- Meetings & Conventions

- Travel Trade

(0) items in your itinerary

Vancouver's Tax & Fee Structure

- Helpful Tips & Resources

- Vancouver's Tax Structure

Vancouver's Tax & Fee Structure

Tax on short-term accomodation in vancouver.

Short-term accommodation in the City of Vancouver includes hotels, as well as to Airbnb, VRBO and all online marketplace facilitators.

The total rate in Vancouver (as of February 2023) is 20% of the room rate, consisting of:

8% Provincial Sales Tax (PST)

3% Municipal & Regional District Tax (MRDT), which most major cities in BC collect.

2.5% Major Event MRDT. On Feb 1, 2023, a temporary Major Events MRDT over seven years was introduced and in effect until Jan 31, 2030.

1.5% Destination Marketing Fee (DMF) . Most downtown Vancouver hotels collect this fee to assist with the marketing of Vancouver as a destination.

5% Goods & Services Tax (GST) on the total purchase price

Airbnb, VRBO and all online marketplace facilitators

2.5% Major Event MRDT. On Feb 1, 2023, a temporary Major Events MRDT over seven years was introduced and in effect until Jan 31, 2030.

Additional charges may include guest services fees and guest cleaning fees.

SALES TAX IN BRITISH COLUMBIA

Most goods and services in British Columbia are subject to a sales tax totaling 12% of the purchase price (7% PST + 5% GST). Please note that alcohol is taxed at 15% (10% PST + 5% GST).

visit gov.bc.ca for more information [link to https://www2.gov.bc.ca/gov/content/taxes]

Customs Brokers

Visa and entry requirements, weather in vancouver.

- Member Newsletter

- News Centre

- Pay Your Fees

This website uses cookies. For more information, click here .

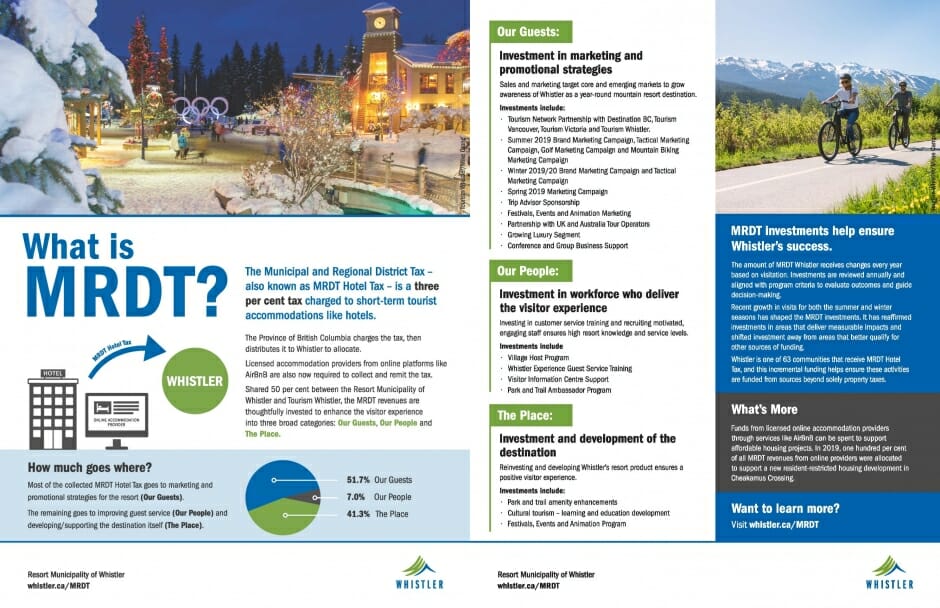

Municipal and Regional District Tax

The Municipal and Regional District Tax (MRDT) is a tax of up to three per cent (3%) on the purchase of short-term tourist accommodation imposed in specific geographic areas of British Columbia (designated accommodation areas) on behalf of municipalities, regional districts or eligible entities.

The MRDT program – sometimes referred to as the Hotel Tax - was originally introduced by the Provincial Government in 1987 to raise revenues for local tourism marketing, programs, and projects. MRDT is paid by visitors (not residents or Members) when they book accommodation and it is collected by the accommodation sector.

In Whistler, the MRDT funds are received by the Resort Municipality of Whistler (RMOW) and then shared with Tourism Whistler based on a number of agreements. Revenues are reinvested by both organizations on behalf of the destination. Expenditures are approved by, and reported back to, the Province to ensure ongoing alignment with the prescribed purposes of the tax as outlined in the Provincial Sales Tax Act.

More information about how MRDT is collected and invested in Whistler is available on the RMOW’s website at whistler.ca/mrdt .

- Review the 2023-2027 MRDT Whistler Five-Year Strategic Plan

- Review the 2018-2022 MRDT Whistler Five-Year Strategic Plan

Additional information about the provincial MRDT program is available on Destination BC’s website .

How are the MRDT funds spent in Whistler?

In Whistler, the MRDT funds are primarily invested into a mix of product reinvestment and enhancement, service delivery and leisure marketing and sales initiatives. Investment examples in 2022 include:

Marketing Campaigns

- Summer 2022 Golf Campaign

- Festival & Events Campaign (e.g. Gran Fondo, Cornucopia, Whistler Film Festival)

Conference Centre Initiatives

- Attendance at industry-related events

- Execution of familiarization trips for meeting planners

- Targeted sales initiatives directed at filling midweek and shoulder season periods

Investment in Affordable Housing Initiatives

- Construction of employee-restricted housing in Cheakamus Crossing

Planning, Investing & Development of Whistler

- Park and amenity upkeep and signage

- Valley Trail enhancements and connections

- Parks Masterplan Project

- Bylaw support and Goose Management

- Investments in third-party festivals and events

Investment in the Workforce Who Deliver the Visitor Experience

- Village Host Program

- Whistler Experience Guest Service Training (in partnership with the Whistler Chamber of Commerce)

- Visitor Information Centre Support

- Park and Trail Ambassador Program

- About Tourism Whistler

- Manage Your Membership

- Member Tools & Resources

- Visitor Servicing

- Research & Insights

- Whistler Inside Scoop

- Health & Safety Information

- Value of Tourism

- Whistler's Place Brand

- Destination Stewardship

- Planning, Strategy & Results

- Board of Directors

- Annual General Meeting

- Corporate Documents

- Membership Overview

- Become A Member

- Pay Membership Fees

- Maintain Your Business Listing

- List Your Rental Property

- Member Forms

- Fee Information Request

- Real Estate & Clients

- Underused Housing Tax

- Member Opportunities

- Member Meetings

- Seasonal Marketing Campaigns

- Promotional Tools

- Messaging Toolkits

- Business Planning

- Destination Experience & Opportunities

- Emergency Preparedness

- Submit Member Feedback

- Visitor Servicing Information

- Whistler Business Directory

- Online Interactive Map

- Ask Whistler

- Go Whistler Tours

- Submit Visitor Feedback

- Research Overview

- Performance & Forecasting Data

- Survey & Visitor Insights

- Skip to main content

- Skip to main navigation

- Skip to site search

- Skip to side bar

- Skip to footer

BC Gov News

- News Archive

- Live Webcast

- Office of the Premier

- Agriculture and Food

- Attorney General

- Children and Family Development

- Citizens' Services

- Education and Child Care

- Emergency Management and Climate Readiness

- Energy, Mines and Low Carbon Innovation

- Environment and Climate Change Strategy

- Indigenous Relations and Reconciliation

- Intergovernmental Relations Secretariat

- Jobs, Economic Development and Innovation

- Mental Health and Addictions

- Municipal Affairs

- Post-Secondary Education and Future Skills

- Public Safety and Solicitor General

- Social Development and Poverty Reduction

- Tourism, Arts, Culture and Sport

- Transportation and Infrastructure

- Water, Land and Resource Stewardship

Secondary suite program launches, creating thousands of more affordable homes for people

B.C. moves to ban drug use in public spaces, taking more steps to keep people safe

More from the premier.

