- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

Is There Travel Insurance That Covers COVID Quarantine?

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

We get it — traveling these days can be an uncomfortable experience. In the ever-changing world of COVID-19 variants, border restrictions and PCR tests, learning how to stay protected is important.

Travel insurance can insure you against a variety of complications during travel, including trip delay, trip cancellation and medical issues. But not all policies are the same, and coverage can vary not only across providers, but across policies themselves.

Let’s take a look at travel insurance that covers COVID-19 quarantine, plus the best COVID-19 travel insurance.

What does travel insurance usually cover?

Travel insurance can provide peace of mind on vacation, especially when things go awry. There are varying types and levels of coverage for travel insurance, though these are common inclusions for travel insurance policies:

Trip cancellation insurance.

Trip interruption insurance.

Trip delay insurance.

24-hour hotline assistance.

Emergency medical insurance.

Primary/secondary medical insurance.

Lost or delayed baggage insurance.

Rental car insurance.

There's a lot of variety when it comes to travel insurance and the types of incidents it’ll cover. The cost of your premium will vary according to the plan you select.

Cancel for Any Reason insurance allows you to cancel your trip and recoup your costs, no matter why you’ve chosen to cancel.

Before buying travel insurance, check to see if any of your credit cards offer trip insurance . Some travel credit cards offer this insurance free of charge when you use your card to pay.

The Chase Sapphire Preferred® Card , for example, provides primary rental car insurance when you charge the car to your card.

The Platinum Card® from American Express , meanwhile, will cover trip cancellation, trip delay and lost luggage insurance. Terms apply.

There are no credit cards whose benefits include medical insurance. You’ll want to read the terms carefully to be sure that any travel insurance you purchase covers instances of COVID-19.

» Learn more: Will my travel insurance cover coronavirus?

Finding insurance that covers COVID quarantine

In the beginning of the pandemic, many insurance policies covered losses related to COVID-19, including trip cancellation and medical issues.

Since then, some providers have chosen to exclude coverage for coronavirus-related issues. So you’ll need to search specifically for an insurance policy that covers COVID-19.

Fortunately, there are still insurance providers that’ll provide coverage in the event you’re affected by COVID-19, including:

Trip cancellation.

Trip delay.

Medical care/hospitalization.

Quarantine.

Several countries — like Thailand — actually require that you purchase this insurance before traveling.

If you already have an insurance provider in mind, take a look at their coverage options — and any available add-ons — to see if COVID-19 quarantines are covered.

» Learn more: The best travel insurance companies

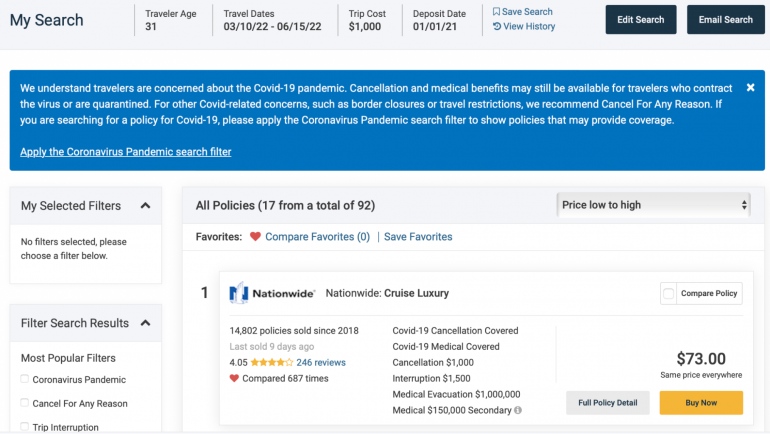

If you aren’t already committed to an insurance company, sites such as SquareMouth, a NerdWallet partner, will allow you to search for and compare policy coverage from multiple companies at once.

You’ll be asked to provide a variety of information, such as your destination, dates of travel, age, and whether you’d like to be reimbursed for cancellations.

SquareMouth’s search also includes the ability to filter search results so you’ll only see policies with COVID-19 protections.

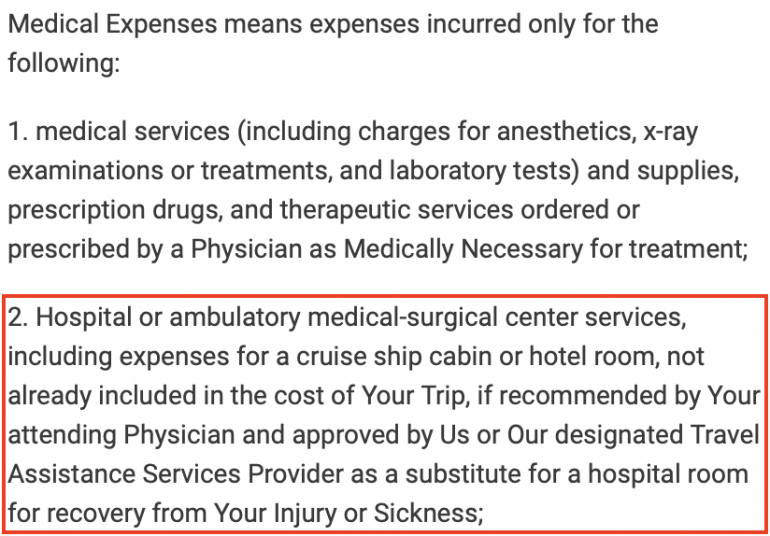

Once you’ve found a provider whose policy includes COVID-19 coverage, you’ll want to make certain that quarantine will also be reimbursed. Reading the policy in full will tell you; it can look something like this:

» Learn more: What to know before buying travel insurance

How much will COVID quarantine travel insurance cost?

The price of travel insurance is going to depend on many factors, including the length of your trip, your age, your destination and your coverage limits.

As you’d expect, the more comprehensive your coverage and the higher your limits, the more expensive your policy will be. The same is true if you’re heading out of the country for an extended period of time.

When comparing insurance policies, you’ll want to think about coverage limits as well as whether the insurance will provide primary or secondary coverage. Compare these factors against other policies to see which policy is the right fit for you.

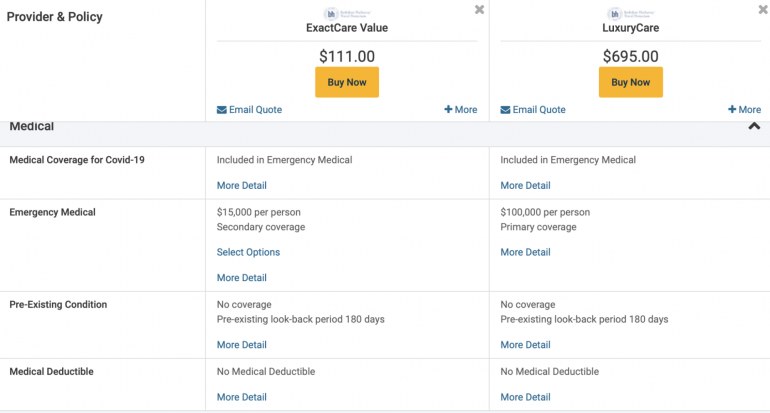

Here’s a comparison between two different policies. Although neither of these requires a deductible, one of these is secondary (it pays out after other insurance) and caps out at $15,000 per person in emergency medical expenses.

The other is primary (it pays out before other insurance policies) and covers up to $100,000 per person in emergency medical expenses:

While $15,000 may seem like a lot of money, remember that this total includes all doctor visits, tests and medications — in addition to the cost of your quarantine stay.

If you’re staying somewhere expensive, those costs can quickly add up.

Although some communities, such as New York City, may provide cost-free isolation accommodation, others will leave you to fend for yourself.

Even if staying in a moderately priced hotel, five to 10 days (or more) of isolation can quickly run into the thousands of dollars. You’ll want to be sure your insurance policy can cover this.

» Learn more: Does travel insurance cover COVID-19?

Final thoughts on travel insurance that covers COVID quarantine

Although the world is still trying to grapple with the COVID-19 pandemic, you may be looking to get out and travel again. Being protected in the event something happens can give you peace of mind when away from home.

