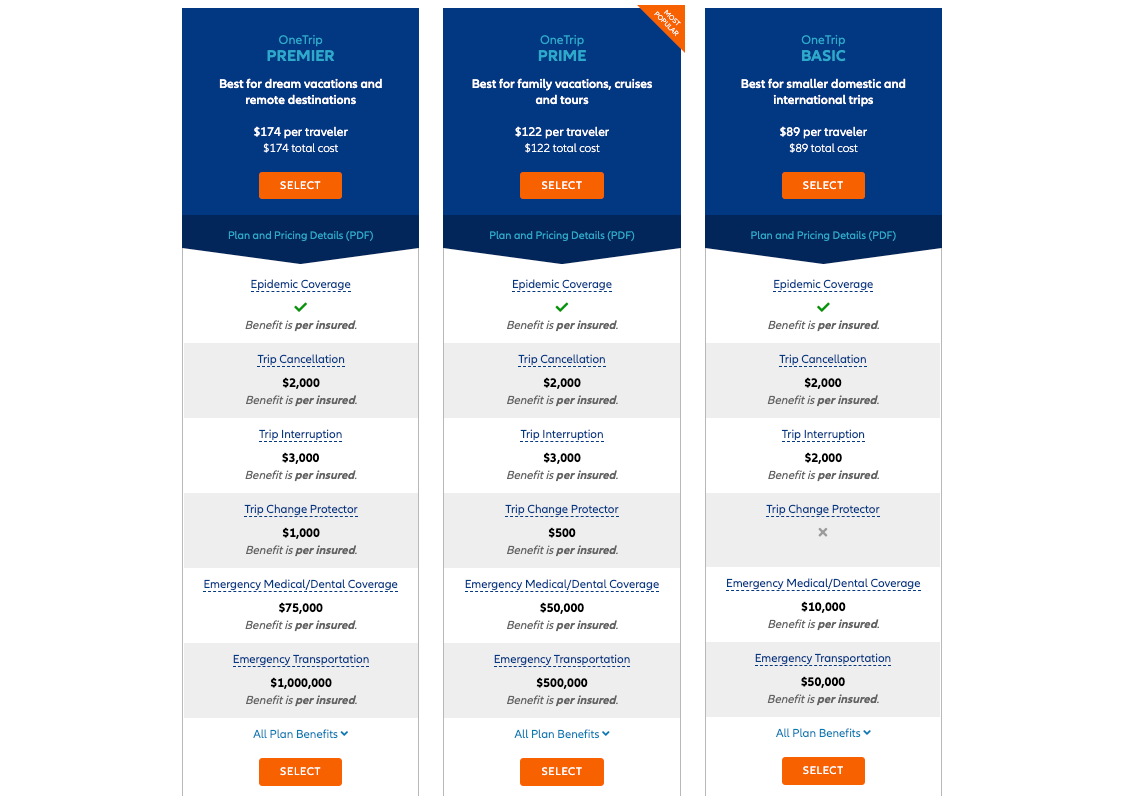

Allianz Travel Insurance

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

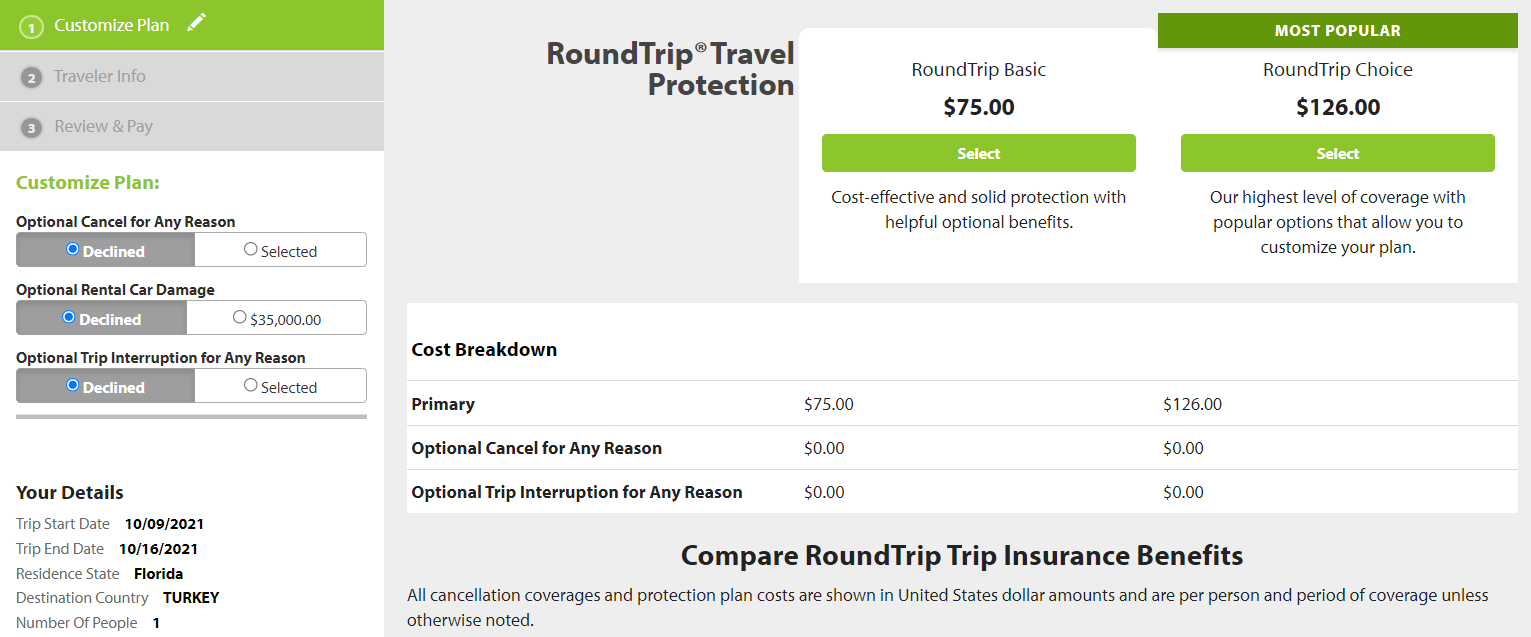

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

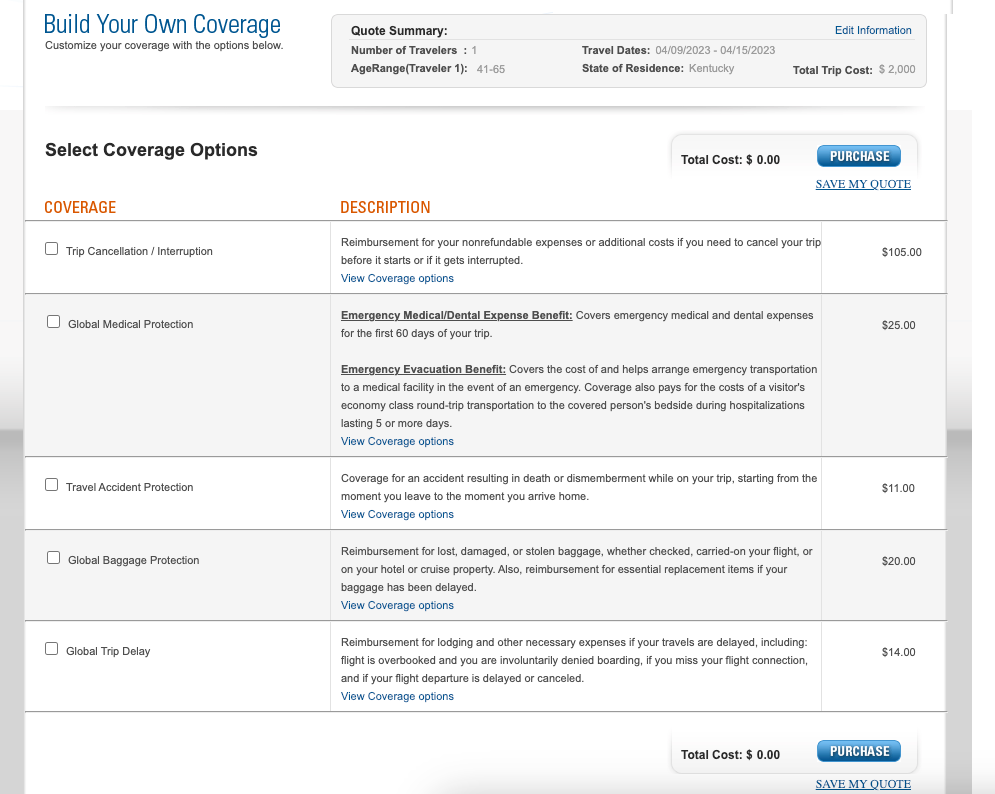

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

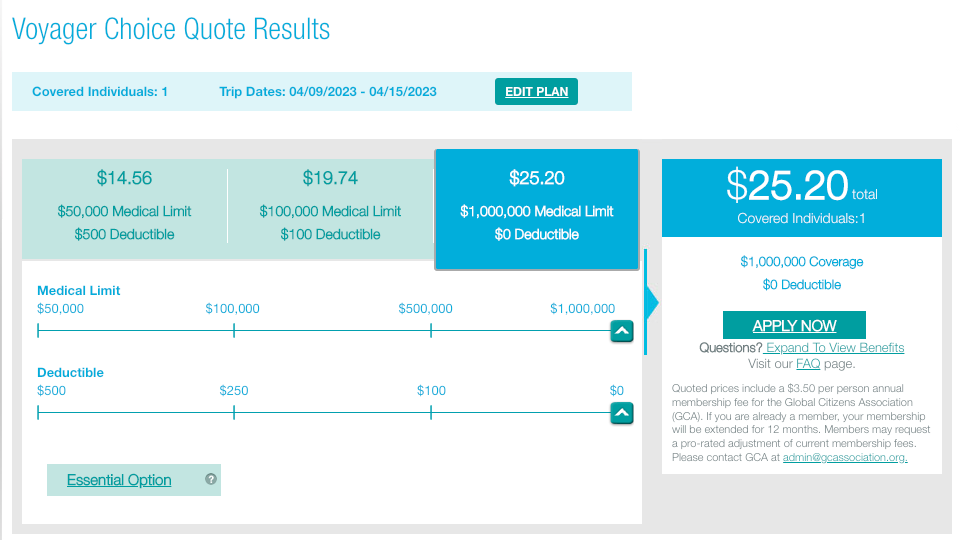

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

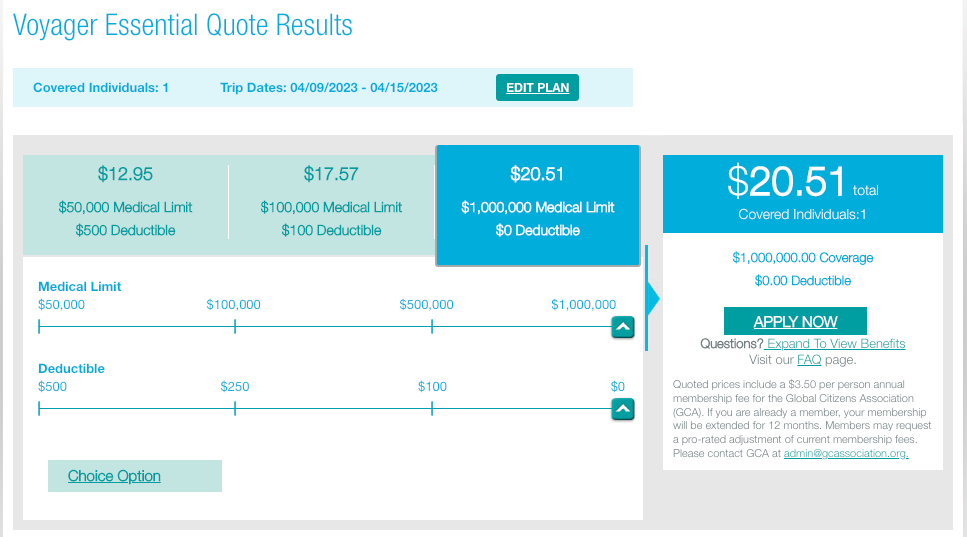

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

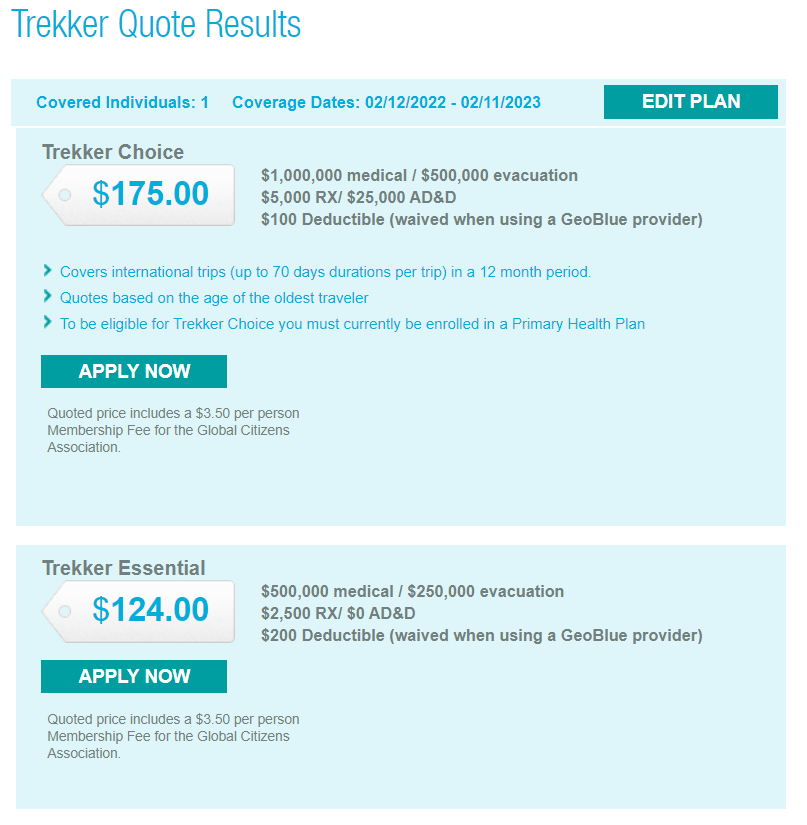

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

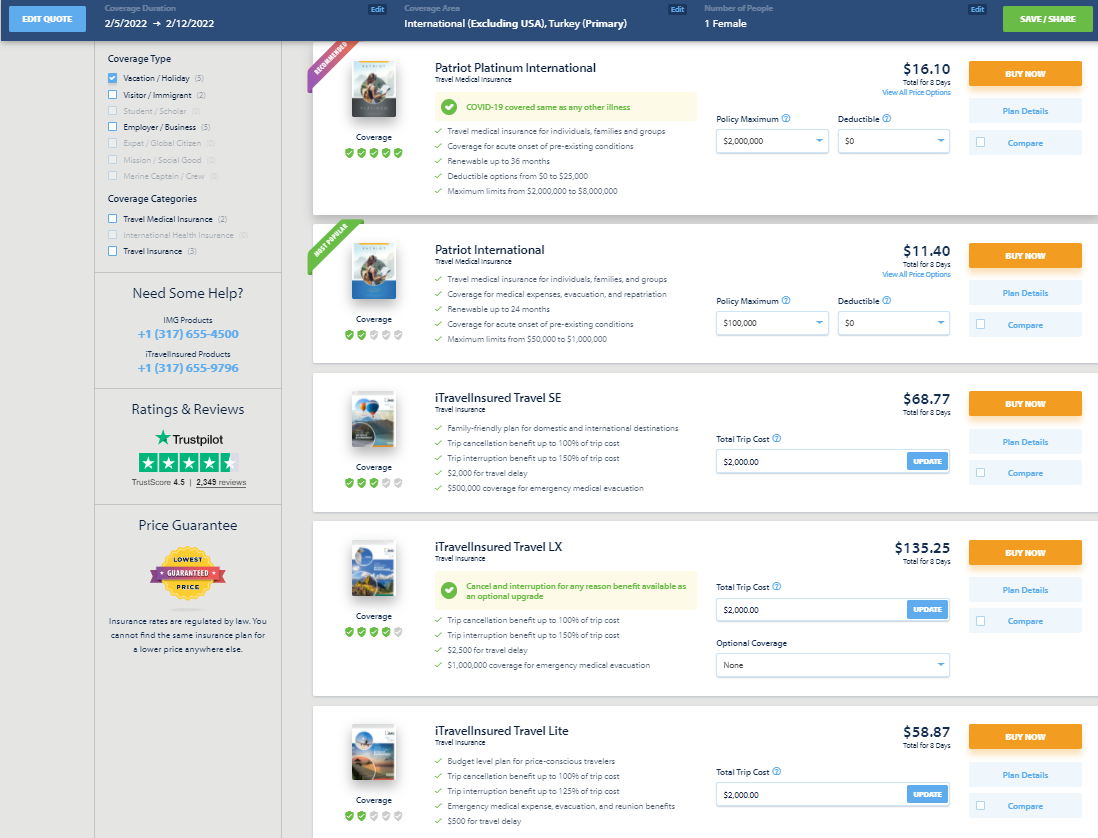

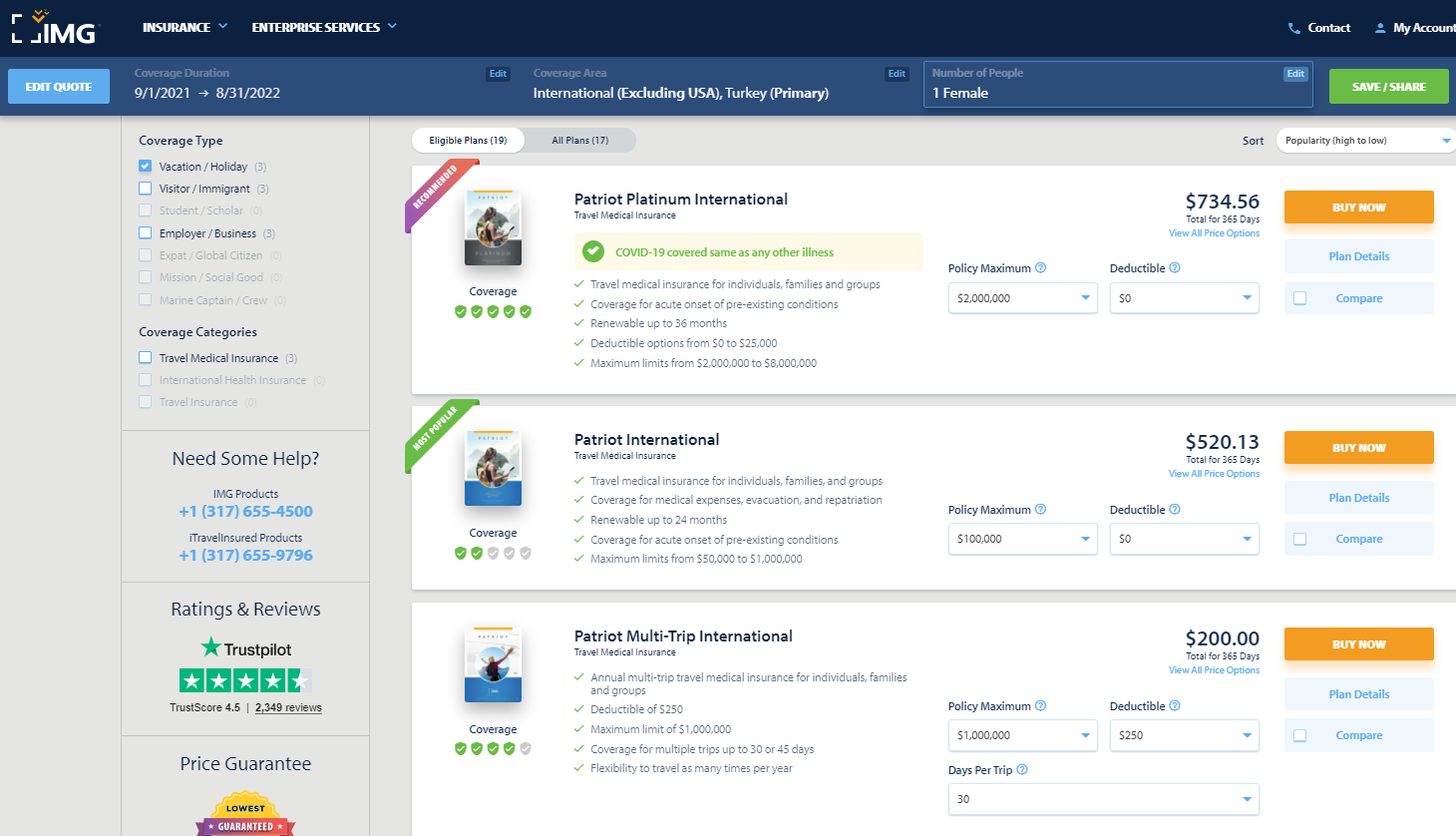

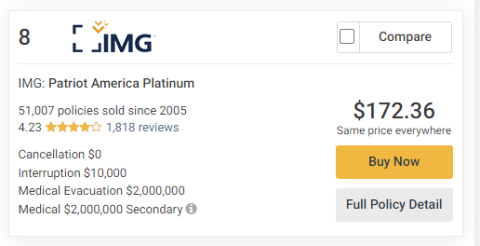

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

Seven Corners

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

- Auto Insurance Best Car Insurance Cheapest Car Insurance Compare Car Insurance Quotes Best Car Insurance For Young Drivers Best Auto & Home Bundles Cheapest Cars To Insure

- Home Insurance Best Home Insurance Best Renters Insurance Cheapest Homeowners Insurance Types Of Homeowners Insurance

- Life Insurance Best Life Insurance Best Term Life Insurance Best Senior Life Insurance Best Whole Life Insurance Best No Exam Life Insurance