- Factsheets & Opinion Editorials

- Search News

- Premier's Bio

Province strengthens drought preparedness

B.C. vineyards, orchards receive help to replant for changing climate

More from this ministry.

- Minister's Bio

Joint statement on Asian Heritage Month

Premier’s, minister’s, parliamentary secretary’s statements on Jewish Heritage Month

Expanded eligibility, new supports available for current, former youth in care.

New position expedites progress on Indigenous child welfare

Governments of canada and british columbia working together to bring high-speed internet to more than 7,500 households.

Michael McEvoy to serve as interim information and privacy commissioner

B.c. takes action to improve literacy for students.

More spaces coming for elementary students in Burnaby

Stronger local-disaster response will keep people safer.

More than $26 million invested in disaster mitigation infrastructure improvements across British Columbia

Bc hydro issues call for new clean electricity to power b.c.’s future.

New legislation ensures B.C. benefits from clean, affordable electricity

Working together to preserve the natural beauty of pipi7íyekw/joffre lakes park.

More climate-action funding coming to communities throughout B.C.

Budget 2024: taking action for people, families in b.c..

Climate action tax credit helps people with everyday costs

B.c. plants its 10-billionth tree.

B.C. continues investments to support forest sector

Urgent and primary care centre opens in Chilliwack

Indigenous people in sooke get access to 170 below-market homes, historic b.c. legislation introduced recognizing haida aboriginal title.

Throne speech lays out vision of a stronger B.C. that works better for people

Province honours people providing extraordinary community service

New agritech plant anchors b.c.’s industrial blueprint.

Funding will strengthen rural Kootenay economies

2024 minimum wage increases confirmed, minister’s and parliamentary secretary’s statement on construction and skilled trades month, expanded mental-health, addictions support coming for south asian community, expanding multi-language support, services for newcomers, construction underway on cowichan sportsplex field house, new legislation recognizes work of first nations post-secondary institutes.

TradeUpBC builds, enhances tradespeoples’ skills

Province reaches major milestone in surrey police transition plan, budget 2024 supports improvements to treatment, recovery services.

Changes aim to help people out of poverty

Province provides updates for fifa world cup 26.

Province moves ahead on a safer amateur sport system

Province, yvr work together to support good jobs, fight pollution.

Airport improvements support services, growth for communities

Province supports new weir to keep cowichan river flowing.

Province strengthens flood defences, protecting people, communities

Province provides new tool for communities hosting major tourism events.

Honourable Katrine Conroy

Minister of Finance and Minister responsible for Columbia Basin Trust, Columbia Power Corporation, and the Columbia River Treaty

Email: [email protected]

Translations

News release, media contacts, ministry of finance.

- Visit Ministry Website

Featured Topics

- Public Accounts

- Economic Indicators

- Public Sector Bargaining

- Crown Agencies & Board Resourcing Office

Featured Services

- Provincial Sales Tax Exemptions

- Home Owner Grant

- Pay or Defer Your Property Tax

- Apply for Personal or Corporate Tax Credits

- Natural Resource Taxes

- Billing & Payment Services

Communities hosting major international tourism events need additional revenue to plan, stage and host those events, and reap the long-term economic benefits.

A new Major Events Municipal and Regional District Tax (MRDT) of up to 2.5% on short-term accommodation sales would help communities cover the cost of hosting major international tourism events that help bolster provincial tourism and the economy.

The Major Events MRDT is a time-limited, dedicated funding tool that communities can apply for through Destination BC. Communities will need support and prior approval from the minister responsible for tourism and the minister of finance to help ensure the tax is dedicated and applied as intended, and that it is time-limited and subject to public reporting and transparency.

“This isn’t a new concept,” said Selina Robinson, Minister of Finance. “In 2007, a temporary 4% Resort Area Tax, on top of the existing 2% accommodation tax, was introduced in the Resort Municipality of Whistler to help pay its costs for hosting the 2010 Winter Olympics. We see the potential benefits for other communities that are working to put B.C. on the international stage and bolster our economy.”

The City of Vancouver has asked the Province to temporarily raise the MRDT charged on purchases of accommodation within the city to help pay for the cost of planning, staging and hosting FIFA 2026 matches.

“We are thrilled that Vancouver was selected as one of the host cities for the FIFA World Cup 2026, the largest single sporting event in the world,” said Lisa Beare, Minister of Tourism, Arts, Culture and Sport. “This tool will support our partnership with the city to ensure the event is a success.”

A key goal of the legislation is to help Vancouver address its FIFA 2026 costs while providing a way for other communities to access the same tool to help cover the cost of hosting major international tourism events. The Province is working with Vancouver on how the new Major Events MRDT could be applied within the city.

Quick Facts:

- The additional major events accommodation tax is separate from the current MRDT that applies to short-term accommodations in more than 60 areas throughout the province.

- To apply, communities must have an agreement in place with the minister responsible for tourism to ensure the tax is used as intended, is time-limited and subject to public transparency. The minister of finance must also designate the event as a major international tourism event of provincial significance.

- The FIFA World Cup 2026 will be jointly hosted by Canada, the United States and Mexico. This World Cup will be the largest series of events ever held, and the first to feature 48 teams playing in 80 matches.

- It is expected that the United States will host 60 matches, with Canada and Mexico expected to host 10 matches each.

- Major_events_tax_French.pdf

Related Articles

More supports coming for women, children facing domestic violence, exploitation.

Connect with the Ministry

View the Ministry's latest photos on Flickr.

Watch the Ministry's latest videos on YouTube.

Acknowledgment

The B.C. Public Service acknowledges the territories of First Nations around B.C. and is grateful to carry out our work on these lands. We acknowledge the rights, interests, priorities, and concerns of all Indigenous Peoples - First Nations, Métis, and Inuit - respecting and acknowledging their distinct cultures, histories, rights, laws, and governments.

Connect with Us:

- Newsletters

- Accessibility

B.C. introduces new hotel tax to support major tourist events

The tax, up to 2.5 per cent on short-term accommodations, comes from a City of Vancouver request for support in hosting games during the 2026 World Cup

You can save this article by registering for free here . Or sign-in if you have an account.

Article content

British Columbia is introducing a new tax on hotels and other short-term accommodations that communities can tap to offset the cost of hosting major tourism events.

B.C. introduces new hotel tax to support major tourist events Back to video

The idea for the surtax, called the major events municipal and regional district tax, grew out of a request by the City of Vancouver to help with the cost of hosting games during the 2026 World Cup.

Subscribe now to read the latest news in your city and across Canada.

- Unlimited online access to articles from across Canada with one account.

- Get exclusive access to the Vancouver Sun ePaper, an electronic replica of the print edition that you can share, download and comment on.

- Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

- Support local journalists and the next generation of journalists.

- Daily puzzles including the New York Times Crossword.

Create an account or sign in to continue with your reading experience.

- Access articles from across Canada with one account.

- Share your thoughts and join the conversation in the comments.

- Enjoy additional articles per month.

- Get email updates from your favourite authors.

Sign In or Create an Account

A community can tap into the tax, up to a maximum of 2.5 per cent, to plan, stage and host a major event that provides a boost to the provincial tourism economy.

The B.C. government describes it as “a time-limited, dedicated funding tool that communities can apply for through Destination B.C. ”

Communities must get approval from the tourism and finance ministers before applying the tax, which is only allowed for a defined time and must be publicly reported.

“This isn’t a new concept,” said B.C. Minister of Finance Selina Robinson, noting that Whistler had a temporary four-per-cent resort area tax on top of its existing accommodation tax to help with the costs of hosting the 2010 Winter Olympics.

“We are thrilled that Vancouver was selected as one of the host cities for the FIFA World Cup 2026, the largest single sporting event in the world,” said Tourism Minister Lisa Beare. “This tool will support our partnership with the city to ensure the event is a success.”

Though introduced before incoming Vancouver mayor Ken Sim takes office, Sim indicated Monday he is on side.

“The provincial government and mayor-elect Sim are aligned on this new mechanism to support major events like the 2026 World Cup,” said a statement. “The province has articulated that the incoming (tax) will be up to 2.5 per cent. We recognize that our tourism sector will be rate sensitive to such a measure.”