This is especially true when it comes to mandatory COVID-19 quarantine, when costs can easily pile up. Acquiring travel insurance with COVID-19 quarantine protection can save you — and your wallet — in case of an emergency.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024 , including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-10x Earn 5x total points on flights and 10x total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3x points on other travel and dining & 1 point per $1 spent on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $900 toward travel when you redeem through Chase Travel℠.

1x-5x 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $750 when you redeem through Chase Travel℠.

1x-2x Earn 2X points on Southwest® purchases. Earn 2X points on local transit and commuting, including rideshare. Earn 2X points on internet, cable, and phone services, and select streaming. Earn 1X points on all other purchases.

50,000 Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening.

U.S. News takes an unbiased approach to our recommendations. When you use our links to buy products, we may earn a commission but that in no way affects our editorial independence.

The 5 Best COVID-19 Travel Insurance Options

Travelex Insurance Services »

Allianz Travel Insurance »

World Nomads Travel Insurance »

Generali Global Assistance »

IMG Travel Insurance »

Why Trust Us

U.S. News evaluates ratings, data and scores of more than 50 travel insurance companies from comparison websites like TravelInsurance.com, Squaremouth and InsureMyTrip, plus renowned credit rating agency AM Best, in addition to reviews and recommendations from top travel industry sources and consumers to determine the Best COVID Travel Insurance Options.

Table of Contents

- Rating Details

- Travelex Insurance Services

- Allianz Travel Insurance

Even though COVID-19 is no longer considered a global emergency, concerns around illness-related costs remain for many travelers. If you're looking for travel insurance that covers COVID – as well as other potential disruptions like flight delays and lost luggage – these are your best options.

- Travelex Insurance Services: Best Optional Coverage Add-ons

- Allianz Travel Insurance: Best for Multitrip and Annual Plans

- World Nomads Travel Insurance: Best for Active Travelers

- Generali Global Assistance: Best for Comprehensive Travel Insurance

- IMG Travel Insurance: Best for Travel Medical Insurance

Best COVID Travel Insurance Options in Detail

Plans include coverage for COVID-19

Optional CFAR coverage is available with Travel Select plan

Some coverages require an upgrade, including rental car collision, accidental death and dismemberment, and more

Not all add-ons are available with every plan

Allianz offers some travel insurance plans that come with an epidemic coverage endorsement

Single-trip, multitrip and annual plans available

COVID-19 benefits don't apply to every plan

Low coverage limits with some plans (e.g., only $10,000 in emergency medical coverage with OneTrip Basic plan)

24-hour travel assistance services included

More than 200 sports and activities covered in every plan

Low trip cancellation benefits ($2,500 maximum) with Standard plan

No CFAR option is offered

Free 10-day trial period

Some coverage limits may be insufficient

Rental car damage coverage only included in top-tier Premium plan

Offers travel medical insurance, international travel health insurance and general travel insurance plans

Some plans include robust coverage for testing and quarantine due to COVID-19

Not all plans from IMG offer coverage for COVID-19

Cancel for any reason coverage not available with every plan

Frequently Asked Questions

When comparing COVID-19 travel insurance options, you'll want to make sure you fully understand the coverages included in each plan. For example, you should know the policy inclusions and limits for COVID-related claims, including coverage for testing, treatments, trip cancellation or COVID-related interruptions that can occur. Meanwhile, you should understand how your coverage will work if you contract some other illness while away from home.

Also ensure your travel insurance coverage will kick in for other mishaps that occur, and that limits are sufficient for your needs. If you're planning a trip to a remote area in a country like Costa Rica or Peru , you'll want to have emergency evacuation and transportation coverage with generous limits that can pay for emergency transportation to a hospital if you need treatment.

You can also invest in a travel insurance policy that offers cancel for any reason coverage. This type of travel insurance plan lets you cancel and get a percentage of your prepaid travel expenses back for any reason, even if you just decide you're better off staying home.

It depends on your private health insurance provider and/or travel insurance policy. As of May 11, 2023, private health insurers are no longer required to cover the cost of COVID-19 testing. Out-of-pocket costs for COVID-19 test kits at local drugstores and on Amazon are relatively affordable, however.

As you search for plans that will provide sufficient coverage for your next trip, you'll find travel insurance that covers COVID-19 quarantine both inside and outside the United States. However, you'll typically need to have your condition certified by a physician in order for this coverage to apply. Also make sure your travel insurance plan includes coverage for travel claims related to COVID-19 in the first place.

Many travel insurance plans do cover trip cancellation as a result of COVID-19, although the terms vary widely. You typically need to be certified by a physician in order to prove your condition. Disinclination to travel because of COVID-19 – such as fear of exposure to illness – will generally not be covered. This means you will actually have to test positive for coronavirus for benefits to apply; simply not wanting to travel is not a sufficient reason to make a claim.

If you want more flexibility in your COVID-19 travel insurance, ensuring you have a cancel for any reason policy may be your best bet, but be sure to check with your chosen travel insurance provider to assess your options.

Why Trust U.S. News Travel

Holly Johnson is an award-winning writer who has been covering travel insurance and travel for more than a decade. She has researched the best travel insurance options for her own trips to more than 50 countries around the world and has experience navigating the claims and reimbursement process. Over the years, Johnson has successfully filed several travel insurance claims for trip delays and trip cancellations. Johnson also works alongside her travel agent partner, Greg, who has been licensed to sell travel insurance in 50 states.

You might also be interested in:

5 Best Travel Insurance Plans for Seniors (Medical & More)

Holly Johnson

Discover coverage options for peace of mind while traveling.

Does My Health Insurance Cover International Travel?

Private health insurance typically doesn't cover international travel expenses.

8 Cheapest Travel Insurance Companies Worth the Cost

U.S. News rates the cheapest travel insurance options, considering pricing data, expert recommendations and consumer reviews.

Is Travel Insurance Worth It? Yes, in These 3 Scenarios

These are the scenarios when travel insurance makes most sense.

How do you choose travel insurance that covers COVID-19?

Oct 26, 2021 • 5 min read

COVID-19 has made it more important to check the health coverage on your travel insurance © Maskot/Getty Images

After 18 months of pandemic-related travel restrictions, you may be itching to act on your pent-up wanderlust—but the situation and the rules are still continuously evolving. So before you go anywhere, it’s best to have a travel insurance plan that protects the investment you’ve made in a long-awaited trip.

A robust travel insurance plan will reimburse pre-paid trip costs and non-refundable deposits if you have to cancel or interrupt your trip, encounter trip delays, experience baggage loss or require medical expense and medical evacuation. Your policy will also reimburse “covered reasons” in your plan, such as death, illness or injury, serious family emergencies, unplanned jury duty, military deployment, acts of terrorism, or your travel supplier going out of business.

But COVID-19 has added an additional checklist to your usual insurance needs—it’s now important to check to ensure your travel insurance plan includes coverage for COVID-19 medical expenses, and losses related to illness. Your policy should also cover quarantine costs if you need to self-isolate after testing positive for the virus.

What do I look for in COVID-19 insurance coverage?

When you’re shopping for a travel insurance plan that covers COVID-19, you need to do your research and read the fine print of your plan.

Look for a travel insurance product that will protect your non-refundable, prepaid expenses if you have to cancel your trip due to illness caused by COVID-19. Your policy should also cover emergency medical treatment and emergency medical transportation. With regard to COVID-19 coverage, be sure your policy covers medical care, medicine, hospitalization and quarantine expenses.

“The type of coverage you should look for depends on you, your needs, travel dates, and the type of trip you’re taking,” says Sasha Gainullin, CEO of battleface , a travel insurance carrier. He says some travel insurance companies have now excluded COVID-19 coverage because it has been labeled a “known/foreseeable event”, while others may exclude pandemics altogether.

“It’s important to search for plans that include medical and quarantine expenses as well—this will be critical in the event you become ill and need to receive treatment while traveling,” continues Gainullin.