- Pet Insurance Best Pet Insurance Cheap Pet Insurance Pet Insurance Costs Compare Pet Insurance Quotes

- Travel Insurance Best Travel Insurance Cancel For Any Reason Travel Insurance Best Cruise Travel Insurance Best Senior Travel Insurance

- Health Insurance Best Health Insurance Plans Best Affordable Health Insurance Best Dental Insurance Best Vision Insurance Best Disability Insurance

- Credit Cards Best Credit Cards 2024 Best Balance Transfer Credit Cards Best Rewards Credit Cards Best Cash Back Credit Cards Best Travel Rewards Credit Cards Best 0% APR Credit Cards Best Business Credit Cards Best Credit Cards for Startups Best Credit Cards For Bad Credit Best Cards for Students without Credit

- Credit Card Reviews Chase Sapphire Preferred Wells Fargo Active Cash® Chase Sapphire Reserve Citi Double Cash Citi Diamond Preferred Chase Ink Business Unlimited American Express Blue Business Plus

- Credit Card by Issuer Best Chase Credit Cards Best American Express Credit Cards Best Bank of America Credit Cards Best Visa Credit Cards

- Credit Score Best Credit Monitoring Services Best Identity Theft Protection

- CDs Best CD Rates Best No Penalty CDs Best Jumbo CD Rates Best 3 Month CD Rates Best 6 Month CD Rates Best 9 Month CD Rates Best 1 Year CD Rates Best 2 Year CD Rates Best 5 Year CD Rates

- Checking Best High-Yield Checking Accounts Best Checking Accounts Best No Fee Checking Accounts Best Teen Checking Accounts Best Student Checking Accounts Best Joint Checking Accounts Best Business Checking Accounts Best Free Checking Accounts

- Savings Best High-Yield Savings Accounts Best Free No-Fee Savings Accounts Simple Savings Calculator Monthly Budget Calculator: 50/30/20

- Mortgages Best Mortgage Lenders Best Online Mortgage Lenders Current Mortgage Rates Best HELOC Rates Best Mortgage Refinance Lenders Best Home Equity Loan Lenders Best VA Mortgage Lenders Mortgage Refinance Rates Mortgage Interest Rate Forecast

- Personal Loans Best Personal Loans Best Debt Consolidation Loans Best Emergency Loans Best Home Improvement Loans Best Bad Credit Loans Best Installment Loans For Bad Credit Best Personal Loans For Fair Credit Best Low Interest Personal Loans

- Student Loans Best Student Loans Best Student Loan Refinance Best Student Loans for Bad or No Credit Best Low-Interest Student Loans

- Business Loans Best Business Loans Best Business Lines of Credit Apply For A Business Loan Business Loan vs. Business Line Of Credit What Is An SBA Loan?