B.C. Liberal finance critic Peter Milobar warned that communities need to tread lightly hitting up the highly taxed sector for more money.

“I think you always have to be careful … around that level of taxation when you start to layer on things,” said Milobar. He said there are still many questions such as how long the tax can be applied, and what type of event will qualify.

“I think there’s a certain irony that on a day in question period where we were asking questions about the Olympic bid, that they were bringing forward a way to generate revenues that could have offset a lot of those costs of the 2030 Olympics if this was already in the works legislatively.

“So it does make you question what cabinet is talking about when they go in and say the Olympics is going to be too much risk,” when this tax could have been put in place to offset that risk, said Milobar.

While it was introduced with the 2026 World Cup in mind, any B.C. community hosting a major event can apply.

— With a file from Katie DeRosa

More news, fewer ads: Our in-depth journalism is possible thanks to the support of our subscribers. For just $3.50 per week, you can get unlimited, ad-lite access to The Vancouver Sun, The Province, National Post and 13 other Canadian news sites. Support us by subscribing today: The Vancouver Sun | The Province .

Postmedia is committed to maintaining a lively but civil forum for discussion. Please keep comments relevant and respectful. Comments may take up to an hour to appear on the site. You will receive an email if there is a reply to your comment, an update to a thread you follow or if a user you follow comments. Visit our Community Guidelines for more information.

BMO Vancouver Marathon 2024: Which roads will be closed on race day? (with map)

Motorcyclist hit head-on will never work again, b.c. court awards $1.8 million.

London Drugs announces gradual reopening of stores following cybersecurity incident

B.c. parents of gifted children decry pause in accelerated learning program.

Former B.C. MP has 'lost faith' after inquiry finds foreign interference may have cost him his seat

This website uses cookies to personalize your content (including ads), and allows us to analyze our traffic. Read more about cookies here . By continuing to use our site, you agree to our Terms of Service and Privacy Policy .

You've reached the 20 article limit.

You can manage saved articles in your account.

and save up to 100 articles!

Looks like you've reached your saved article limit!

You can manage your saved articles in your account and clicking the X located at the bottom right of the article.

Municipal and Regional District Tax

MRDT – also known as Hotel Tax – applies to short-term tourist accommodation, including hotel rooms. This 3% hotel tax is in addition to the eight per cent Provincial Sales Tax (PST).

The MRDT tax program was originally established by the Province in 1987 to support the financing and operations of incremental tourist related facilities as well as ongoing funding of tourism marketing and associated programs.

In Whistler, MRDT revenues are received by the RMOW and shared equally with Tourism Whistler based on a number of agreements. Revenues are reinvested by both organizations on behalf of the community. Expenditures are approved by, and reported back to, the Province to ensure ongoing alignment with the prescribed purposes of the tax as outlined in the Provincial Sales Tax Act.

In 2021, the RMOW’s share was budgeted for $2.6 million. These funds are leveraged to enhance the tourism experience and encourage travel in shoulder seasons and mid-week.

MRDT (along with the Resort Municipality Initiative ) has been critical for Whistler to supplement property tax revenues and ensure a revenue stream directly from, and reinvested back into, the tourism economy.

Increase to three per cent

The Province of B.C. increased the amount of MRDT that Whistler receives from two to three per cent on November 2018.

Changes to online accommodation

Airbnb and other online accommodation providers are legally required to submit PST and MRDT on short-term accommodation of less than 27 days.

The Province started collecting MRDT on tourist rentals listed on online accommodation providers on October 1, 2018. Compliance is legal requirement, and fines are in place for non-compliance, late filings or remittances.

Incremental funds collected through online accommodation providers are also eligible to be invested in affordable housing. The Province requires interested communities to submit an additional annual proposal to the Province. The RMOW has invested 100 per cent of its share of online accommodation provider revenues into the Cheakamus Crossing Phase II (Lot 1) affordable housing project since 2019.

I want to...

- Activities and classes

- Permits or licences

- Home Owner Grants

- MyWhistler account

- Parking pass

- E-newsletter subscription

- Council meetings and minutes

- Recreation facilities, parks and trails

- Career opportunities

- Bus schedules and information

- Parking information

- Permits and licences

- Bylaws and regulations

- Waste disposal information

- News Releases

- Bid opportunities

- Community monitoring indicators

- Parking (day rates and passes)

- Parking ticket

- Violation tickets

- Dog licence

- Business licence

- Property tax

- Recreation activity registration

- Parking passes

- Parking ticket payment

- Property taxes

- Report a concern

- All Online Services

- Meadow Park Sports Centre

- Notices and closures

- Rates: admission and passes

- Recreation activity schedules

- Login to MyRecreation

- Registration information

- Fitness Classes

- Nordic skiing/snowshoeing

- View all services

Section Quick Links

Our community vision.

Whistler: A place where our community thrives, nature is protected and guests are inspired. Learn More

Development

Sign up for the RMOW mailing List

Get the latest community news, upcoming events and programs and important updates from Council conveniently delivered straight to your inbox. Opt in or out anytime.

- Municipal Hall

- 4325 Blackcomb Way,

- Whistler, B.C. V8E 0X5

- Tel: 604-932-5535

- Fax: 604-935-8109

- Toll-Free: 1-866-932-5535

- [email protected]

- About the Resort Municipality of Whistler

- Accessibility

- Facts and Figures

- Privacy Policy

- Stay informed

- Newsletter subscription

- Submit website feedback

- Media contact

- Submit media inquiry

- Latest news

- Mayor and Council

- Departments

Whistler: A place where our community thrives, nature is protected and guests are inspired. More Info

- EN FRANÇAIS

B.C. approves 2.5% Vancouver accommodation tax to help city pay to host FIFA World Cup

Major events tax will be in effect in vancouver for 7 years to help city offset cost of hosting the games.

Social Sharing

Starting Feb. 1, booking a room in a Vancouver hotel, Airbnb or vacation rental by owner (VRBO) will come with an additional 2.5 per cent tax as the city seeks to raise revenue to host the 2026 FIFA World Cup.

To help offset hosting costs, the B.C. government and Destination Vancouver have agreed to the temporary tax rate on sales of short-term accommodation for the next seven years.

Revenues from the temporary tax hike — known as the Major Events Municipal Regional District Tax — will be used to finance planning, staging and hosting the soccer tournament.

The City of Vancouver asked the provincial government for the tax hike last fall, saying the city would have to run at "above and beyond normal operating city service levels" for the World Cup.

Revenues from the major events tax will go toward offsetting the costs of staff, security, venues, resourcing and training sites.

Vancouver and Toronto are among 16 North American host cities and will hold 10 of the event's 70 matches.

- Vancouver seeks 2.5% tax on short-term accommodation to raise revenue for hosting FIFA World Cup games

- B.C. extends bar hours for 2022 World Cup

The B.C. government previously imposed a major events tax to fund the Vancouver Olympics in 2010.

Communities can also seek the approval of the ministers of tourism and finance for such a tax through Destination B.C.

It can be applied on top of an existing accommodation tax already in place in more than 60 regions in the province that finance tourism marketing, programs and projects.

"I think it's fairly reasonable," said Vancouver Coun. Pete Fry. "It's a modest fee attached to hotel and short-term rental stays that'll help offset some of the cost demands we will have with an event like FIFA."

Fry tells CBC that raising revenue through tourism will spare Vancouver residents the significant costs of hosting such a high-level event.

Hotel and tourism sector on board, says minister

B.C.'s finance minister, Katrine Conroy, says the rate was determined in consultation with Vancouver's hotel and tourism sector.

"They all agreed after much discussion that there will be hundreds of thousands of people coming into the city, so it will bolster tourism and help them."

The B.C. Hotel Association was not available for comment.

Peter Milobar, the B.C. Liberal MLA for Kamloops-North Thompson and opposition finance critic with a background in the hotel industry says he can imagine the sector agreeing to the rate but says he has concerns about the timeline.