One additional tip is to confirm there are no exclusions based on the destinations you’re traveling to—this can happen with countries under government-issued travel warnings, Gainullin says.

“If a traveler feels uncertain, I recommend speaking with the travel insurance company directly. They can review the policy details with you, answer all of your questions, and confirm all of your required coverage options are included,” he adds.

Is getting coverage dependent on vaccination?

While it’s a good idea to be fully vaccinated before traveling, vaccination is not required to purchase a travel insurance policy, says Daniel Durazo, spokesperson with Allianz Partners USA.

What are the medical costs that are covered by travel insurance?

Travel insurance can cover the cost of both medical treatment and emergency medical transportation. A US health insurance plan, as well as Medicare, generally will not cover overseas medical expenses, so it’s best to check with your personal health insurance provider if any global coverage is available.

“While losing the cost of a trip due to an unexpected cancellation would be painful, paying for expensive emergency medical treatment or emergency medical transportation can be financially devastating,” Durazo says.

Under a travel insurance plan, medical costs could range doctor visits, pharmacy expenses, imaging costs and covering a hospital stay if required. Other expenses that can be covered are transportation to medical care and medicine.

Read more: Will my health insurance cover getting COVID-19 while traveling in the US—or abroad?

What about covering an unexpected quarantine due to COVID-19?

Many international destinations are now requiring that visitors purchase travel insurance coverage for an unexpected quarantine. Allianz Travel Insurance has added coverage to many of its products that includes reimbursement for quarantine-related accommodations if you or a traveling companion is individually-ordered to quarantine while on their trip, says Durazo.

This coverage typically covers the cost of additional food, lodging and transportation while quarantined. In addition, trip interruption and travel delay benefits on certain Allianz plans also provide coverage if you or your travel companion is denied boarding by your travel carrier due to suspicion of illness.

The benefits for quarantine coverage vary from carrier to carrier. For example, on select Trawick International plans, they offer $2,000 in quarantine benefits and for an additional charge, and you can increase it up to $7,000.

What about pre-flight COVID-19 testing?

Your plan may provide coverage for flights if you are turned away at a border for not passing a health inspection. Foster says Trawick’s travel insurance plans that cover COVID-19 would cover the expenses if you could not pass your pre-health inspection. Also, the plan would cover the costs of the failure of your PCR test to return to the United States, such as having to quarantine abroad.

It’s important to note that the actual cost of the PCR test is not covered by your policy, just the loss associated with the negative test.

Read more: PCR tests for travel: everything you need to know

Some destinations require COVID-specific insurance coverage—how do I comply with those restrictions?

Before any international travel, you should check the country where you are headed to make sure you comply with insurance coverage requirements. Countries like Spain, Turks and Caicos and Thailand are among the nations that mandate COVID-19 insurance coverage.

“You first must check the countries’ specific COVID regulations for entry into the country. Some countries require travelers to provide proof of travel insurance that covers COVID-19 related expenses purchased from a third party,” explains Foster. Providing proof coverage is key; so travelers need to ensure they receive documentation from their insurance provider that their policy covers COVID-19 related expenses to show customs officials, she says.

Should you arrive in a country that requires proof of insurance to cover COVID-19 medical expenses and quarantine costs, and you don’t hold a policy, you will not be granted entry.

For more information on COVID-19 and travel, check out Lonely Planet's Health Hub .

You may also like: What happens if I'm denied entry to a country on arrival? What is a vaccine passport and do I need one to travel? What is the IATA Travel Pass and do I need it to travel?

Explore related stories

Destination Practicalities

Mar 28, 2023 • 3 min read

Here’s all you need to know about getting a traveler visa to visit China now that “zero COVID” has come and gone.

Sep 12, 2022 • 4 min read

Apr 14, 2024 • 6 min read

Apr 14, 2024 • 7 min read

Apr 13, 2024 • 8 min read

Apr 13, 2024 • 9 min read

Apr 13, 2024 • 5 min read

Does travel insurance cover pandemics?

More than a quarter of the population of the U.S. has received at least one COVID-19 vaccination as of this week, and all those shots in arms seem to be directly correlating to a surge in travel.

In fact, the number of passengers in U.S. airports reached their highest numbers in more than a year last week according to the Transportation Security Administration ( TSA ). Whether you're vaccinated or not, concerns about new strains of the coronavirus are high, so it's not surprising to hear that inquiries about travel insurance have also hit their highest level since the pandemic began, according to InsureMyTrip .

However, "there is a big misconception about what travel insurance does — and doesn't — cover," said Meghan Walch, pandemic travel insurance expert for InsureMyTrip . In the company's latest poll of travel insurance agents, the vast majority of questions (a whopping 97%) from would-be travelers are regarding how travel insurance may or may not cover COVID-19 related travel concerns.

So, does your travel insurance cover a pandemic? Here's everything you need to know.

For more TPG news delivered each morning to your inbox, sign up for our daily newsletter .

Why travel insurance usually doesn't cover epidemics and pandemics

In general terms, regular travel insurance policies cover the "unknowns" — for example, an accident you couldn't have anticipated in advance, such as falling while you were hiking and breaking your leg — and not losses caused directly or indirectly by known or foreseeable events (in this case, an epidemic complete with government travel advisories).

Similar to a weather event , once something becomes "known" it may not be a covered reason for cancellation if a traveler purchases insurance after that date.

In other words, if you purchased travel after the World Health Organization (WHO) declared COVID-19 a pandemic, you've entered "known" territory, the same as deciding to fly into the eye of a hurricane.

Related: Avoiding outbreaks isn't covered by most travel insurance

What travel insurance normally covers

"Essentially, travel insurance covers unexpected events during your travels and pre-departure starting the effective date of your policy," said Christina Tunnah, general manager of the Americas of travel insurance company World Nomads.

According to Tunnah, regular travel insurance breaks down into three main categories:

- The protection of your pocketbook (investment in flights, delays, interruption, cancellation)

- The protection of yourself (emergency medical and evacuation)

- The protection of your belongings ( delayed and lost bags , theft)

Many credit cards also offer travel protection. Covered situations, maximum coverage amounts and eligible expenses vary across the cards that offer this benefit. Covered situations typically include accidental bodily injury; loss of life or sickness; severe weather; terrorist action or hijacking and jury duty or a court subpoena that can't be postponed or waived.

Related: The best credit cards with complimentary travel protection

Are some insurers covering COVID-19?

Not all the news on the COVID-19 insurance front is negative. According to Walch, many traditional travel insurance policies will cover your COVID-19 related travel concerns if you meet regular guidelines.

Examples of COVID-19 coverage in traditional plans include:

- If you must visit a doctor or hospital during a trip due to a COVID-19 illness

- If you get sick with COVID-19 and must cancel a trip

- If a physician orders you to quarantine before a trip

- If you lost a job during the coronavirus pandemic by no fault of your own

In addition, some plans are now offering higher travel delay limits in order to help with additional accommodation expenses due to a covered quarantine, adds Walch.

And, there are also some individual insurers that are simply covering COVID-19 outright. For example, World Nomads' plans cover the diagnosis of COVID-19 the same as any other illness with benefits that could include emergency medical care, emergency medical evacuation, trip delay and trip interruption coverage if you contract COVID-19 while traveling.

How to find a plan that covers COVID-19

First of all, you should look in the exclusion section to see if pandemics or epidemics are mentioned. If so, you'll need to shop around for a different policy, said Tunnah.

Even though travel insurance companies may offer COVID-19 sickness coverage, they typically don't offer benefits for every circumstance.

"Every policy is different, so you'll want to get a good grasp of a plan's coverage before you purchase it," Tunnah explained. Some of the questions you should ask yourself are: Does the plan cover emergency medical and evacuation expenses if I contract COVID-19? What are covered reasons for cancellation? What if my trip is delayed or interrupted because of a COVID-19 event?

If you're getting confused from reading the legal jargon of a policy, you can contact the customer service department of your travel insurance company, Tunnah advised. Representatives should be able to provide plain English explanations of coverage and help you identify a plan that meets your specific trip needs.