- Investing Best Online Brokers Top 10 Cryptocurrencies Best Low-Risk Investments Best Cheap Stocks To Buy Now Best S&P 500 Index Funds Best Stocks For Beginners How To Make Money From Investing In Stocks

- Retirement Best Gold IRAs Best Investments for a Roth IRA Best Bitcoin IRAs Protecting Your 401(k) In a Recession Types of IRAs Roth vs Traditional IRA How To Open A Roth IRA

- Business Formation Best LLC Services Best Registered Agent Services How To Start An LLC How To Start A Business

- Web Design & Hosting Best Website Builders Best E-commerce Platforms Best Domain Registrar

- HR & Payroll Best Payroll Software Best HR Software Best HRIS Systems Best Recruiting Software Best Applicant Tracking Systems

- Payment Processing Best Credit Card Processing Companies Best POS Systems Best Merchant Services Best Credit Card Readers How To Accept Credit Cards

- More Business Solutions Best VPNs Best VoIP Services Best Project Management Software Best CRM Software Best Accounting Software

- Manage Topics

- Investigations

- Visual Explainers

- Newsletters

- Abortion news

- Coronavirus

- Climate Change

- Vertical Storytelling

- Corrections Policy

- College Football

- High School Sports

- H.S. Sports Awards

- Sports Betting

- College Basketball (M)

- College Basketball (W)

- For The Win

- Sports Pulse

- Weekly Pulse

- Buy Tickets

- Sports Seriously

- Sports+ States

- Celebrities

- Entertainment This!

- Celebrity Deaths

- American Influencer Awards

- Women of the Century

- Problem Solved

- Personal Finance

- Small Business

- Consumer Recalls

- Video Games

- Product Reviews

- Destinations

- Airline News

- Experience America

- Today's Debate

- Suzette Hackney

- Policing the USA

- Meet the Editorial Board

- How to Submit Content

- Hidden Common Ground

- Race in America

Personal Loans

Best Personal Loans

Auto Insurance

Best Auto Insurance

Best High-Yields Savings Accounts

CREDIT CARDS

Best Credit Cards

Advertiser Disclosure

Blueprint is an independent, advertising-supported comparison service focused on helping readers make smarter decisions. We receive compensation from the companies that advertise on Blueprint which may impact how and where products appear on this site. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Blueprint. Blueprint does not include all companies, products or offers that may be available to you within the market. A list of selected affiliate partners is available here .

Travel Insurance

Cheapest travel insurance of April 2024

Mandy Sleight

Heidi Gollub

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

Updated 9:52 a.m. UTC April 11, 2024

- path]:fill-[#49619B]" alt="Facebook" width="18" height="18" viewBox="0 0 18 18" fill="none" xmlns="http://www.w3.org/2000/svg">

- path]:fill-[#202020]" alt="Email" width="19" height="14" viewBox="0 0 19 14" fill="none" xmlns="http://www.w3.org/2000/svg">

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy .

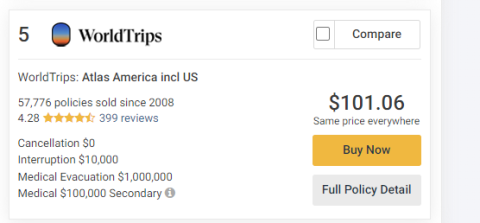

WorldTrips is the best cheap travel insurance company of 2024 based on our in-depth analysis of the cheapest travel insurance plans. Its Atlas Journey Preferred and Atlas Journey Premier plans offer affordable travel insurance with high limits for emergency medical and evacuation benefits bundled with good coverage for trip delays, travel inconvenience and missed connections.

Cheapest travel insurance of 2024

Why trust our travel insurance experts

Our team of travel insurance experts analyzes hundreds of insurance products and thousands of data points to help you find the best travel insurance for your next trip. We use a data-driven methodology to determine each rating. Advertisers do not influence our editorial content . You can read more about our methodology below.

- 1,855 coverage details evaluated.

- 567 rates reviewed.

- 5 levels of fact-checking.

Best cheap travel insurance

Top-scoring plans

Average cost, medical limit per person, medical evacuation limit per person, why it’s the best.

WorldTrips tops our rating of the cheapest travel insurance with two plans:

- Atlas Journey Preferred is the cheaper travel insurance plan of the two, with $100,000 per person in emergency medical benefits as secondary coverage and an optional upgrade to primary coverage. It’s also our pick for the best travel insurance for cruises .

- Atlas Journey Premier costs a little more but gives you $150,000 in travel medical insurance with primary coverage . This is a good option if health insurance for international travel is a priority.

Pros and cons

- Atlas Journey Preferred is the cheapest of our 5-star travel insurance plans.

- Atlas Journey Premier offers $150,000 in primary medical coverage.

- Both plans have top-notch $1 million per person in medical evacuation coverage.

- Each plan offers travel inconvenience coverage of $750 per person.

- 12 optional upgrades, including destination wedding and rental car damage and theft.

- No non-medical evacuation coverage.

Cheap travel insurance for cruises

Travel insured.

Top-scoring plan

Travel Insured offers cheap travel insurance for cruises and its Worldwide Trip Protector plan gets 4 stars in our rating of the best cruise travel insurance .

- Worldwide Trip Protector offers $1 million in emergency evacuation coverage per person and a rare $150,000 in non-medical evacuation per person. It also has primary coverage for travel medical insurance benefits, which means you won’t have to file medical claims with your health insurance first.

- Cheap trip insurance for cruises.

- Offers a rare $150,000 for non-medical evacuation.

- $500 per person baggage delay benefit only requires a 3-hour delay.

- Optional rental car damage benefit up to $50,000.

- Missed connection benefit of $500 per person only available for cruises and tours.

Best cheap travel insurance for families

Travelex has the best cheap travel insurance for families because kids age 17 are covered by your policy for free when they’re traveling with you.

- Free coverage for children 17 and under on the same policy.

- $2,000 travel delay coverage per person ($250 per day) after 5 hours.

- Hurricane and weather coverage after a common carrier delay of any amount of time.

- Only $50,000 per person emergency medical coverage.

- Baggage delay coverage is only $200 and requires a 12-hour delay.

Best cheap travel insurance for seniors

Evacuation limit per person

Nationwide has the best cheap travel insurance for seniors — its Prime plan gets 4 stars in our best senior travel insurance rating. However, Nationwide’s Cruise Choice plan ranks higher in our best cheap travel insurance rating.

- Cruise Choice has a $500 per person benefit if a cruise itinerary change causes you to miss a prepaid excursion. It also has a missed connections benefit of $1,500 per person after only a 3-hour delay, for cruises or tours. But note that this coverage is secondary coverage to any compensation provided by a common carrier.

- Coverage for cruise itinerary changes, ship-based mechanical breakdowns and covered shipboard service disruptions.

- Non-medical evacuation benefit of $25,000 per person.

- Baggage loss benefits of $2,500 per person.

- Travel medical coverage is secondary.

- Trip cancellation benefit for losing your job requires three years of continuous employment.

- No “cancel for any reason” (CFAR) upgrade available.

- Missed connection coverage of $1,500 per person is only for tours and cruises, after a 3-hour delay.

Best cheap travel insurance for add-on options

AIG offers the best cheap travel insurance for add-on options because the Travel Guard Preferred plan allows you to customize your policy with a host of optional upgrades.

- Travel Guard Preferred upgrades include “cancel for any reason” (CFAR) coverage , rental vehicle damage coverage and bundles that offer additional benefits for adventure sports, travel inconvenience, quarantine, pets, security and weddings. There’s also a medical bundle that increases the travel medical benefit to $100,000 and emergency evacuation to $1 million.

- Bundle upgrades allow you to customize your affordable travel insurance policy.

- Emergency medical and evacuation limits can be doubled with optional upgrade.

- Base travel insurance policy has relatively low medical limits.

- $300 baggage delay benefit requires a 12-hour delay.

- Optional CFAR upgrade only reimburses up to 50% of trip cost.

Best cheap travel insurance for missed connections

TravelSafe has the best cheap travel insurance for missed connections because coverage is not limited to cruises and tours, as it is with many policies.

- Best-in-class $2,500 per person in missed connection coverage.

- $1 million per person in medical evacuation and $25,000 in non-medical evacuation coverage.

- Generous $2,500 per person baggage and personal items loss benefit.

- Most expensive of the best cheap travel insurance plans.