"They want to make sure that it's not just an unlimited pot of money that keeps getting added to in terms of cost, cost pressures, or length of time with taxes in place."

Conroy says representatives from the hotel sector initially had concerns with the time frame. The province estimates the tax will generate approximately $230 million.

- So the 2026 World Cup is coming to Vancouver. Here's what we know

- New Canadian pro women's soccer league to fill missing link in player development

"There was an agreement that this would be applied over seven years, and there's also an agreement that if that amount of money is incurred prior to the seven years, the tax will end."

"Inflation has gone up, so we feel estimates might be a little higher, but we'll see," said Conroy. "We know the costs could increase with more detailed planning."

ABOUT THE AUTHOR

Ali Pitargue is an associate producer at CBC Vancouver. You can contact her at [email protected].

Related Stories

- Top stories from British Columbia

- Kelowna man photographs rare encounter with pack of wolves

- Hospital psychiatrist gives contradicting evidence at inquest into death of VPD Const. Nicole Chan

- 2 Vancouver Island area ERs to close overnight for foreseeable future

- Skip to main content

- Skip to main navigation

- Accessibility Statement

Tourism resources

Information to help start or grow your existing tourism business. Review the latest tourism research, learn about funding and connect with industry partners.

Services and information topics

Tourism funding programs.

There are a number of different funding sources available to support B.C.'s tourism sector.

Destination Development

Destination development is guided by the Strategic Framework for Tourism in British Columbia and aims to help communities grow and manage their destinations. Destination development is focused on enhancing the supply side of tourism, by providing compelling experiences, quality infrastructure, and remarkable services to entice repeat visitation.

British Columbia’s Tourism Ecosystem

As the provincial leader in tourism, the role and responsibilities of the Ministry are to set the strategic direction for provincial tourism priorities. This work is done through collaboration within government, with municipalities, tourism organizations and businesses that creates the fabric of tourism in the Province of B.C.

Strategic Framework for Tourism in B.C.

Tourism has — and will always be — integral to who we are as British Columbians. A thriving tourism industry contributes to an inclusive economy and provides a pathway for jobs, opportunity, and entrepreneurship in our province.

Tourism Research

This page includes summary statistics that describe the importance of the tourism sector in British Columbia. It also includes sources for tourism data and statistics.

Conversations on the Future of Tourism in British Columbia

Tourism Marketing

Tourism marketing and promotion in B.C. is led by Destination British Columbia (Destination BC).

Tourism Recovery Collaboration

The Government of B.C. collaborates with the tourism industry to guide its work in accelerating recovery and growth of the tourism sector in British Columbia.

These voices are represented in two forums - the Tourism Sector Recovery Roundtable and the past work of the Tourism Task Force.

Training & Finding Jobs in B.C.'s Tourism Sector

Tourism in B.C. supported over 46,400 jobs in 2020. This includes $2.4 billion in GDP (in 2012 constant dollars) contributed to B.C.'s economy and $1.8 billion in tourism wages & salaries.

There are many different jobs available in the tourism sector. Use these resources to find tourism jobs and access job-related advice.

The B.C. Public Service acknowledges the territories of First Nations around B.C. and is grateful to carry out our work on these lands. We acknowledge the rights, interests, priorities, and concerns of all Indigenous Peoples - First Nations, Métis, and Inuit - respecting and acknowledging their distinct cultures, histories, rights, laws, and governments.

News + Updates

- No Comments

GENERAL INFORMATION: As announced in British Columbia’s Budget 2022 on February 22, 2022, effective July 1, 2022, certain marketplace facilitators must charge and collect provincial sales tax (PST) and the municipal and regional district tax (MRDT) on taxable sales and leases that they facilitate through an online marketplace. This includes taxable sales of accommodation facilitated through an online marketplace by an online marketplace facilitator.

A marketplace facilitator is a person who:

- operates, owns or controls (solely or jointly) an online marketplace,

- through the online marketplace, facilitates a marketplace seller’s retail sales of goods, software or taxable services, and

- collects payment in respect of the retail sales of goods, software or taxable services.

Marketplace facilitators must register to collect and remit PST effective July 1, 2022, if they facilitate a marketplace seller’s retail sale of:

- goods that at the time of sale are located within Canada and are sold to a person in BC,

- software for use on or with an electronic device ordinarily situated in BC,

- accommodation in BC, or

- taxable services, other than accommodation, to a person in BC

However, marketplace facilitators are not required to register if:

- the gross value of retail sales of goods, software and taxable services that the marketplace facilitator made or facilitated in the preceding 12 months was $10,000 or less, or

- the reasonable estimate of the gross value of retail sales of goods, software and taxable services that the marketplace facilitator will make or facilitate in the next 12 months is $10,000 or less, or

- There are two or more marketplace facilitators who jointly operate, own or control an online marketplace and at least one of the other marketplace facilitators is registered for PST and will collect all PST payable for those taxable sales made through the online marketplace.

A marketplace seller is a person who, through an online marketplace, sells goods, software or taxable services (including accommodation). Additional information on the new rules is available in the Ministry of Finance’s Bulletin 142, Marketplace Facilitators, Marketplace Sellers, and Online Marketplace Services , available at: https://www2.gov.bc.ca/assets/gov/taxes/sales-taxes/publications/pst-142-marketplace-facilitators.pdf . In addition, Bulletin 120, Accommodation , has been updated with information on the new rules and is available at: https://www2.gov.bc.ca/assets/gov/taxes/sales-taxes/publications/pst-120-accommodation.pdf . SPECIFIC QUESTIONS: 1. Is the municipal and regional district tax (MRDT) and provincial sales tax (PST) exempt for all prepaid online travel agency (OTA) bookings?

These prepaid bookings are still subject to PST and MRDT (where applicable) as sales of accommodation in BC, unless a specific exemption applies. However, effective July 1, 2022, online marketplace facilitators are required to collect and remit the PST and MRDT where they facilitate retail sales of accommodation in BC made by an online marketplace seller through an online marketplace. Online marketplace facilitators are also generally required to register to collect and remit PST where they facilitate retail sales of accommodation in BC.

When it comes to online travel agency bookings, the online travel agency is considered an online marketplace facilitator and the accommodation provider is considered an online marketplace seller. Therefore, for prepaid bookings made through the online travel agency website, the online travel agency is required to collect and remit the applicable PST and MRDT on the facilitated accommodation sale. The accommodation provider does not collect and remit the PST and MRDT on these sales. Nevertheless, the accommodation provider remains jointly and severally liable for any PST and/or MRDT not collected and remitted by the marketplace facilitator.

Also, accommodation providers themselves are still required to collect and remit PST and MRDT on sales of accommodation in BC where they do not sell the accommodation through an online marketplace facilitator (e.g. the accommodation provider sells it over the phone or through their own website).

2. This does not apply for Fit and Tour bookings, only online travel agencies?

Where “Fit” and “Tour” bookings refer to purchases of tourism services from a tourism agent where accommodation has been packaged into that tourism service.

If a marketplace facilitator is required to be registered, then they must collect and remit PST and MRDT, when applicable, on all taxable sales of accommodation that they facilitate through their online marketplace.

However, where accommodation is purchased by a tourism agent and is packaged into a tourism service that the tourism agent sells to their customer through an online marketplace, the tourism agent is not considered to be making a sale of accommodation. Therefore, if a marketplace facilitator facilitates the sale of tourism service (that includes accommodation) by a tourism agent through the facilitator’s online marketplace, the marketplace facilitator does not charge PST or MRDT on the sale. No taxable sale of accommodation has taken place.

If the “Fit” or “Tour” booking does not involve purchasing a packaged tourism service from a tourism agent, then the booking does involve the taxable sale of accommodation. If a marketplace facilitator facilitates the sale of accommodation through the facilitator’s online marketplace, the marketplace facilitator must charge PST and MRDT on that taxable sale of accommodation.