To see multiple options in one place, InsureMyTrip has a COVID-19 coverage tool that allows you to compare different policies.

Here's what you should be looking for according to the company:

- Trip cancellation coverage: While traditional trip cancellation does not allow a traveler to cancel a trip due to COVID-19 fears, it may cover a traveler in the event they get sick from COVID-19 and must cancel a trip.

- Trip interruption coverage: In the event a traveler gets sick from COVID-19 and the trip is interrupted, this coverage may apply.

- Cancel for any reason coverage : If eligible, this protection allows travelers the option to cancel a trip due to concerns over COVID-19, whereas traditional trip cancellation coverage does not (see below for more details).

Cancel for any reason insurance could be your best option

Cancel for any reason, also known as CFAR in the insurance industry, is an add-on to certain traditional trip insurance policies.

While travel insurance policies can offer a range of inclusions (think: medical evacuation, trip cancellation due to foreign or domestic terrorism or rental car damage) not every eventuality is included in all insurance policies. For example, some trip insurance plans cover employment layoffs while others do not. Some policies may have robust emergency medical coverage while competitors don't. That's why it's so important for you to select a plan that meets your specific needs for each trip.

One commonality among insurance policies? A long lists of exclusions. That's where a CFAR policy comes into play.

" InsureMyTrip strongly recommends travelers strongly consider a CFAR upgrade," said Walch. This upgrade offers the most trip cancellation flexibility and is the only option available to cover "fear of travel" (traditional travel insurance does not offer cancellation coverage for "fear of travel," whether related to COVID-19 or not).

If eligibility requirements are met, reimbursement is typically up to 70% of the pre-paid, nonrefundable trip cost. "Just be aware that this add-on will increase the cost of the plan," Walch advised.

Some countries are requiring mandatory insurance for entry

Even in pre-pandemic times, many countries required travelers to have personal medical insurance to visit (although you weren't necessarily required to provide proof). Now, with pandemic concerns, some countries are instituting mandatory COVID-19 insurance for entry.

The Bahamas is one example. Travel health insurance is required for all incoming visitors and the cost for the mandatory insurance is included in the price of the Travel Health Visa all tourists are required to apply for before entry. Aruba is another example where COVID-19 insurance is purchased onsite at arrival and mandatory for entry.

Note that these insurance coverage policies just are for medical coverage, so travelers will still need additional coverage to cover non-health-related expenses such as travel delays or lost baggage.

Bottom line

If you're planning on traveling during a pandemic, don't assume that your usual travel insurance will cover you. Be sure to compare different insurance policies. and strongly consider Cancel For Any Reason insurance if you want to make sure your trip costs are covered.

- Small Business

- English Selected

COVID-19 (Coronavirus) Frequently Asked Questions

- Credit Cards

Personal Banking

Business Banking

International Mail Interruptions

How can i see my td account statements if i live in a country affected by mail service suspensions.

Due to COVID-19, many countries outside of Canada and the US are not accepting mail causing Canada Post to suspend its international mail service. Learn more .

You can bank with us securely online through EasyWeb and with your mobile through the TD app. If you have questions on how to bank with us online, including viewing your various account balances and transaction history, check out our Digital Banking tutorials.

Daily Banking

How is td helping community-based organizations at this time.

The COVID-19 pandemic has had an immense impact on society and that's why this year, we have made the decision to focus the 2020 TD Ready Challenge on supporting innovative solutions that address the impacts of the pandemic. This year's TD Ready Challenge is part of the $25 million (CAD) that TD has allocated to help strengthen community resilience and COVID-19 recovery through the TD Community Resilience Initiative , a part of the TD Ready Commitment , the Bank’s corporate citizenship platform. This comprehensive program includes funding, employee engagement and on-going collaboration with organizations and community groups that operate locally, regionally and nationally in Canada and the United States across TD's operating footprint.

How is TD protecting customers and TD colleagues from COVID-19?

We are advising TD colleagues to follow health and safety policies we have established at TD in accordance with applicable public health guidelines. TD colleagues complete a health screening before coming to work each day, and any colleague who is unwell must not come to work. We are limiting the number of colleagues and customers in the branches at any one time, and continue to follow physical distancing protocols. Face coverings are mandatory for all colleagues while on TD premises and mandatory for customers where required by law. We have installed plexiglass and physical distancing markers in all branches and have hand sanitizers for colleagues and customers.

I'm seeing an increase in phishing emails relating to COVID-19, how do I know which ones are legitimate?

As the situation with COVID-19 evolves it is important that we all remain vigilant in protecting ourselves against fraud. TD will never send you unsolicited emails asking for confidential or personal information, such as your password, PIN, Access Code, credit card and account numbers. Here are some additional tips and best practices to consider:

- Be wary of suspicious emails – do not open attachments or click on embedded links in emails that you do not trust. By opening an attachment or clicking on an embedded link, you could unknowingly download malicious software onto your device

- The Canadian Bankers Association is also cautioning against email scams related to COVID-19

What is the transaction limit to tap to pay with my TD Credit Card or my TD Access Card (contactless transactions)?

For TD Credit Cards, we've temporarily increased the transaction limits for credit cards when you tap your credit card or eligible mobile wallet (e.g., Apple Pay, Samsung Pay & TD Wallet) to make a purchase. A single purchase transaction using your TD Credit Card cannot exceed $250*. Some merchants may have set a lower tap limit (often $100). In the cases where your purchase is above $250 or above the merchant's tap limit, you will be asked to insert your card and enter your PIN in order to authorize the purchase. For TD Access Cards, the limit for a single purchase transaction cannot exceed $250 when you use tap or your mobile wallet. If your purchase is above this amount, you will be asked to insert your card and enter your PIN in order to authorize the purchase.

I recently received notice of upcoming changes to credit card pricing. Will that still be coming into effect?

We know how challenging the current environment has been for our customers, colleagues and communities. In consideration, we have chosen to focus our efforts on providing guidance and support to those experiencing financial challenges, and as a result we will not be moving forward with the following planned changes to our credit card terms at the current time:

- How we calculate interest on all personal credit cards

- The introduction of an Overlimit fee on TD First Class Travel ® Visa Infinite * Card, TD ® Cash Back Visa Infinite * Card, TD ® Aeroplan ® Visa Infinite * Credit Card

- Annual Interest Rate changes if we don’t receive your Minimum Payment before or on the Payment Due Date twice within any 12 consecutive months for all personal credit cards

Branch Access

Are you reopening td branches that were temporarily closed due to covid-19.

We have been thoughtfully reopening branches across the country with the health and safety of our colleagues and customers as our guiding principle. While the majority of our branches are now open with changes to help safeguard health and safety, we will continue to review and adjust our operations to meet the needs of our customers and adhere to guidance from public health officials. We continue to encourage our customers to bank digitally or at the ATM where possible

How can I book an appointment at my local TD Branch?

If you require assistance for borrowing, investing or other financial advice, please book an appointment and we would be pleased to serve you at a branch or by phone. You can book an appointment using our online appointment booking tool, the TD app or by calling your local open branch and pressing 6. You can book an appointment from 2 different places within the TD app. The Branch Locator Tool, at the bottom left corner of the TD app home screen and the Contact Us screen, which you can find at the bottom right corner of the TD app home screen.

How can I take care of my banking needs if I don't want to leave my home or a branch is closed?

- Online and mobile banking is a convenient way for you to check your balance, send money, pay bills, deposit cheques, or find the nearest TD ATM. Our Contact Centres are also open to help you.

- Check out our Digital 'How To' for a step by step guide to getting started.

- Contact centers: For the health and safety of customers over 75, as well as healthcare professionals, we now utilize existing account information to identify your call and automatically prioritize it in queue.

- Due to the ongoing increase in COVID-19 related inquiries, you may experience longer wait times when you call our Contact Centres. We appreciate your patience.

How are you supporting seniors and customers who require special assistance?

If you are a Senior, or vulnerable customer who may need special assistance with your banking needs, our branch staff will be available to help provide priority access when arriving at the branch should you require it. We will do our best to prioritize customers who need extra assistance and branch staff will proactively offer this support throughout the day.