- No “interruption for any reason” coverage available.

- Weak baggage delay coverage of $250 per person after 12 hours.

Cheapest travel insurance comparison

How much does the cheapest travel insurance cost?

The cheapest travel insurance in our rating is $334. This is for a WorldTrips Atlas Journey Preferred travel insurance plan, based on the average of seven quotes for travelers of various ages to international destinations with a range of trip values.

Factors that determine travel insurance cost

There are several factors that determine the cost of travel insurance, including:

- Age and number of travelers being insured.

- Trip length.

- Total trip cost.

- The travel insurance plan you choose.

- The travel insurance company.

- Any add-ons, features or upgraded benefits you include in the travel insurance plan.

Expert tip: “In general, travelers can expect to pay anywhere from 4% to 10% of their total prepaid, non-refundable trip costs,” said Suzanne Morrow, CEO of InsureMyTrip.

Is buying the cheapest travel insurance a good idea?

Choosing cheaper travel insurance without paying attention to what a plan covers and excludes could leave you underinsured for your trip. Comparing travel insurance plans side-by-side can help ensure you get enough coverage to protect yourself financially in an emergency for the best price.

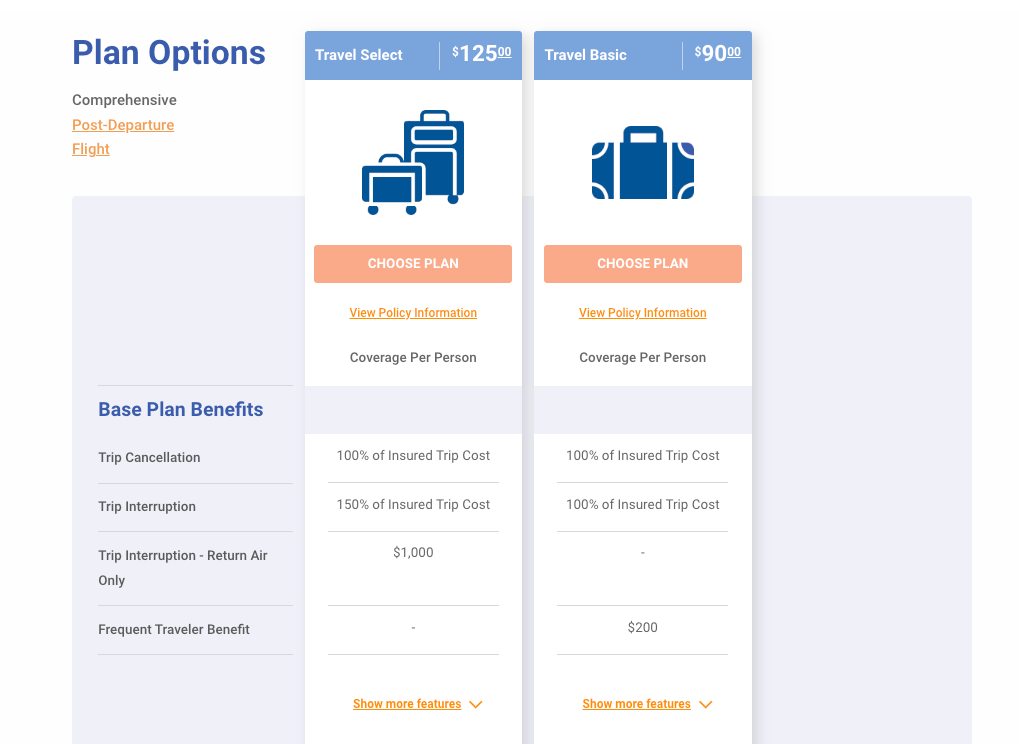

For example, compare these two Travelex travel insurance plans:

- Travel Basic is cheaper but it only provides up to $15,000 for emergency medical expense coverage. You’ll also have to pay extra for coverage for children.

- Travel Select will cost you a bit more but it covers up to $50,000 in medical expenses and includes coverage for kids aged 17 and younger traveling with you. It also offers upgrades such additional medical coverage, “cancel for any reason” (CFAR) coverage and an adventure sports rider that may be a good fit for your trip.

Reasons to consider paying more for travel insurance

Make sure you understand what you’re giving up if you buy the cheapest travel insurance. Here are a few reasons you may consider paying a little extra for better coverage.

- Emergency medical. The best travel medical insurance offers primary coverage for emergency medical benefits. Travel insurance with primary coverage can cost more than secondary coverage but will save you from having to file a claim with your health insurance company before filing a travel insurance claim.

- Emergency evacuation. If you’re traveling to a remote location or planning a boat excursion on your trip, look at travel insurance with a high medical evacuation insurance limit. If you are injured while traveling, transportation to the nearest adequate medical facility could cost in the tens to hundreds of thousands. It may make sense to pay more for travel insurance with robust emergency evacuation coverage.

- Flexibility. To maximize your trip flexibility, you might consider upgrading your travel insurance to “ cancel for any reason” (CFAR) coverage . This will increase the cost of your travel insurance but allow you to cancel your trip for any reason — not just those listed in your policy. The catch is that you’ll need to cancel at least 48 hours before your trip and will only be reimbursed 50% or 75% of your trip expenses, depending on the plan.

- Upgrades. Many travel insurance plans have optional extras like car rental collision and adventure sports (which may otherwise be excluded from coverage). These will cost you extra but may give you the coverage you need.

How to find the cheapest travel insurance

The best way to find the cheapest travel insurance is to determine what you’re looking for in a travel insurance policy and compare plans that meet your needs.

“Travel insurance isn’t one-size-fits-all. Every trip is different, and every traveler has different needs, wants and concerns. This is why comparison is key,” said Morrow.

Consider the following factors when comparing cheap travel insurance plans.

- How often you’re traveling. A single-trip policy may be the most cost-effective if you’re only going on a single trip this year. But a multi-trip travel insurance plan may be cheaper if you’re going on multiple international trips throughout the year. Annual travel insurance policies cover you for a whole year as long as each trip doesn’t exceed a certain number of days, usually 30 to 90 days.

- Credit card has travel insurance benefits. The best credit cards offer perks and benefits, and many offer travel insurance-specific benefits. The coverage types and benefit limits can vary, and you must put the entire trip cost on the credit card to use the coverage. If your trip costs more than the coverage limit on your card, you can supplement the rest with a cheaper travel insurance plan.

- The coverage you need. When looking for the best travel insurance option at the most affordable price, only buy extras and upgrades you really need. A basic plan may only provide up to $500 in baggage insurance, but if you only plan to take $300 worth of clothes and accessories, you don’t need to pay more for higher coverage limits.

Is cheap travel insurance worth it?

Cheap travel insurance can be worth it, as long as you understand the plan limitations and exclusions. Taking the time to read your policy, especially the fine print, well before your trip can ensure there won’t be any surprises about what’s covered once your journey begins.

“If a traveler is looking for coverage for travel delays, cancellations, interruptions, medical and baggage — a comprehensive travel insurance policy will provide the most bang for their buck,” said Morrow. But if you’re on a tight budget and are only worried about emergency medical care and evacuation coverage while traveling abroad, stand-alone options are cheaper.

Before buying travel insurance, you should also consider what your health insurance will cover.

“Most domestic health insurance plans, including Medicare, will not cover medical bills abroad,” said Morrow. Even if you’re staying stateside, you may find value in an affordable travel insurance plan with medical coverage if you have a high-deductible health plan (HDHP).

A cheap travel insurance plan is better than none at all if you end up in a situation that would have covered some or all of your prepaid, nonrefundable trip expenses.

Methodology

Our insurance experts reviewed 1,855 coverage details and 567 rates to determine the best travel insurance . From those top-scoring travel insurance plans, we chose the most affordable for our rating of the cheapest travel insurance.

Insurers could score up to 100 points based on the following factors:

- Cost: 40 points. We scored the average cost of each travel insurance policy for a variety of trips and traveler profiles.

- Medical expenses: 10 points. We scored travel medical insurance by the coverage amount available. Travel insurance policies with emergency medical expense benefits of $250,000 or more per person were given the highest score of 10 points.

- Medical evacuation: 10 points. We scored each plan’s emergency medical evacuation coverage by coverage amount. Travel insurance policies with medical evacuation expense benefits of $500,000 or more per person were given the highest score of 10 points.