3. Do OTA bookings that pay at the hotel still pay all taxes (GST, PST, MRDT)?

The Ministry cannot provide advice on the taxes of other jurisdictions, or the application of the Goods and Services Tax (GST)/Harmonized Sales Tax (HST), as that is a federal tax on sales of goods and services. The Canada Revenue Agency (CRA) is responsible for administering the GST/HST. For questions concerning the application of the GST/HST, your members may visit the CRA’s dedicated GST/HST web pages at or call the CRA at 1-800-959-5525.

PST and MRDT apply to all sales of accommodation in BC (unless a specific exemption applies) regardless of how and when the purchase of accommodation is made.

Who is responsible for collecting and remitting the PST and MRDT on a taxable accommodation sale depends on who is collecting the payment for the accommodation. If an individual books accommodation through an online marketplace but pays the accommodation provider directly, then PST and MRDT must be levied by the accommodation provider. In this situation, the online marketplace is not acting as an online marketplace facilitator because they are not collecting payment in respect of the accommodation. The accommodation provider is directly collecting the payment.

If an individual books accommodation through an online marketplace and payment for the accommodation is collected by the online marketplace, then the online marketplace is acting as an online marketplace facilitator and is required to collect and remit the PST and MRDT on the accommodation sale.

4. They are not GST exempt, only provincial taxes?

As mentioned above, the Ministry cannot comment on the taxes of other jurisdictions, or the application of the Goods and Services Tax (GST)/Harmonized Sales Tax (HST), as that is a federal tax on sales of goods and services. The Canada Revenue Agency (CRA) is responsible for administering the GST/HST. For questions concerning the application of the GST/HST, your members may visit the CRA’s dedicated GST/HST web pages at or call the CRA at 1-800-959-5525. We assume that the reference to “only provincial taxes” refers to accommodation providers who sell their accommodation on an online marketplace are not required to levy and collect PST and MRDT on that accommodation because the online marketplace facilitator will. If so, then that is correct.

5. Is there anything that the hotels should be doing to change their collection and remittance of taxes? Accommodation providers do not collect and remit PST and MRDT on sales of accommodation that are sold through an online marketplace facilitator that is required to be registered for PST. If an accommodation provider is unsure of whether a marketplace facilitator will be collecting and remitting PST and MRDT on accommodation sales made through the facilitator’s online marketplace, they should contact the facilitator as soon as possible to verify that the facilitator will be collecting and remitting the PST and MRDT. If the marketplace facilitator does not levy PST and MRDT as required on accommodation sales made through the online marketplace, the accommodation provider cannot charge PST and MRDT directly to the guest. The guest is required to self-assess and pay any PST and MRDT directly to government. 6. How is my business protected if I stop charging PST on July 1 assuming it will be remitted by the marketplace facilitator (e.g. Expedia, Booking.com)? If the PST and MRDT is for some reason not paid on these bookings and I am audited in the following year, I have no recourse to collect PST from the guest. Is this correct?

While the marketplace facilitator is required to register, levy and collect PST and MRDT on accommodation sales that are facilitated through the online marketplace, the accommodation provider remains jointly and severally liable for any PST and MRDT not collected and remitted by the marketplace facilitator if the marketplace facilitator is later assessed for the outstanding PST and MRDT.

As noted in our answer to #5, if the marketplace facilitator does not levy PST and MRDT as required on accommodation sales made through the online marketplace, the accommodation provider cannot charge PST and MRDT directly to the guest. The guest is required to self-assess and pay any PST and MRDT directly to government.

7. I am assuming the tax consequence to be triggered by the payment, for example, an Expedia Prepaid booking attracts tax to be levied by Expedia. However, if someone uses Expedia, but just as a booking tool and then pays us directly when they get to the hotel, does that extinguish Expedia’s role as tax collector and put it back on the hotelier? Yes, as noted in answer to #3, this is correct. Who is responsible for collecting and remitting the PST and MRDT on a taxable accommodation sale depends on who is collecting the payment for the accommodation. If an individual books accommodation through an online marketplace (e.g. Expedia) but pays the accommodation provider directly, then PST and MRDT must be levied by the accommodation provider. In this situation, the online marketplace is not acting as an online marketplace facilitator because they are not collecting payment in respect of the accommodation. The accommodation provider is directly collecting the payment.

If an individual books accommodation through an online marketplace and payment for the accommodation is collected by the online marketplace (e.g. Expedia), then the online marketplace is acting as an online marketplace facilitator and is required to collect and remit the PST and MRDT on the accommodation sale. FURTHER INFORMATION For more information on British Columbia’s PST, including registration, and collecting and remitting the PST, can be found in a series of PST Bulletins and Notices , and the Small Business Guide to PST . Our Forms Page contains exemptions certificates and forms related to registration, applying for a refund, and self-assessing the PST. For additional information, including free interactive webinars, informational videos and upcoming events, you may be interested in visiting the Government’s PST Outreach webpage. To receive updates about legislative changes and new public information, click “Subscribe To Receive Updates.” To share any additional questions – reach out to [email protected] .

Leave a Reply Cancel reply

You must be logged in to post a comment.

- February 2024

- January 2024

- December 2023

- September 2023

- August 2023

- February 2023

- January 2023

- December 2022

- November 2022

- September 2022

- August 2022

- February 2022

- January 2022

- Advocacy Win

- BC Tourism Hospitality Conference

- Government Relations

- Hotel Cyber Awareness

- IT Partners

- Message From Ingrid Jarrett

- Rapid Tests

- Recruitment

- Restrictions

- Road Closures

- Safety Plan

- State of Emergency

- Tip Our Hat

- Uncategorized

Copyright © 2023 All Rights Reserved BC Hotel Association

Language selection

- Français fr

British Columbia tax information for 2023 - Personal income tax

Personal income tax

British Columbia tax information for 2023

Use the information on this page to help you complete your provincial tax and credits form.

On this page

New for 2023, british columbia benefits for individuals and families.

- Form BC428 – British Columbia Tax

- Form BC479 – British Columbia Credits

Download a copy of British Columbia tax information for 2023

Prior years.

The personal income levels used to calculate your British Columbia tax have changed.

The amounts for most provincial non-refundable tax credits have changed.

The clean buildings tax credit is effective February 23 , 2022. For more information, see British Columbia clean buildings tax credit .

The training tax credit has been extended until December 31 , 2024.

The shipbuilding and ship repair industry tax credit has been extended until December 31, 2024.

The farmer's food donation tax credit has been extended until December 31 , 2026.

A new refundable renter's tax credit is available for individuals. For more information, see British Columbia renter's tax credit .

To make sure you get your payments on time, you and your spouse or common-law partner need to file your 2023 Income Tax and Benefit Return (s) by April 30, 2024. The CRA will use the information from your return(s) to calculate the payments you are entitled to get from the following programs:

This benefit is a non-taxable amount paid to most families with children under the age of 18. This amount is combined with the Canada child benefit into a single monthly payment.

You do not need to apply for the BC Family benefit. The Canada Revenue Agency (CRA) will use the information from your Form RC66, Canada Child Benefits Application to determine if you are entitled to receive this credit.

This credit is a non-taxable amount paid to help individuals and families with the carbon taxes they pay. This amount is combined with the quarterly payment of the federal GST/HST credit.

You do not need to apply for the GST/HST credit or the BC climate action tax credit. The CRA will use the information from your return to determine if you are entitled to receive these credits.

The BC family benefit and the BC climate action tax credit are fully funded by the Province of British Columbia . For more information, call the CRA at 1-800-387-1193 .

Form BC428 – British Columbia Tax and Credits

Use this form to calculate your provincial taxes and credits to report on your return. Form BC428 must be completed after you have completed steps 1 to 5 of your federal income tax and benefit return.

Who should complete Form BC428

Complete Form BC428 if one of the following applies:

You were a resident of British Columbia at the end of the year

You were a non-resident of Canada in 2023 and any of the following applies:

- You earned income from employment only in British Columbia

- You received income from a business with a permanent establishment only in British Columbia

Completing Form BC428

Fill out part a – british columbia tax on taxable income.