Customers can also take advantage of our priority EasyLine access, which is automatic for customers 75+, and will provide you with an alternate option to bank safely from the comfort of your home, 24 hours a day and seven days a week. You can access this line by calling Easyline, or the priority access service number directly, where you will be automatically provided priority service by being placed at the front of the queue.

In addition, we have other options available, so you don't have to wait or come into a branch. You can bank anytime using branch ATMs, EasyWeb Online Banking, EasyLine Telephone Banking and the TD app. You can also book an appointment before coming into the branch to avoid a line.

What do I do if I need to pick-up or order foreign currency, and my branch is closed?

Unfortunately, you will have to wait until your branch reopens, or use our branch locator to find an open branch to fulfill your foreign currency needs. Any deliveries requested to branches which have closed will only be available for pick-up once the branch has reopened. This decision has been taken in the interest of public safety.

I have a Safety Deposit box in a closed branch – can I still get access to it?

Yes, please call your local branch to confirm access and request an appointment. If there is no answer, please press six and leave a message.

Minimum Payment Deferral Option

What is minimum payment deferral option.

As a part of our commitment to help our customers deal with potential financial hardship, we had made a Minimum Payment Deferral option available to customers, which allowed them to defer the minimum payment for 3 months.

Applications for this option ended on Nov 30, 2020.

If I have a monthly pre-authorized payment set up to pay my credit card account, will this payment stop for the 3-month duration of the minimum payment deferral?

No, it will not stop the payment from being withdrawn from your account. If you currently have pre-authorized payments set up from your account to pay your minimum payment, you will need to contact your bank to pause payments from automatically being withdrawn. If your payment is coming out of a TD account, please contact us at 1-800-983-8472 .

Will interest accrue with the Minimum Payment Deferral option?

If you have chosen to defer your payments through the Minimum Payment Deferral program, interest that has accrued during the deferral period will be added to your outstanding balance as set out in your Cardholder Agreement and Disclosure Statement.

On month 4, when the deferral period is over, your minimum payment will continue as outlined in your Cardholder Agreement and Disclosure Statement.

I have signed up for the Minimum Payment Deferral option, should I stop making any payments if I feel like I can afford to?

If you are able to make any payments during the Minimum Payment Deferral window, we would strongly recommend that you continue to make whatever payments you can. All these payments will help to reduce the amount outstanding and due upon Month 4 when the Minimum Payment Deferral option expires.

If I sign up for the Minimum Payment Deferral option, what if I change my mind?

Once you submit a request for the Minimum Payment Deferral option, you cannot cancel it. If you wish to make any payments, simply make any payments each month and we will apply these payments as outlined in your TD Credit Cardholder Agreement .

Will my balance protection insurance continue for the duration of the Minimum Payment Deferral program?

Yes, if you have a balance protection insurance, your premiums will continue to be changed and your credit card account will continue to be insured during the deferral period.

Will my credit report or credit score be impacted if I defer a credit card payment through the TD Helps financial relief programs?

If approved for a payment deferral, we will report to the credit bureaus that the underlying is "deferred". A deferred payment is not considered the same as a missed payment on credit bureaus or credit scores. We do not report a COVID-19 related "deferred payment" as a "missed payment".

Your credit score is calculated using a formula based on your credit report and reflects various factors. One of the factors that may affect your credit score includes the amount of your outstanding debts – which may increase as a result of a payment deferral.

For more information about credit reports and your credit score, you can visit the Financial Consumer Agency of Canada (FCAC) site , or contact the credit bureaus (also known as the credit reporting agencies), Equifax Canada and TransUnion Canada, directly.

Dispute a transaction

How do i request a transaction dispute.

If you would like to dispute a transaction on your account statement, simply complete and submit a transaction dispute request within 60 days of the credit card statement closing date.

I have a credit for goods or services that I didn’t use, but now the merchant is bankrupt. What can I do?

While we empathize with the situation, there are no dispute rights in play here since you are voluntarily choosing not to use the services and the voucher was offered as a courtesy.

I can’t use the voucher I took from a merchant when they cancelled a service as they’re bankrupt. Can I dispute?

You must first attempt to resolve the dispute with the merchant after the original expected date of receipt. Although we are asking for clients to be flexible, if the merchant fails to provide the service by the expected date, you may have dispute rights. Please contact us so we can start an investigation.

I'm expecting a refund, but I haven't seen it posted to my account. What can I do?

Because companies can take up to 15 business days to issue a refund, we cannot begin our investigation until that time has expired. If it has been at least 15 days since the refund was issued, please contact us so we may start an investigation.

You can also check your most recent transactions online through EasyWeb. If you have not set up an online banking profile you can do so by going to EasyWeb and clicking on the register online now button.

I ordered merchandise/services from a merchant and I still haven’t received them, can a dispute be filed?

You must first attempt to resolve the dispute with the merchant after the expected date of receipt. Although we are asking for clients to be flexible, if the merchant fails to provide the merchandise by the expected date, you may have dispute rights. Please contact us so we can start an investigation.

I haven’t been able to return an item within the timeframe, and now the store is closed down. Can I dispute?

You must first attempt to resolve the dispute with the merchant as some merchant have extended their return window during this time. Although we are asking for clients to be flexible, if the merchant fails to follow their cancellation/return/refund policies, please contact us so that we may start an investigation.

I bought tickets for an event that was rescheduled, but I can’t make the merchant’s new date. What do I do?

Please contact the merchant and attempt to resolve before contacting us. You are not required to accept an alternate date. If the dispute cannot be resolved with the merchant, we may be able to dispute the transaction.

If I choose to miss an event due to fear of the virus and cancel my tickets, can I dispute for non-receipt?

While we empathize with the situation, unfortunately if the event is scheduled as planned and the merchant is willing and able to provide the service there would not be dispute rights for this situation under non-receipt. If you canceled the tickets, the merchant’s cancellation and/or refund policy would apply.

Note: If services/tickets were purchased through third-party resale sites, the refund policy of that third-party sale would apply—not the refund/cancellation policy of the original merchant.

I’ve purchased a proprietary gift card from a merchant. The merchant went out of business so now I can’t use any goods or services, or a refund. What should I do?

Please contact the merchant and attempt to resolve before contacting us. As the gift card represents purchased services, and the merchant is now unable to provide the services, we may be able to dispute. Please contact us to start an investigation.

I purchased a gift card from a 3rd party, and the merchant on the card has closed. Can I dispute the charge?

Please contact the merchant of record (such as grocery store) and attempt to resolve with them before contacting us. If you are unable to resolve with that merchant, please contact us to start an investigation.

TD Helps - Mortgage Deferrals

What is a mortgage payment deferral.

A mortgage payment deferral is a temporary pause on mortgage payments. Once the deferral ends, the principal and accumulated interest will still need to be repaid.

What happens after my mortgage deferral period is over?

After your deferral, your regular mortgage payments will remain the same until the term is renewed or you make any other change to your payments (e.g. amount, payment date, or frequency). One of these changes might result in your payment being higher to ensure your mortgage is paid off within the amortization period that was agreed upon when your mortgage agreement was originally signed.

What if I want to change or cancel my mortgage payment deferral?

You can contact us to discuss changes or cancellation in a number of ways. Call our Contact Centre at 1-888-720-0075 , speak to someone online with Click to Chat through EasyWeb, or talk to somebody in one of our branches. You can use our Branch Locator to find a location near you that's open. Remember that, with your health in mind, we've temporarily closed or reduced hours at some branches, and you may experience longer than usual call wait times.

My mortgage is coming up for renewal. Given the current situation with Coronavirus and COVID-19, what is the best way to renew my mortgage?

Currently, the fastest and easiest way to renew your mortgage is through EasyWeb® Online Banking or the TD app—and you can get it done from the comfort of your own home.

You'll be able to review your current mortgage rate and terms and compare them against a range of other options we have for you.