- Pre-existing medical condition exclusion waiver: 10 points. We gave full points to travel insurance policies that cover pre-existing medical conditions if certain conditions are met.

- Missed connection: 10 points. Travel insurance plans with missed connection benefits of $1,000 per person or more received full points.

- “Cancel for any reason” upgrade: 5 points. We gave points to travel insurance plans with optional “cancel for any reason” coverage that reimburses up to 75%.

- Travel delay required waiting time: 5 points. We gave 5 points to travel insurance policies with travel delay benefits that kick in after a delay of 6 hours or less.

- Cancel for work reasons: 5 points. If a travel insurance plan allows you to cancel your trip for work reasons, such as your boss requiring you to stay and work, we gave it 5 points.

- Hurricane and severe weather: 5 points. Travel insurance plans that have a required waiting period for hurricane and weather coverage of 12 hours or less received 5 points.

Some travel insurance companies may offer plans with additional benefits or lower prices than the plans that scored the highest, so make sure to compare travel insurance quotes to see your full range of options.

Cheapest travel insurance FAQs

When buying travel insurance, cheapest is not always the best. The most affordable travel insurance plans typically offer fewer coverages with lower policy limits and few or no optional upgrades. Add up your total nonrefundable trip costs and compare travel insurance plans and available features that cover your travel expenses. This strategy can help you find the cheapest travel insurance policy that best protects you from financial loss if an unforeseen circumstance arises.

Get the coverage you need: Best travel insurance of 2024

According to our analysis, WorldTrips , Travel Insured International and Travelex offer the best cheap travel insurance. Policy coverage types and limits can vary by each travel insurance provider, so the best way to get the cheapest travel insurance plan is to compare several policies and companies to find the right fit for your budget.

A good rate for travel insurance depends on your budget and coverage needs. The most comprehensive travel insurance plan is usually not the cheapest. But cheap trip insurance may not have enough coverage or the types of coverage you want. Comparing different levels of coverage and how much they cost can help you find the best cheap insurance for travel.

The average cost of travel insurance is between 5% to 6% of your total travel expenses for one trip, according to our analysis of rates. However, you may find cheaper travel insurance if you opt for a plan with fewer benefits or lower coverage limits. How much you pay for travel insurance will also depend on the number of travelers covered, their ages, the length of the trip and any upgrades you add to your plan.

Travel insurance covers nonrefundable, prepaid trip costs — up to the policy coverage limits — when your trip is interrupted or canceled for a covered reason outlined in your plan documents. Even the cheapest travel insurance policies usually provide coverage for:

- Medical emergencies.

- Trip delays.

- Trip interruption.

- Trip cancellation.

- Lost, stolen or damaged luggage.

However, if you’re looking to save on travel insurance, you can shop for a policy that only has travel medical insurance and does not include benefits for trip cancellation .

Even when you buy cheap travel insurance, you can often use upgrade options to customize your policy to meet your specific needs.

Some common travel insurance add-ons you may want to consider include:

- Rental car damage coverage.

- Medical bundle.

- Security bundle.

- Accidental death and dismemberment coverage.

- Adventure sports bundle.

- Pet bundle.

- Wedding bundle.

- “Cancel for work reasons” coverage.

- “Interruption for any reason” (IFAR) coverage.

- “Cancel for any reason” (CFAR) coverage .

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy . The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.

Mandy is an insurance writer who has been creating online content since 2018. Before becoming a full-time freelance writer, Mandy spent 15 years working as an insurance agent. Her work has been published in Bankrate, MoneyGeek, The Insurance Bulletin, U.S. News and more.

Heidi Gollub is the USA TODAY Blueprint managing editor of insurance. She was previously lead editor of insurance at Forbes Advisor and led the insurance team at U.S. News & World Report as assistant managing editor of 360 Reviews. Heidi has an MBA from Emporia State University and is a licensed property and casualty insurance expert.

10 worst US airports for flight cancellations this week

Travel Insurance Heidi Gollub

AXA Assistance USA travel insurance review 2024

Travel Insurance Jennifer Simonson

10 worst US airports for flight cancellations last week

Average flight costs: Travel, airfare and flight statistics 2024

Travel Insurance Timothy Moore

John Hancock travel insurance review 2024

HTH Worldwide travel insurance review 2024

Airfare at major airports is up 29% since 2021

USI Affinity travel insurance review 2024

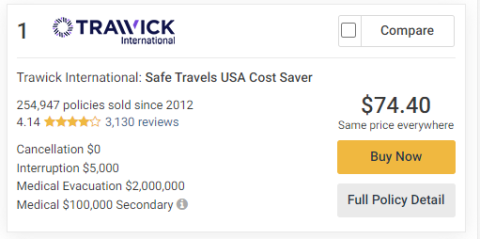

Trawick International travel insurance review 2024

Travel insurance for Canada

Travel Insurance Mandy Sleight

Travelex travel insurance review 2024

Best travel insurance companies of April 2024

Travel Insurance Amy Fontinelle

Best travel insurance for a Disney World vacation in 2024

World Nomads travel insurance review 2024

Outlook for travel insurance in 2024

12 Best Travel Insurance Policies and Why You Need Them

By Suzanne Rowan Kelleher

Condé Nast Traveler has partnered with CardRatings for our coverage of credit card products. Condé Nast Traveler and CardRatings may receive a commission from card issuers. We don't review or include all companies, or all available products. Moreover, the editorial content on this page was not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are entirely those of Condé Nast Traveler's editorial team.

You’ve purchased your flights and booked your hotel. Now, what about travel insurance? These days, it’s easy to add coverage to your trip, but what's the best travel insurance policy to buy? And is the extra cost always necessary?

When planning a trip, nobody loves imagining worst-case scenarios and everyone has a different risk tolerance. For a weekend road trip , you may be willing to cross your fingers and suck up your losses should something go awry. But what if you’re shelling out for a longer, more complex and more expensive trip? You’ll likely want peace of mind when your risk and financial investment are greater.

When do you need travel insurance?

There’s nothing like bad luck to turn you into an insurance evangelist. For travel writer Katherine Fan, the epiphany came after a thunderstorm disrupted her flight in Chicago . “My bags didn't make it to Italy for more than five days, and my travel insurance covered all the costs for replacement items as well as the alternative transportation I had to rebook because of the delay,” she says. “I'll never live without it now.”

In general, the older you are and the more remote your destination, the more crucial it is to buy travel insurance. Lou Desiderio, a communications executive from Long Island, New York, recalls the time his octogenarian father became ill during a European cruise , and doctors recommended that his parents return home immediately. His parents’ travel insurance covered the lion’s share of the $9,500 they subsequently racked up in medical costs, ground transportation, flights, hotel, and meals. “You always wonder if the cost of insurance is worth it,” says Desiderio. “In this instance, it was absolutely worth it.”

“Not all domestic health and medical insurance plans will follow you outside your home country,” says Justin Tysdal, CEO of Seven Corners , a travel insurance provider. “Something as simple as twisting your ankle in a foreign country may not be covered and could result in expensive medical bills.”

Simply having travel insurance can have side benefits, too. “One of the best hidden perks is the 24/7 global travel assistance provided by the plan,” says Stan Sandberg, CEO of TravelInsurance.com . The hotline can be helpful in dealing with a multitude of unexpected issues, from currency conversion or cash transfers to replacing passports or IDs to finding a local physician.

Where can you find a good policy?

Travel agencies, airlines, cruise lines, and tour operators often offer an optional insurance add-on, but these plans tend to have been run through the company’s legal team and contain more exclusions. Travel rewards credit cards also offer some built-in insurance benefits to their cardholders, like trip cancellation coverage, delayed baggage coverage, and trip interruption and delay coverage. But you’ll often be better served by a plan from a third-party insurer, which tend to offer more holistic plans.

The good news is that it has never been easier to buy exactly the type of travel insurance you need at a reasonable price. Most people buy comprehensive insurance for a single trip, but annual travel insurance plans that cover multiple trips in a one-year period are becoming more popular.

You can find some of the best travel insurance policies by visiting an insurance comparison site like TravelInsurance.com, InsureMyTrip.com or SquareMouth.com . Plug in your trip details and you’ll get instant quotes for multiple insurance plans that you can compare on price, coverage limitations, and other parameters. Be sure to read the policy details, as inclusions can vary from plan to plan but will end up making all the difference to your particular needs.