Calculate your tax on taxable income using the chart in Part A

Fill out Part B – British Columbia non-refundable tax credits

The eligibility conditions and rules for claiming most British Columbia non-refundable tax credits are the same as those for federal non-refundable tax credits. However, the amount and calculation of most British Columbia non-refundable tax credits are different from the corresponding federal credits.

As a newcomer or an emigrant, you may be limited in the amount you can claim for certain provincial non-refundable tax credits.

If you reduced your claim for any of the following federal amounts, you also need to reduce your claim for the corresponding provincial amount in the same manner:

For examples on how to calculate these amounts, see Guide T4055 , Newcomers to Canada .

You can claim this amount if the rules are met for claiming the amount on line 30300 of your return and your spouse's or common-law partner's net income from line 23600 of their return (or the amount that it would be if they filed a return) is less than $11,285 .

You can claim this amount if the rules are met for claiming the amount on line 30400 of your return and your dependant's net income from line 23600 of their return (or the amount that it would be if they filed a return) is less than $11,285 .

You may be able to claim up to $5,243 for your spouse or common-law partner or an eligible relative who was dependent on you because of an impairment in physical or mental functions at any time in the year.

An eligible relative is one of the following:

- your (or your spouse's or common-law partner's) child or grandchild

- your (or your spouse's or common-law partner's) parent, grandparent, brother, sister, aunt, uncle, niece, or nephew who was a resident in Canada at any time in the year

Each dependant must meet all of the following conditions:

- They were 18 years of age or older

- Their net income for 2023 from line 23600 of their return (or the amount that it would be if they filed a return) was less than $22,985

- They were dependent on you because of an impairment in physical or mental functions

How to claim this amount

Complete the calculation for line 58175 using Worksheet BC428 . If you are claiming this amount for more than one dependant, enter the total amount on line 58175 of your Form BC428 .

You can claim the volunteer firefighters' amount (VFA) or the search and rescue volunteers' amount (SRVA) if the rules are met for claiming the amount on line 31220 or line 31240 of your return.

Enter on line 58315 the VFA you claimed on line 31220 of your return or enter on line 58316 the SRVA you claimed on line 31240 of your return.

Only residents of British Columbia are eligible for these amounts. If you were not a resident of British Columbia at the end of the year, you cannot claim either of these credits when calculating your British Columbia tax even if you may have received income from a source in British Columbia in 2023.

You can claim this amount if the rules are met for claiming the amount on line 31300 of your return.

You can claim up to $18,210 of eligible expenses for each child.

Enter on line 58330 the amount you claimed on line 31300 of your return.

Only residents of British Columbia are eligible for this amount. If you were not a resident of British Columbia at the end of the year , you cannot claim this tax credit when calculating your British Columbia tax even if you may have received income from a source in British Columbia in 2023.

The amount you can claim on line 58360 is the amount on line 31400 of your return or $1,000, whichever is less .

Only residents of British Columbia are eligible for this amount. If you were not a resident of British Columbia at the end of the year, you cannot claim this tax credit when calculating your British Columbia tax even if you may have received income from a source in British Columbia in 2023.

You can claim this amount if the rules are met for claiming the amount on line 31600 of your return.

If you were 18 years of age or older at the end of the year, enter $8,986 on line 58440 of your Form BC428 .

If you were under 18 years of age at the end of the year, use Worksheet BC428 to calculate the amount to enter on line 58440 .

You can claim this amount if the rules are met for claiming the amount on line 31800 of your return.

Complete Schedule BC(S11), British Columbia Tuition and Education Amounts .

If you claimed the Canada Training Credit (CTC) on line 45350 of your return, the amount you enter on line 59140 of your Schedule BC(S11) is already reduced by the CTC claimed.

Transferring amounts

If you do not use all of your 2023 tuition amount to reduce your provincial income tax to zero, you can transfer all or part of the unused amount to one of the following individuals that you designate:

- your spouse or common-law partner (who would claim it on line 59090 of their Schedule BC(S2) )

- your parent or grandparent (who would claim it on line 58600 of their Form BC428 )

- your spouse’s or common‑law partner’s parent or grandparent (who would claim it on line 58600 of their Form BC428 )

If your spouse or common-law partner is claiming an amount for you on line 58120 or line 58640 of their Form BC428 , you cannot transfer your unused tuition amount for the current year to your (or your spouse's or common-law partner's) parent or grandparent.

To designate who can claim the transferred amount and to specify the provincial amount they can claim, complete any of the following forms that you received as a student:

- Form T2202 , Tuition and Enrolment Certificate

- Form TL11A , Tuition and Enrolment Certificate – University Outside Canada

- Form TL11C , Tuition and Enrolment Certificate – Commuter to the United States

Complete the "Transfer or carryforward of unused amounts" section of Schedule BC(S11) to transfer an amount.

Carrying forward amounts

Complete the "Transfer or carryforward of unused amounts" section of Schedule BC(S11) to calculate the amount you can carry forward to a future year.

This amount is the part of your tuition and education amounts that you are not claiming for the current year and the part of your current-year tuition amount that you are not transferring to an individual that you designate.

Supporting documents

If you are filing a paper return, attach your completed Schedule BC(S11) . Keep your supporting documents in case you are asked to provide them later.

You may be able to claim the transfer of all or part of the unused 2023 tuition amount from your child or grandchild or their spouse or common-law partner.

The maximum amount each student can transfer to you is $5,000 minus the current year's amount that they claimed.

Enter, on line 58600, the total of all tuition amounts transferred to you from each student as shown on their forms T2202 , TL11A , or TL11C .

The student must enter this amount on line 59200 of their Schedule BC(S11) . They may choose to transfer an amount that is less than the available provincial amount.

The student cannot transfer to you any unused tuition and education amounts carried forward from previous years.

If you and the student were not residents of the same province or territory on December 31 , 2023, special rules may apply. For more information, call the CRA at 1-800-959-8281 .

The medical expenses you can claim on line 58689 are the same as those you can claim on line 33099 of your return. They also have to cover the same 12-month period ending in 2023 and must be expenses that were not claimed for 2022.

You can claim medical expenses for other dependants in addition to the medical expenses for self, spouse or common-law partner, and your dependent children born in 2006 or later on line 58689 .

The medical expenses you can claim on line 58729 are the same as those you can claim on line 33199 of your return. They also have to cover the same 12-month period ending in 2023 and must be expenses that were not claimed for 2022.

You can claim this credit if you meet all of the following conditions:

- You (or your spouse or common-law partner) carried on a farming business in British Columbia in the year the qualifying gift was made

- You made a qualifying gift to an eligible charity on or after January 1, 2018, and have not claimed it yet

- You claimed the qualifying gift on line 34000 of your federal Schedule 9, Donations and Gifts , and on line 58969 of your Form BC428 as a charitable donation or gift for the year

You can claim 25% of the eligible amount of the total qualifying gifts made to an eligible donee.

A qualifying gift is a gift of one or more agricultural products you produced in British Columbia and donated to an eligible charity in British Columbia on or after January 1, 2018 .

An agricultural product is any of the following:

- meat products

- eggs or dairy products

- maple syrup

- anything else that is grown, raised or harvested on a farm and can legally be sold, distributed, or offered for sale at a place other than the producer's premises as food or drink in British Columbia

An item of any of these types that has been processed is an agricultural product if it was processed only to the extent necessary to be legally sold off the producer’s premises as food or drink intended for human consumption. Items that have been processed beyond this point, such as pies, sausages, beef jerky, pickles, and preserves, are not agricultural products.

An eligible charity is a registered charity under the Income Tax Act that meets at least one of the following conditions:

- It distributes food to the public without charge in British Columbia and does so to provide relief to the poor (food banks meet this condition)

- It is engaged in providing meals or snacks to students in a qualifying school

The amount of qualifying donations can be split between you and your spouse or common-law partner. However, the total amount of qualifying donations that can be claimed by you and your spouse or common-law partner cannot be more than the total of the qualifying donations made in the tax year.

Any unused amounts can be carried forward for five years as long as you (or your spouse or common-law partner) earned farming income in British Columbia in the year the gift was made.

If you are preparing a return for a person who died in 2023 , you can claim this credit on their final return.