It only takes a few simple steps:

- Log in to EasyWeb or the TD app, and click on your Mortgage account

- Click Renew Now to review your options and select one

- Review the Mortgage Renewal Agreement and accept the terms and conditions

Can I make a lump sum payment on my mortgage?

You are able to make a lump sum payment but there may be a prepayment charge if it exceeds a certain amount. You can refer to your Mortgage Loan Agreement for more information. You can also call our Contact Centre at 1-888-720-0075 , or speak to someone online with Click to Chat through EasyWeb to get details on your options .

TD Home Equity FlexLine Term Portion Deferrals

What happens when my td home equity flexline term portion the payment deferral period is over.

If you deferred both principal and interest, when your deferral period ends your payments will begin again and be applied to the interest accrued during the deferral period first. Once all interest owed is repaid your payments will start going towards your principal (plus interest) again as normal. You can find the date your payments will resume along with additional cost of borrowing information in the Confirmation of the Changes to your TD Home Equity FlexLine/Home Equity Line of Credit that was mailed to you.

If you deferred your principal, when your deferral period ends your payments will begin again. You can find the date your payments will resume along with additional cost of borrowing information in the Confirmation of the Changes to your TD Home Equity FlexLine/Home Equity Line of Credit that was mailed to you.

We're also ready to help you with any questions you may have. Give us a call at our Contact Centre at 1-888-720-0075 , click to Chat through Easy Web , or talk to somebody in branch. You can use our Branch Locator to find a branch near you that's open.

My TD Home Equity FlexLine Term Portion is coming up for renewal. Given the current situation with Coronavirus and COVID-19, what is the best way to renew?

You can renew your TD Home Equity FlexLine by visiting your local branch or calling 1-800-450-7320 . You can use our Branch Locator to find a branch near you that's open and book an appointment at an open branch with our Branch Appointment Booking Tool .

Payment Deferrals – Impact to Credit Report

Will my credit report or credit score be impacted if i defer a mortgage, td home equity flexline term portion, personal loan or credit card payment or other payment deferral through td's covid-19 financial relief programs.

If you were approved for a COVID-19 payment deferral, we reported to the credit bureaus that the payments were "deferred". A deferred payment is not considered the same as a missed payment on credit bureaus or credit scores. We do not report a COVID-19 related "deferred payment" as a "missed payment".

Credit protection

How do i defer my td credit protection insurance premiums.

You can request a deferral of your insurance premium charges through an online application. Our call centre and branch staff are also able to assist you with this deferral request. Call our Contact Centre at 1-888-720-0075 or contact a branch.

How many months can I defer my TD Credit Protection premiums for?

You can request to defer your TD Credit Protection insurance premium charges for up to 6 months for a mortgage or TD Home Equity FlexLine, and up to 4 months for a personal line of credit or personal loan. At the end of the deferral period, you will have up to 12 months to repay deferred premium charges. The deferral period and repayment period cannot extend beyond your coverage end date. You can request a deferral of your insurance premium charges through the online application .

How many insured borrowers can request a deferral of TD Credit Protection insurance premium charges?

A separate request is required for each insured person and for each insured credit product account. Not all insured persons need to defer premiums on the same credit product for premium charges to be deferred for any one insured person.

What happens if I need to make a claim during my TD Credit Protection premium deferral period?

Your coverage will not terminate during the deferral and repayment periods if your request to defer premium charges is approved. If you need to make a claim during either of these periods, just complete a claim through the usual process. However, please note that in the event of an approved claim, any deferred premiums owing at the time of claim will be deducted from the total amount of the claim benefit payment and/or required to be paid by you if the benefit amount doesn't cover the outstanding premiums.

If you would like to dispute a transaction on your account statement, simply complete and submit a transaction dispute request within the following timeframe:

- TD Credit Card: within 60 days of the credit card statement closing date

- TD Access Card: within 30 days of the date you have received notice of the transaction as per your account agreement

I haven’t been able to return an item within the timeframe, and now the store has closed down. Can I dispute?

You must first attempt to resolve the dispute with the merchant as some merchants have extended their return window during this time. Although we are asking for clients to be flexible, if the merchant fails to follow their cancellation/return/refund policies, please contact us so that we may start an investigation.

I’ve purchased a proprietary gift card from a merchant that went out of business. What should I do?

My trip has been cancelled by the airline due to low demand. what can i do.

Many airlines are offering to waive fees, change flights or possibly refund in-full. Please attempt to resolve this with the Airline, before contacting us. Merchants may be experiencing heavy call volumes. We are encouraging cardholders to please visit the merchant websites to resolve the matter. If you are unable to resolve and your date of travel has passed, please contact us and we will try to help.

My flight was cancelled too late for me to cancel my hotel reservation. Can I dispute the hotel charge(s)?

Since the merchant is willing and able to provide the hotel stay, the merchant is entitled to be paid for one night’s accommodation. We encourage you to continue to work with them for a mutually agreeable outcome.

I can’t get to my cruise departure destination due to a cancelled flight. Do I have a valid dispute?

While we empathize with the situation, the cruise merchant is expecting to be paid as they are willing and able to provide the cruise. We encourage you to work with them for a solution. Many cruise lines are offering to waive fees to change bookings or possibly offer vouchers for alternate dates. However, if the cruise line was responsible arranging your flight - we might be able to assist. In this case, please contact us, so we may start an investigation.

Can I get money back for out-of-pocket expenses incurred by making new travel arrangement based on advisories?

As these charges are not disputable we are limited to the value of the transaction. We encourage you to continue to work with the merchant for a mutually agreeable solution. If your new travel arrangements are separate from your original booking, and after contacting the merchant you were unable to resolve the dispute, please contact us so we may start an investigation on the original booking.

If I choose not to take a trip due to fear of the virus and cancel, can I dispute charges?

While we appreciate your safety concerns, if the travel merchant is willing and able to provide the service then their cancellation and/or refund policy would apply. This would need to be handled separately for each aspect of your itinerary (e.g., airline, hotel and rental car agency). Note : If services/tickets were purchased through third-party resale sites, the refund policy of that third-party sale would apply—not the refund/cancellation policy of the original merchant.

Travel Insurance

Where can i find information about travel insurance policies related to my td credit card.

The Cardholder Agreement for your TD Credit Card contains important and useful information relating to specific Travel Insurance Policies. Please review your Cardholder Agreement online.

I have a TD Credit Card that I used to book a trip, does it include Trip Cancellation Insurance?

The following TD Credit Cards include Trip Cancellation coverage:

- TD® First Class Travel® Visa Infinite* Card

- TD® Aeroplan® Visa Infinite Privilege* Card

- TD® Aeroplan® Visa Infinite* Credit Card

- TD® Business Travel Visa* Credit Card

My TD Credit Card comes with Trip Cancellation Insurance. Will I be covered if I cancel my trip due to a travel advisory for COVID-19?

A customer may be eligible for coverage if they charged their trip (in full) to their TD Credit Card that offers Trip Cancellation Insurance, before an “Avoid all Travel” or “Avoid non-Essential Travel” travel advisory was issued by the Government of Canada for their destination. However, please note that each Trip Cancellation claim is evaluated on an individual basis.

An updated list of Travel Advisories can be accessed here .

More information about benefits, features, coverage and exclusions can be found in the Certificate of Insurance included in the Credit Cardholder Agreement. Cardholder Agreements for each product are below:

- TD® Business Travel Visa* Card

Travel cancellation and modification

How do i make a trip cancellation claim.

24 Hour Emergency Assistance Number

Interruption, Trip Cancellation, you can call our provider 24 hours a day/7 days a week:

- From the U.S.A. or Canada 1-866-374-1129

- From elsewhere, call collect 416-977-4425

Customer Service Phone Number

For more general customer service questions, you can call the provider at:

1-866-374-1129 or (416) 977-4425

Monday – Saturday 8 a.m. – 8 p.m. Eastern Time

What should I do if I want to modify or cancel a trip booked through Expedia For TD?

For support with a current or past booking , contact the Expedia For TD call center at 1-877-222-6492 . You will be asked to provide your itinerary number or phone number before speaking to an agent to confirm your travel dates. To assist the most urgent cases, please consider calling closer to your travel dates.