What’s it going to cost?

The cost of travel insurance depends on a variety of factors, including the price and length of the trip, your age, destination, and any optional add-ons. For your average domestic or international trip with flights and hotels , expect to pay anywhere from 3 to 7 percent of your trip’s cost, depending on inclusions.

So for a $2,000 trip, you might expect a typical comprehensive plan with trip cancellation, interruption, and delay, along with baggage loss and delay, and emergency medical coverage and evacuation to cost in the $100 ballpark. Some upgrades, like a “cancel for any reason” provision, will cost more.

When should you buy travel insurance?

Don’t procrastinate. “Some benefits and coverages are available only if you’ve purchased your policy within a short window, typically seven to 21 days from when you make the first payment towards your trip,” says Sandberg. Buy early and you may qualify for a pre-existing condition waiver or a ‘cancel for any reason’ upgrade.

It’s especially important not to delay buying travel insurance if you’re traveling to, say, the Caribbean during hurricane season. Once a major storm has been named, the window of opportunity slams shut, and you can no longer buy insurance for that hurricane. “If you purchase a policy after a storm is named, trip cancellation and trip interruption are excluded from coverage,” says Sandberg.

What’s not covered?

“Some people believe that a travel insurance plan is designed to give you the flexibility to cancel your trip for any reason whatsoever,” says Sandberg. “But the standard plan is not going to provide cancellation coverage for a change of heart or a relationship break-up or an outbreak of Zika in your destination.” If you need that flexibility, opt for the ‘cancel for any reason’ upgrade.

“As far as medical coverage, people often believe a travel insurance plan will cover preventative services such as immunizations and annual check-ups,” says Tysdal. “But travel insurance is intended to cover illnesses and injuries that originate during a trip, and that’s why it’s relatively inexpensive.” Be careful about overindulging, too. “If you injure yourself as a result of being intoxicated beyond a legal limit, your travel insurance policy will not likely cover you,” says Sandberg. Ditto for drug use.

How easy is it to file a claim?

“Documentation is key,” says Meghan Walch, product manager for InsureMyTrip. If luggage is lost or items are stolen, file a report with the airline or police. You may need to provide original receipts for the stolen items in order to receive reimbursement up to the policy limits.“ Also, be aware that baggage coverage only offers coverage up to a set amount,” says Walch. “So, if you are carrying, say, a fancy $3,000 Nikon or Canon camera , you’ll likely need to buy additional insurance elsewhere or cover it under a homeowner's policy.” Note, also, that many plans specifically exclude computers and electronics.

What about car rental insurance?

It’s often possible to add car rental insurance, also known as the Collision Damage Waiver (CDW), to a comprehensive travel insurance plan, which can save you from a serious headache should you get into an accident while driving. “But the biggest mistake people make when renting a car is to waste money on duplicate coverage,” says Jonathan Weinberg, CEO of AutoSlash , the car rental deal-finding site. “The reality is that if you own your own vehicle and have car insurance, you are likely already covered when renting in the U.S.”

Anna Borges

Jessica Puckett

Karthika Gupta

And if you don’t own a car? “Your credit card may also cover you when renting,” says Weinberg. “It's always important to check to be sure, but why pay again for coverage you already have?” Indeed, paying for your rental with the right travel rewards credit card might cover your collision insurance, with some policies covering damage up to the value of the car. Travel outside the U.S. and Canada , though, and it’s a different story. “Most personal auto insurance policies will not cover a claim for damage to a rental outside the U.S. or Canada,” says Weinberg. “Likewise, different credit cards have different exclusions when it comes to covering damage to a rental car in a foreign country.”

Types of travel insurance

Most travelers opt for a comprehensive plan, but you should know what each type of coverage does, so you’ll know if a package truly fits your needs. Here’s a brief rundown of the main types of coverage.

Trip protection

Often known simply as “travel insurance,” this type of comprehensive package is the most common purchase.

Commonly covers: Reimbursement for money spent on your trip due to cancellations, interruptions, and delays; medical expenses if you become sick or injured and, if necessary, emergency medical evacuation and repatriation; and coverage for your belongings if lost, stolen, damaged, or delayed.

How to get it: Compare plans at Square Mouth , Seven Corners , InsureMyTrip.com , and TravelInsurance.com

Trip cancellation

This benefit can reimburse 100 percent of your trip cost—flights, hotels, cruises, and pre-paid activities—if you need to cancel for a covered reason.

Commonly covers: Unforeseen illness or injury; the death of you, a family member, or a traveling companion; terrorism; inclement weather; natural disasters.

Fine print: Some policies also include other covered reasons, such as jury duty or an employment layoff.

Trip interruption

You’ll be reimbursed for your costs if your trip is interrupted for a covered reason. The payout may exceed the total trip cost if you need to incur additional expenses to return home, but some policies limit coverage to a return flight home.

How to get it: Signing up for travel rewards cards like the Chase Sapphire Reserve can automatically give you this coverage for all trips booked on the card.

Learn more about signing up for the Chase Sapphire Reserve here .

Cancel for any reason

This upgrade provides reimbursement for 50 to 75 percent of prepaid and non-refundable trip payments if you cancel a trip for any reason not otherwise covered by your policy.

Watch out: You’ll be required to insure your trip’s entire cost, which will typically increase your premium by roughly 40 percent.

Fine print: Typically available for purchase up to seven to 21 days from the date you make your initial trip deposit. You must cancel the entire trip at least two to three days before your departure date.

Travel delay

If your trip is unexpectedly delayed by a designated amount of time (typically three to 12 hours, depending on the policy), this benefit provides a per-diem dollar amount (typically $150 to $200) that can be used for meals, hotels, and other necessary expenses during the delay.

Commonly covers: Inclement weather and mechanical breakdowns of “common carriers,” meaning public transportation such as planes, trains, or buses.

How to get it: Signing up for travel rewards cards like the Chase Sapphire Reserve can automatically give you this coverage for all trips booked on the card that meet the requirements.

Missed connection

You’ll be reimbursed for additional costs for you to catch up to your trip if you miss your departure due to a common carrier delay of a specified amount of time. It's usually an added feature of larger insurance packages.

Commonly covers: Inclement weather and mechanical breakdowns of common carriers.

Watch out: Some policies only reimburse if you need to catch up to a cruise or tour. Since the wording typically specifies public transportation delays, you would be out of luck if you’re driving and miss your connection because you got caught in traffic.

Baggage and personal items loss

You’ll be covered for lost, stolen, or damaged luggage. Expect limits in both overall coverage and per-item coverage. It's included with many travel rewards credit card benefits.

Watch out: While most policies cover your personal belongings throughout the entire trip, some will only cover luggage while it is checked with an airline or transportation carrier.

Baggage delay

If your luggage is delayed for a specified period of time—typically 12 or 24 hours—this coverage will reimburse you for any clothing, toiletries, and other essential items you need to purchase. Expect a maximum coverage amount per person, as well as a daily limit. It's also included as a cardholder benefit with many travel credit cards.

Emergency medical coverage

This covers the costs to treat a medical emergency, including treatment, hospitalization, and medication. This type of coverage is highly recommended for international trips and cruises.

Watch out: You would pay for medical care out-of-pocket, and then file a claim for reimbursement when you return home. In certain situations, an insurer might pre-authorize payment of medical bills, but it is not guaranteed.

How to get it: Browse medical coverage plans at Seven Corners .

Emergency evacuation coverage

This coverage is for transportation to the nearest medical facility in the event of a medical emergency during your trip. It's usually an add-on to larger medical coverage.

Commonly covers: If the treating physician recommends that you should return home for further medical attention, this benefit can also cover those transportation expenses. In the case of a death, repatriation can transport a traveler’s remains back home. It's usually an add-on to a larger travel insurance policy.

Pre-existing medical conditions waiver

Most policies have built-in exclusions for pre-existing conditions. So if you’ve been seriously ill in the past or need ongoing treatment, consider looking for a plan that offers a pre-existing condition exclusion waiver.

Fine print: You’ll need to purchase the plan within a few weeks from the date you make your initial trip payment.

Hazardous/adventure sports coverage

Are you an adrenaline junkie? Adventure activities such as heli-skiing, off-trail snowboarding, bungee jumping, wakeboarding, Jet Skiing, spelunking, rock climbing, and scuba diving are almost always excluded from coverage in most travel insurance plans.