If you were bankrupt in 2023, claim your farmers' food donation tax credit on the pre- or post‑bankruptcy return you file for the tax year ending December 31 , 2023 , depending on when the qualifying donations were made.

If qualifying donations are claimed on more than one return, the total amount of donations that can be claimed on all returns filed for the year cannot be more than the total qualifying donations made.

How to claim this credit

Enter the amount of donations you have included on line 34000 of your federal Schedule 9 that are qualifying gifts for the farmers' food donation tax credit. Then enter 25% of this amount on line 58980 of your Form BC428.

Fill out Part C – British Columbia tax

Complete this part to calculate your British Columbia tax.

If you are reporting federal tax on split income on line 40424 of your return, complete Part 3 of your Form T1206, Tax on Split Income , to calculate the British Columbia tax to enter on line 42800 of your return.

If you need to pay federal minimum tax as calculated on Form T691, Alternative Minimum Tax , complete the calculation on line 69 of your Form BC428 to determine your British Columbia additional tax for minimum tax purposes.

If your federal foreign tax credit on non-business income is less than the related tax you paid to a foreign country, you may be able to claim a provincial foreign tax credit.

Complete Form T2036, Provincial or Territorial Foreign Tax Credit .

If you are filing a paper return, attach your Form T2036.

If your net income for the year is less than $37,814 , you may be able to reduce or eliminate your British Columbia tax by claiming a BC tax reduction.

If you are preparing a return for a person who died in 2023, you can claim the tax reduction on their final return.

You can claim this credit if you have to pay British Columbia logging tax for 2023 under the Logging Tax Act for logging operations in British Columbia .

Enter, on line 81 of your Form BC428 , the credit shown on Form FIN 542S , Logging Tax Return of Income , or Form FIN 542P , Logging Tax Return of Income for Processors .

You can claim this credit if, in 2023 , you (or your spouse or common-law partner) contributed to a political party or constituency association registered in British Columbia or to candidates seeking election to the British Columbia legislature.

Enter your total political contributions made in 2023 on line 60400 of your Form BC428. Then calculate and enter your credit on line 84 as follows:

- For contributions of more than $1,150 , enter $500 on line 84 of your Form BC428

- For contributions of $1,150 or less , complete the calculation for line 84 using Worksheet BC428

If you are filing a paper return, attach the official receipt (signed by an official agent of the political party or independent candidate) for each contribution.

You can claim this credit if you acquired shares from a registered British Columbia employee share ownership plan ( E SOP ) at any time in 2023 (that you did not claim on your 2022 return ) or in the first 60 days of 2024.

Your Certificate ESOP 20 confirms the amount of your investment and the credit you are entitled to. The date you bought your shares is shown in the "Investment date" box.

If you bought shares under an employee share ownership plan and you want to know if the plan is registered under the Employee Investment Act , ask your employer.

If you are filing a paper return, attach your Certificate(s) ESOP 20 .

You can claim this credit if you acquired shares from a registered British Columbia employee venture capital corporation ( EVCC ) at any time in 2023 (that you did not claim on your 2022 return) or in the first 60 days of 2024.

Your Certificate EVCC 30 confirms the amount of your shares and the credit you are entitled to. The date you bought your shares is shown in the "Investment date" box .

If you have questions about the employee venture capital corporation tax credit certificate, contact your stockbroker, investment advisor or the employee venture capital corporation that issued your shares.

If you are filing a paper return, attach your Certificate(s) EVCC 30 .

The maximum total ESOP and EVCC tax credits you can claim on your 2023 return is $2,000. The ESOP and EVCC tax credits that you do not claim in a year are not refundable, and you cannot carry them forward to a future year.

If you bought ESOP or EVCC shares in the first 60 days of 2024, you can claim the tax credit on your 2023 or 2024 return or you can divide the credit between the two returns.

On the certificate, enter the credit amount you are claiming on your 2023 return and the credit amount you will claim on your 2024 return.

If you are filing a paper return, attach a photocopy of the original 2023 and 2024 certificates showing the breakdown of your credit between your 2023 and 2024 returns .

You can claim this credit if you invested in flow-through shares and BC flow-through mining expenditures have been renounced to you.

Your BC qualifying expenses are shown in box 141 or box 151 , or both on Form T101, Statement of Resource Expenses , that you received from a mining exploration corporation or in box 197 and box 241 of Form T5013, Statement of Partnership Income , that you received as a member of a partnership.

Complete Form T1231, British Columbia Mining Flow-Through Share Tax Credit .

If you are filing a paper return, attach your Form T1231 and your T101 or T5013 .

Form BC479 – British Columbia Credits

You may be entitled to the credits listed in this section even if you do not have to pay tax. If the total of these credits is more than the taxes you have to pay, you may get a refund for the difference.

To claim these credits, attach a completed Form BC479 , British Columbia Credits , to your return.

You can claim this credit if, on December 31 , 2023, you were a resident of British Columbia and you met any of the following conditions:

- You were 19 years of age or older

- You had a spouse or common-law partner

- You were a parent of a child

If you had a spouse or common-law partner on December 31 , 2023, you and your spouse or common-law partner need to decide who will claim the sales tax credit for the both of you.

If you are claiming the additional credit for your spouse or common-law partner ( line 10 ), your spouse or common-law partner must have been a resident of British Columbia on December 31, 2023 .

You are not eligible for this credit if any of the following conditions apply:

- You had a spouse or common-law partner on December 31 , 2023, and your adjusted family net income was $25,500 or more

- You were single, separated, divorced, or widowed on December 31 , 2023, and your adjusted family net income was $18,750 or more

- You were confined to a prison or a similar institution at the end of the year and you have been confined for more than six months in total for the year that you are claiming the credit

Do not claim this credit on a return for a person who died in 2023.

Bankruptcies for 2023

The British Columbia sales tax credit cannot be claimed on your pre-bankruptcy return for 2023 and subsequent years.

You may be eligible for this credit if, at the end of 2023 , you met both of the following conditions:

- You were a resident of British Columbia

- You, or someone on your behalf, paid or incurred eligible expenses in 2023 for improvements to your principal residence or the land your principal residence is situated on

You must also meet one of the following conditions for 2023:

- You were a senior ( 65 years of age or older) or a family member living with a senior

- You were a person with a disability eligible for the federal disability tax credit or a family member living with a person with a disability eligible for the federal disability tax credit

If you are not claiming the disability amount because you are claiming fees that you paid for an attendant or care in a nursing home, you may still be eligible.

You can claim whichever is less :

- the amount of eligible expenses that you, or someone on your behalf, paid or incurred relating to your principal residence

You must reduce your eligible expenses by the amount of any government assistance you received, or expect to receive, that is related to the eligible expenses.

If you occupied more than one principal residence at different times in 2023, eligible expenses that you paid or incurred for one or more of those residences would qualify for the credit.

The combined amount that you or your spouse or common-law partner can claim cannot be more than $10,000 . However, if, on December 31, 2023, you and your spouse or common-law partner occupied separate principal residences for medical reasons or because of a breakdown in your marriage or common-law relationship for a period of 90 days or more, each spouse or common-law partner can claim up to $10,000 of eligible expenses.

If you occupied separate principal residences for medical reasons , tick the box on line 60890 of your Form BC479 .

If you shared a principal residence with one or more family members , one of you may claim the entire amount of eligible expenses, or each member may claim a part of the eligible expenses. The combined amount that can be claimed by all family members is either $10,000 or the amount of eligible expenses paid, whichever is less .

If someone who does not live with you or is not related to you paid for the qualifying home renovation to your principal residence, you can still claim the credit. You will need to get the supporting documents and keep them in case you are asked to provide them later.

If an eligible expense also qualifies as a medical expense, you can claim both the medical expense tax credit and the British Columbia home renovation tax credit for seniors and persons with disabilities for that expense.

Definitions

A family member includes a parent, step-parent, grandparent, in-law , sibling, spouse, common-law partner, aunt, uncle, great-aunt , great-uncle , child, step-child , grandchild, niece, or nephew.