For upcoming travel cancellations , you may be able to submit an Online Cancellation Request. By completing the Online Cancellation Request Form, you give permission to Expedia For TD to contact the travel supplier and cancel your reservation. Please note that any refunds are subject to the policy of the airline or travel provider you are booked with. For more information on online cancellation, please check out Expedia For TD Customer Service Portal for COVID-19 Support .

What should I do if I want to modify or cancel a trip booked through Aeroplan?

For TD Aeroplan trip cancellations all of the miles will be returned to your account, and any fees you paid for your booking will be returned to your original method of payment. Simply log-in at Aeroplan and visit Manage your bookings.

If you want to change your Aeroplan Flight Reward to travel on a different date without cancelling the booking, you must call the Aeroplan Contact Centre at 1-800-361-5373 . Please note that Aeroplan is experiencing a high volume of calls related to COVID-19. If you are not travelling within the next 3 days, please consider calling at a later time. For all other information around Air Canada route suspensions, please visit Air Canada COVID-19 Updates .

While we appreciate your safety concerns, if the travel merchant is willing and able to provide the service then their cancellation and/or refund policy would apply. This would need to be handled separately for each aspect of your itinerary (e.g., airline, hotel and rental car agency).

Note : If services/tickets were purchased through third-party resale sites, the refund policy of that third-party sale would apply—not the refund/cancellation policy of the original merchant.

Canada Emergency Business Account (CEBA) Frequently Asked Questions

All application outcomes and repayment deadlines for the ceba are now final.

All program eligibility determinations, application outcomes and repayment deadlines are now final and cannot be changed. As an administrator for the CEBA program, TD does not have the authority to grant exceptions to the CEBA eligibility criteria.

Where can I get more information about CEBA?

- Full details are provided on the Government of Canada CEBA website: https://ceba-cuec.ca/

What is the CEBA?

The Government of Canada established the CEBA program to support Canadian businesses adversely affected by COVID-19. Eligible businesses received a loan for immediate financial support to cover short term operating expenses, payroll and other non-deferrable expenses critical to sustain business continuity.

CEBA details are as follows:

- A $40,000 interest-free (until January 18, 2024), government funded loan for eligible borrowers in good standing to help pay for operating costs that businesses were not able to defer as a result of COVID-19. If the CEBA loan is not repaid by January 18, 2024 or March 28, 2024, as applicable, it will be extended until December 31, 2026 and bear interest at 5% per annum payable monthly.

- $10,000 of the $40,000 TD CEBA loan is eligible for forgiveness if $30,000 of the loan is fully repaid on or before January 18, 2024 or March 28, 2024 if a refinancing application is submitted to TD by January 18, 2024 (provided that interest shall commence on January 19, 2024).

- A $60,000 interest-free (until January 18, 2024), government-funded loan for eligible borrowers in good standing to help pay for operating costs that businesses were not able to defer as a result of COVID-19. If the CEBA loan is not repaid by January 18, 2024 or March 28, 2024, as applicable, it will be extended until December 31, 2026 and bear interest at 5% per annum payable monthly.

- $20,000 of the $60,000 TD CEBA loan is eligible for forgiveness if $40,000 of the loan is fully repaid on or before January 18, 2024 or March 28, 2024 if a refinancing application is submitted to TD by January 18, 2024 (provided that interest shall commence on January 19, 2024).

- If the loan is not repaid by January 18, 2024 or March 28, 2024, as applicable, it will be extended until December 31, 2026 bearing an interest at a rate of 5% per annum. Starting January 19, 2024, the CEBA loan interest will be payable monthly and all outstanding CEBA loans must be repaid in full by December 31, 2026.

- Lumpsum payments can be applied to the loan at any time without penalty.

- TD CEBA Loans must be repaid in full by December 31, 2026

On September 14, 2023, the Government of Canada announced that the repayment deadline for partial loan forgiveness has been extended from December 31, 2023 to January 18, 2024 or March 28, 2024 if a refinancing application is submitted to TD by January 18, 2024 for eligible TD CEBA loan holders in good standing, how does this impact my CEBA loan?

For eligible TD CEBA loan holders in good standing , the following are the key changes and related important dates affecting their CEBA loan:

- January 18, 2024/March 28, 2024 – For eligible TD CEBA loan holders in good standing, the non- forgivable portion of a CEBA loan must be repaid by January 18, 2024 or March 28, 2024 if a refinancing application is submitted to TD by January 18, 2024 (provided that interest shall commence on January 19, 2024) to be eligible for partial loan forgiveness.

- January 19, 2024 – Outstanding CEBA loan balances will be extended until December 31, 2026, with an interest rate of 5% per annum. Monthly interest payments are required.

- December 31, 2026 – Outstanding CEBA loans must be fully repaid by this date.

Eligible TD CEBA loan holders in good standing that have submitted a refinancing loan application to TD by January 18, 2024 and require time to finalize the payout of their TD CEBA loan may qualify for partial loan forgiveness if the outstanding principal of their CEBA loan, other than the amount eligible for forgiveness is repaid by March 28, 2024 (provided that interest shall commence on January 19, 2024).

I have received a communication from TD, on behalf of the Government of Canada, that states that if my CEBA loan is not repaid before the January 18, 2024 deadline interest will be charged at a rate of 5% per annum. Where will the interest payments be debited from?

Interest will commence on January 19, 2024 and monthly interest payments will be debited from the Business Chequing Account where the CEBA proceeds were credited. If the account the CEBA loan was originally credited to has been closed, please ensure that a new Business Chequing Account number has been provided to TD for pre-authorized debit for the monthly payments.

I have received a communication from TD, on behalf of the Government of Canada, notifying me that I was not eligible for the CEBA loan I received. Who can I contact to find out the reasons behind this decision?

If you have questions about your CEBA eligibility, please contact the CEBA Call Centre at 1-888-324-4201. All decisions pertaining to CEBA loan applications are final, including determination of compliance with CEBA eligibility criteria and approval/decline. Eligibility decisions are made by the Government of Canada.

How can I make payments to my CEBA loan?

Payments can be made via a TD Canada Trust Branch, TD EasyLine (1-855-646-8804), or online through EasyWeb and the TD mobile app. CEBA loans cannot be set up for automated monthly principal payments however lump sum payments can be made at any time using the channels listed above.

I have recently repaid the non-forgivable portion of my CEBA loan. Why does the CEBA loan still show on my banking profile?

Your account will be automatically closed within 21 days of repayment, and a loan closure letter will be mailed to you in 3 - 5 business days after the loan account is closed.

Please note if we and/or the Government of Canada and/or its respective agents and/or consultants determine after the date of repayment that you did not satisfy all of the eligibility requirements for partial CEBA loan forgiveness, including if you were in default under your CEBA Loan Agreement on the date of your repayment, you will be required to repay any amount forgiven.

I will be closing my business and I still have an outstanding CEBA loan, what actions do I need to take?

Business closure renders the CEBA loan immediately due and payable however your business may still be eligible for partial loan forgiveness. Please contact your local Account Manager or EasyLine Business Banking Specialist (1-855-646-8804) to make the necessary arrangements to repay the CEBA loan.

Is the forgivable portion of my CEBA loan taxable?

For any taxation questions relating to your CEBA loan, please contact the Canada Revenue Agency (CRA) or your tax professional for further information.

See you in a bit

You are now leaving our website and entering a third-party website over which we have no control.

TD Bank Group is not responsible for the content of the third-party sites hyperlinked from this page, nor do they guarantee or endorse the information, recommendations, products or services offered on third party sites.

Third-party sites may have different Privacy and Security policies than TD Bank Group. You should review the Privacy and Security policies of any third-party website before you provide personal or confidential information.