Fine print: You can buy coverage as an optional upgrade, which is an especially smart bet if you’re planning an adventure trip outside the United States.

Condé Nast Traveler has partnered with CardRatings for our coverage of credit card products. Condé Nast Traveler and CardRatings may receive a commission from card issuers.

By signing up you agree to our User Agreement (including the class action waiver and arbitration provisions ), our Privacy Policy & Cookie Statement and to receive marketing and account-related emails from Traveller. You can unsubscribe at any time. This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

- Hotels & Resorts

- Travel Guides

- Credit Cards

- Airplane Seat Switch Etiquette

- American Airlines Baggage Fees & Allowance

- Amex Centurion Lounges

- Best & Worst Days to Fly

- Best & Worst Days to Fly & Travel for Christmas & New Year's 2024

- Best & Worst Times to Fly

- Best Days & Times to Book Flights

- Best Seats On a Plane

- Best Websites to Book Cheap Flights

- Capital One Lounges

- Chase Sapphire Lounges

- Delayed, Lost, or Damaged Luggage (Steps to Take)

- Delta Baggage Fees & Allowance

- How to Avoid Airline Flight Delays & Cancellations in 2024

- How to Cancel an American Airlines Flight

- How to Cancel a Delta Air Lines Flight

- How to Earn Delta SkyMiles

- How to Earn United MileagePlus Miles

- How to Find Cheap Flight Deals

- How to Find Cheaper Summer Flights for 2024

- How to Get Through TSA Airport Security Faster

- How to Use Google Flights

- When to Book Christmas Flights - Best Travel Days for 2024

- When to Book Thanksgiving Flights - Best Travel Days for 2024

- United Airlines Baggage Fees & Allowance

- What to Do if Your Airline Cancels or Delays Your Flight

- Worst Seats on a Plane

- Best Atlanta Airport Car Rental Companies

- Best Denver Airport Car Rental Companies

- Best Los Angeles Airport (LAX) Car rental Companies

- Best Miami Airport Car Rental Companies

- Best Orlando Airport Car Rental Companies

- Best Phoenix Airport Car Rental Companies

- Best Websites to Book Cheap Car Rentals

- How to Find Cheap Car Rentals

- Best All-Inclusive Cruise Lines

- Can You Bring Food, Alcohol, & Snacks on a Cruise Ship?

- Best Websites to Book Cheap Cruises

- Where Can I Cruise Without a Passport?

- What is Cruise Ship Tendering?

- What is Port Side on a Cruise Ship?

- Best Economy & Budget-Friendly Hotel Brands

- Best Mid-Tier Hotel Brands

- Best Websites to Book Cheap Hotels

- Choice Privileges Loyalty Program Review

- Hilton Honors Loyalty Program Review

- Hostel Booking Tips

- Hotels.com Booking Guide

- How to Find Cheap Hotel Deals

- IHG One Rewards Loyalty Program Review

- Marriott Bonvoy Loyalty Program Review

- World of Hyatt Loyalty Program Review

- Wyndham Rewards Loyalty Program Review

- Best Travel Products

- Destinations

- Family Travel

- Beach Vacation Packing List

- Best Beaches in Florida

- Best Ticket Websites for Tours & Activities

- Best Travel Tips

- Global Entry Program Guide

- How to Check Your Passport Application Status

- How to Make a Travel Budget

- How to Take Your Own Passport Photo at Home

- Passport Processing Times - Current Wait in 2024

- Summer Travel Survey & Trends 2024

- Sustainable Travel Survey 2023

- TSA PreCheck Program Guide

- Travel Insurance Buying Guide

- Ultimate Travel Packing List

- Travel Credit Card Reviews

- Travel Credit Card Strategies & Tips

- Amex Platinum Card Benefits

- Amex Gold Card Benefits

- Best Starter Travel Credit Cards for Beginners

- Capital One Venture Card Benefits

- Capital One Venture X Card Benefits

- Chase Sapphire Preferred Card Benefits

- Chase Sapphire Reserve Card Benefits

- How to Use CardMatch

- Ink Business Unlimited Card Benefits

Get The Vacationer Newsletter

Get highlights of the most important news delivered to your email inbox

Advertiser Disclosure

Amazon Affiliate Disclosure : Jones-Dengler Marketing, LLC via The Vacationer is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for us to earn fees by linking to Amazon.com and affiliated sites. As an Amazon Associate we earn from qualifying purchases. Amazon and the Amazon logo are trademarks of Amazon.com, Inc. or its affiliates.

The Vacationer • Travel Guides • Travel Insurance

The Best Travel Insurance – Guide to the Top Companies, Cost, & Buying Tips in 2024

When taking any trip, travel insurance can be a beneficial tool to protect yourself if your travels don’t go as planned. Without travel insurance, you may lose money and be upset. The good news is there are many travel insurance options available to purchase. You may even have some travel protections in place if you use travel credit cards to pay for your travel reservations. This guide will help you understand the best travel insurance options, so you know how to better protect yourself before your next trip. Before reading, feel free to check out: World Nomads , InsureMyTrip , and TravelInsurance.com

Table of Contents

What is Travel Insurance?

You’ve probably heard of travel insurance before, but you may still be confused as to what exactly it is. Travel insurance covers unforeseen losses when traveling.

Each policy is different and covered incidents vary greatly. This type of insurance can help you minimize the financial risks associated with traveling. If you get sick, have to cancel your trip due to a covered incident, or experience significant delays, your insurer will provide reimbursement for eligible non-refundable travel costs or provide reimbursement for additional purchases you needed to make as a result of your covered incident.

As you look into insurance options, be sure to carefully review policy details to understand what your insurance includes. There may be exclusions, and you don’t want to unexpectedly find out that you’re not covered after you purchase a policy.

What Types of Travel Insurance Are Available?

There are different types of travel insurance. Knowing more about the different types available can help you choose the right coverage for your needs. Here are some examples:

Trip delay: Lengthy travel delays can happen. If you’re traveling and experience delays covered by this type of insurance, you may be eligible for reimbursement for costs associated with the delay, such as lodging and meals. This type of insurance usually requires that you’re delayed for at least a set amount of hours or requires that the delay results in an overnight stay.

Trip interruption: If you’re forced to cut your trip short or your trip is extended for a covered reason, having trip interruption insurance may be helpful. Prepaid travel costs and extra expenses that occur may be reimbursed. The interruption must be for a covered event.

Trip cancellation: If you must cancel your trip before you leave, trip cancellation may cover prepaid non-refundable travel costs.

Baggage protection: Baggage protection may cover lost, delayed, or stolen baggage. If you qualify for a covered event, your insurance may reimburse for reasonable purchases that you needed to make while your baggage was lost or delayed or may offer reimbursement for stolen items. Baggage insurance policies may vary, so be sure to check coverage terms. Further Reading: What Should I Do If My Luggage is Delayed, Lost or Damaged by My Airline?

Travel medical insurance: This kind of travel insurance can help you get the medical care you need when traveling abroad. Your health insurance from home may not cover care in another country. If you have this coverage and an eligible claim, your insurance may reimburse you for medical costs you pay while abroad.

Emergency medical evacuation: If you’re traveling in an area without adequate medical care or hospitals that can meet your care needs, you may need to be transported elsewhere. Emergency medical evacuation coverage can cover transit to another medical center or hospital for a severe medical emergency.

Accidental death and dismemberment insurance (also called travel accident insurance): Serious accidents can happen when traveling. This type of insurance coverage pays out benefits when a covered person dies or is dismembered—for example, loss of eyesight, loss of a limb, or death.

Rental car coverage: Some policies offer rental car coverage that provides reimbursement for damage or theft that occurs to your rental car for eligible claims. Some policies cover rental cars abroad, but some don’t. Liability insurance is usually not included.

Comprehensive travel insurance: This type of insurance offers a range of travel protections all in one policy. Instead of purchasing individual coverage, this kind of plan may be best.

Cancel for any reason coverage: If you want to be able to cancel your trip no matter what, you may want to look for a policy that includes ‘cancel for any reason’ coverage. These insurance policies are best if you need complete flexibility.

24-Hour assist: Some travel insurance policies include 24-hour assist. If you need help rebooking flights, finding lost luggage, or scheduling an appointment with a local doctor, you can contact this hotline to get assistance.

Will Travel Insurance Protect Me During COVID-19?