If you are a senior or a person with a disability, a principal residence is a residence in British Columbia that you occupy or expect to occupy by the end of 2025.

If you are not a senior or a person with a disability, a principal residence is a residence in British Columbia that you occupy or expect to occupy by the end of 2025 with a family member who is a senior or a person with a disability.

Eligible expenses are expenditures for improvements to the principal residence (or to the land the principal residence is on) that do one of the following:

- allow a senior or a person with a disability to gain access to, or to be more mobile or functional within, the home or on the land

- reduce the risk of harm to a senior or a person with a disability within the home or on the land or in gaining access to the home or the land

The improvements must be of an enduring nature and be integral to the home or the land.

Eligible expenses

Some examples of eligible expenses include:

- certain renovations to permit a first-floor occupancy or secondary suite for a senior or a person with a disability

- grab bars and related reinforcements around the toilet, bathtub, and shower

- handrails in corridors

- wheelchair ramps, stair and wheelchair lifts, and elevators

- walk-in bathtubs

- wheel-in showers

- widening of passage doors

- lowering of existing counters and cupboards

- installation of adjustable counters and cupboards

- light switches and electrical outlets placed in accessible locations

- door locks that are easy to operate

- lever handles on doors and taps, instead of knobs

- pull-out shelves under the counter to enable work from a seated position

- non-slip flooring in the bathroom

- a hand-held shower on an adjustable rod or high-low mounting brackets

- additional light fixtures throughout the home and at exterior entrances

- swing-clear hinges on doors to widen doorways

- creation of knee space under the basin to enable use from a seated position (and insulation of any hot-water pipes)

- relocation of tap to front or side for easier access

- hands-free taps

- motion-activated lighting

- touch-and-release drawers and cupboards

Expenses that are not eligible

Expenses are not eligible if their main purpose is to increase the value of the home or if they are for annual, recurring, or routine repair, maintenance or service.

Examples of ineligible expenses include:

- general maintenance like plumbing or electrical repairs

- roof repair

- aesthetic enhancements like landscaping or redecorating

- installation of new windows or regular flooring

- installation of heating or air conditioning systems

- replacement of insulation

Devices are not eligible. These include:

- equipment for home medical monitoring

- home-security (anti-burglary) equipment

- wheelchairs

- vehicles adapted for people with mobility limitations

- side-swing ovens and appliances with front-located controls

- fire extinguishers, smoke alarms, and carbon monoxide detectors

Services are not eligible. These include:

- security or medical monitoring services

- home care services

- housekeeping services

- outdoor maintenance and gardening services

Filing for a deceased person

- a senior (or would have turned 65 years of age by December 31 , 2023) and otherwise eligible

- a person with a disability

- a family member of a senior (or of a person who would have turned 65 years of age by December 31 , 2023) and otherwise eligible

- a family member of a person with a disability and otherwise eligible

You can claim this credit on your return if you lived with (or expected by the end of 2025 to live with) a family member who, right before death, was a senior or who would have turned 65 years of age by December 31 , 2023 , or was a person with a disability, and you are otherwise eligible.

Bankruptcies in 2023

The British Columbia home renovation tax credit for seniors and persons with disabilities can be claimed on your pre- or post-bankruptcy return depending on when the eligible expenses were paid or became payable.

Complete Schedule BC(S12) , British Columbia Home Renovation Tax Credit for Seniors and Persons with Disabilities .

Enter, on line 60480 of your Form BC479 , the amount from line 5 of your Schedule BC(S12) . Enter 10% of this amount on line 14 of your Form BC479 .

If you are filing a paper return, attach your Schedule BC(S12) to your return. Keep all your receipts in case you are asked to provide them later.

You can claim this refundable tax credit if you acquired shares from a venture capital corporation (VCC) or an eligible business corporation (EBC) registered in British Columbia at any time in 2023 (that you did not claim on your 2022 return ) or in the first 60 days of 2024.

Your Certificate SBVC 10 shows the date you acquired your shares under "Investment date."

Enter, on line 17 of your Form BC479 , your unused venture capital tax credits for VCC or EBC shares acquired in 2022 or previous years. If you acquired venture capital tax credit certificates issued for shares purchased:

- before February 20 , 2019 , the maximum credit you can claim is $60,000

- on or after February 20, 2019 , the maximum credit you can claim is $120,000

Enter, on line 18 of your Form BC479 , the "tax credit amount" and on line 19 , the "certificate number" shown on your Certificate SBVC 10 for VCC or EBC shares acquired in 2023 that you did not elect to claim on your 2022 return .

If you acquired VCC or EBC shares in the first 60 days of 2024, you can elect to claim the tax credit on your 2023 return or 2024 return . If you are electing to claim the credit in 2023 , enter, on line 20 of your Form BC479 , the "tax credit amount" and on line 21 , the "certificate number" shown on your Certificate SBVC 10 for those shares.

For questions about the venture capital tax credit, contact the venture capital corporation or eligible business corporation that issued your shares, your stockbroker, or your investment advisor.

If you are filing a paper return, attach your Certificate(s) SBVC 10 .

You can claim this 20% refundable tax credit if you were a resident of British Columbia at the end of the year and you incurred qualified mining exploration expenses in British Columbia in 2023.

However, you can claim up to 30% for expenses incurred after February 20 , 2007, in prescribed areas affected by the mountain pine beetle.

The expenses must have been incurred for determining the existence, location, extent, or quality of a mineral resource in British Columbia . They also include costs incurred for environmental studies and community consultations.

Complete Form T88, British Columbia Mining Exploration Tax Credit (Individuals) .

If you are claiming a mining exploration tax credit allocated from a partnership, complete Form T1249, British Columbia Mining Exploration Tax Credit Partnership Schedule .

If you are filing a paper return, attach your Form T88 and, if applicable, your Form T1249 .

Training tax credit (individuals)

You can claim this refundable tax credit if you were a resident of British Columbia at the end of 2023 and you met certain requirements in an eligible program administered through SkilledTradesBC.

Complete Form T1014, British Columbia Training Tax Credit (Individuals) .

If you are filing a paper return, attach your Form T1014 .

Training tax credit (employers)

You can claim this refundable tax credit for salaries and wages paid if you met all of the following conditions:

- You were a resident of British Columbia at the end of 2023

- You carried on a business in British Columbia in 2023

- You employed a person who, in 2023, met certain requirements in an eligible program administered through the SkilledTradesBC

If your principal business was construction, repair or conversion of ships in British Columbia, read " Shipbuilding and ship repair industry tax credit (employers) ."

If you were a member of a partnership other than a specified member, such as a limited partner, you can claim your proportionate share of the partnership's training tax credit.

Complete Form T1014-1 , British Columbia Training Tax Credit (Employers) .

If you are filing a paper return, attach your Form T1014-1 .

Shipbuilding and ship repair industry tax credit (employers)

- Your principal business was the construction, repair or conversion of ships in British Columbia

- You employed a person who, in 2023 , met certain requirements in an eligible program administered through the SkilledTradesBC

Complete Form T1014-2 , British Columbia Shipbuilding and Ship Repair Industry Tax Credit (Employers) .

If you are filing a paper return, attach your Form T1014-2 .

You can claim this refundable tax credit if you paid or incurred expenditures for qualifying retrofits that improve the energy efficiency of eligible commercial buildings and residential buildings with 4 or more units in British Columbia .

You must be a resident of British Columbia or have income allocated to British Columbia at the end of the year that you are claiming the credit. The retrofit must be certified by the British Columbia Ministry of Finance before you may claim this credit.

Claim this credit on your income tax return for the year following the tax year that the retrofit is completed. You can claim the credit no later than 18 months after the end of the tax year that follows the tax year in which a retrofit was completed.

The retrofit must be both completed before April 1, 2026 , and an application for certification must be filed to the British Columbia Ministry of Finance before April 1, 2027 , in order to be certified.

Qualifying expenditures are expenditures that are directly attributable to a qualifying retrofit. You must make or incur the expenditures under the terms of an agreement entered into after February 22, 2022 and paid before April 1, 2025 .