TD Personal Banking

- Personal Home

- My Accounts

- Today's Rates

- Accounts (Personal)

- Chequing Accounts

- Savings Accounts

- Youth Account

- Student Account

- Aeroplan points

- Travel Rewards

- No Annual Fee

- U.S. Dollar

- Personal Investing

- GIC & Term Deposits

- Mutual Funds

- TFSA - Tax-Free Savings Account

- RSP - Retirement Savings Plan

- RIF - Retirement Income Options

- RESP - Education Savings Plan

- RDSP - Disability Savings Plan

- Precious Metals

- Travel Medical Insurance

- All Products

- New To Canada

- Banking Advice for Seniors (60+)

- Cross Border Banking

- Foreign Exchange Services

- Ways to Pay

- Ways to Bank

- Green Banking

TD Small Business Banking

- Small Business Home

- Accounts (Business)

- Chequing Account

- Savings Account

- U.S. Dollar Account

- AgriInvest Account

- Cheque Services

- Overdraft Protection

- Line of Credit

- Business Credit Cards

- Business Mortgage

- Canada Small Business Financial Loan

- Agriculture Credit Solutions

- TD Auto Finance Small Business Vehicle Lending

- Invest for your Business

- Advice for your Profession or Industry

- TD Merchant Solutions

- Foreign Currency Services

- Employer Services

TD Investing

- Investing Home

- Direct Investing

- Commissions and Fees

- Trading Platforms

- Investment Types

- Investor Education

- Financial Planning

- Private Wealth Management

- Markets and Research

TD Corporate

- Investor Relations

- Environment

- Supplier Information

- TD Newsroom

Other TD Businesses

- TD Commercial Banking

- TD Asset Management

- TD Securities

- TD Auto Finance

U.S. Banking

- TD Bank Personal Banking

- TD Bank Small Business Banking

- TD Bank Commercial Banking

- TD Wealth Private Client Group

- TD Bank Personal Financial Services

Advertisement

Supported by

Omicron and Travel: So, Now Do I Need Trip Insurance?

In light of the new variant, is extra protection warranted for things like flight and lodging cancellations and quarantine hotels? It depends. Here’s what you need to know.

- Share full article

By Elaine Glusac

While the pandemic has depressed travel, it may have encouraged travel insurance, say those in the industry.

“The biggest question we get from customers is: ‘What happens if I get Covid during travel and what if I have to quarantine?’” said Jeremy Murchland, the president of Seven Corners , a travel insurance management company. “Covid has created a much broader awareness of travel insurance.”

But will it help you in light of the new Omicron variant, which has already led to new travel restrictions and requirements? In the early days of the pandemic, travel insurance largely failed to protect travelers who wanted or needed to cancel as the world shut down. The following are answers to common questions about travel insurance now.

Does travel insurance cover Covid-19, including the new Omicron variant?

For the most part, yes, travel insurance policies now treat Covid-19 in all its variants — including Omicron — like any other medical emergency.

“Consumers should know that most travel insurance plans with medical benefits now treat Covid like any other illness that you could contract while traveling or that could prohibit you from going on your trip,” said Carol Mueller, a vice president of Berkshire Hathaway Travel Protection . “If you become ill before your trip, you’ll need a doctor’s note confirming your illness and that you are unable to travel in order to be eligible for benefits. The benefits are the same regardless of whether you contract Omicron, another variant of Covid or any illness for that matter.”

Buyers should read the policies carefully and look out for those that exclude pandemics, Covid-19 and its variants. To make a claim, you must have had travel insurance before becoming ill.

“We always say, you can’t buy auto insurance after you’ve already had an accident,” said Meghan Walch, the product manager of InsureMyTrip , an insurance sales site. “It is designed for unforeseen issues. You have to purchase it before an event.”

I am traveling internationally. If borders close because of Omicron, am I covered through travel insurance?

No, most policies do not cover you if your foreign destination closes its borders to visitors, as Israel did recently. With a few exceptions, that also goes for a government-issued travel warning to a destination, which is generally not a covered reason to make a claim.

Given the added uncertainties of Omicron, should I consider a ‘Cancel for Any Reason’ policy?

Cancel for Any Reason, or C.F.A.R., provisions would allow you to claim some of your nonrefundable costs if you decide not to go on a trip for any reason, including border closures or fear of contracting Covid. The rub is that this form of insurance — in addition to being more expensive — must generally be purchased within a few weeks of booking the trip and will only return 50 to 75 percent of nonrefundable trip costs.

“Most travel insurance policies do not cover you for wanting to cancel out of fear of Covid. We say this 10 times a week,” said Sarah Groen, the owner of the agency Bell and Bly Travel . She counsels clients to consider their worst fears — illness, for example, or quarantine — in troubleshooting travel insurance. “We’ve become like therapists,” she said.

What about quarantine and medical expenses?

Make sure the policy you choose covers these. In the case of medical coverage, check with your regular health insurer; many policies will not cover you abroad, which is an additional reason to consider coverage if you are traveling internationally.

“What travel insurance can do is cover additional hotel stays if you are able to self-quarantine and additional airfare when you’re able to come home,” said Megan Moncrief, the chief marketing officer for Squaremouth , a travel insurance sales site. She added that most policies will extend to seven days past your originally scheduled return date, effectively covering only about seven days in case of quarantine.

Do some destinations require travel insurance?

Yes, primarily to cover medical care or quarantine accommodations in the event that a traveler tests positive for Covid-19. For example, Singapore requires medical insurance with a minimum coverage of 30,000 Singapore dollars, or about $22,000. Fiji requires travel insurance to cover potential treatment for Covid-19, and makes it available from about $30. Some destinations, such as Anguilla , recommend rather than require travel insurance. InsureMyTrip.com has a page devoted to countries that require travel insurance.

It bears thinking about what it would take to get home for treatment should you contract Covid-19 abroad. Thailand, for example, requires travelers to have medical insurance with the minimum coverage of $50,000. “Evacuation out of Thailand would be higher,” said Sasha Gainullin, the chief executive of Battleface , a travel insurance start-up that unbundles benefits. In the case of a Thailand trip, he advised taking medical coverage up to $100,000 for treatment locally and $500,000 for medical evacuation and repatriation.

Do I need insurance if I have bookings with flexible cancellation policies?

Probably not, if you have hotel reservations that allow free cancellation 24 to 48 hours in advance. The same with flights; if your flight is changeable and will provide a voucher or refund in case of cancellation, you’re covered.

I have rented a house with restrictive cancellation penalties. Can I insure against those?

Yes. Vacation home rentals from Airbnb and the like can be treated just like other accommodations that do not offer refunds. In this case, you would want to get a policy in the amount you would forfeit if you had to cancel for a covered reason like illness. Again, fear of travel is not a covered reason; for that, you would need C.F.A.R.

Elaine Glusac is the Frugal Traveler columnist. Follow her on Instagram: @eglusac .

Follow New York Times Travel on Instagram , Twitter and Facebook . And sign up for our weekly Travel Dispatch newsletter to receive expert tips on traveling smarter and inspiration for your next vacation.

An earlier version of this article misstated the timeframe within which it is recommended that Cancel for Any Reason travel insurance be purchased. It is generally within about two to three weeks of booking the trip, not one or two days.

How we handle corrections

June 1, 2020

Due to travel restrictions, plans are only available with travel dates on or after

Due to travel restrictions, plans are only available with effective start dates on or after

Ukraine; Belarus; Moldova, Republic of; North Korea, Democratic People's Rep; Russia; Israel

This is a test environment. Please proceed to AllianzTravelInsurance.com and remove all bookmarks or references to this site.

Use this tool to calculate all purchases like ski-lift passes, show tickets, or even rental equipment.

Travel Insurance and COVID-19: The Epidemic Coverage Endorsement Explained

Get a Quote

{{travelBanText}} {{travelBanDateFormatted}}.

{{annualTravelBanText}} {{travelBanDateFormatted}}.

Type the country where you will be spending the most amount of time.

Age of Traveler

Ages: {{quote.travelers_ages}}

If you were referred by a travel agent, enter the ACCAM number provided by your agent.

If you're not completely satisfied, you have 15 days (or more, depending on your state of residence) to request a refund - provided you haven't started your trip or initiated a claim. Plans are non-refundable after this period .

Free Review Period

Travel Dates