Language selection

- Français fr

Automobile allowance rates

The automobile allowance rates for 2024 are:

- 70¢ per kilometre for the first 5,000 kilometres driven

- 64¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2023 are:

- 68¢ per kilometre for the first 5,000 kilometres driven

- 62¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2022 are:

- 61¢ per kilometre for the first 5,000 kilometres driven

- 55¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2021 were:

- 59¢ per kilometre for the first 5,000 kilometres driven

- 53¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2020 were:

The automobile allowance rates for 2019 were:

- 58¢ per kilometre for the first 5,000 kilometres driven

- 52¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2018 were:

- 55¢ per kilometre for the first 5,000 kilometres driven

- 49¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2016 and 2017 were:

- 54¢ per kilometre for the first 5,000 kilometres driven

- 48¢ per kilometre driven after that< In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel.

The automobile allowance rates for 2015 were:

Page details

TRAVEL ALLOWANCES

We look at how travel allowances work, which method of calculation is best, and also provide a heads-up of how to manage the unforeseen consequences of the COVID-19 pandemic.

FEATURED IN

COVID-19 has far-reaching effects for the South African taxpayer and, unbeknown to many, may be silently increasing their tax liability for the 2022 year of assessment. In some cases, the purpose for granting a travel allowance to employees (and the same applies to company vehicles) has been subverted by the pandemic, where business travel may no longer be required or possible. In this article we revisit the general taxing principles of a travel allowance, and the reimbursement of travel expenses claims. We also as consider how COVID-19 may increase the tax burden of an employee in this context.

The general taxing principles of a travel allowance and a reimbursive travel allowance

The SARS Guide for Employers in Respect of Allowances (2022 Tax Year) defines a travel allowance as “any allowance paid or advance given to an employee in respect of travelling expenses for business purposes.”

Fundamentally, the legislative framework makes provision for two scenarios –

- A travel allowance given to an employee to finance transport, which in the ordinary course would be a set rate or amount per pay period (“travel allowance”).

- A reimbursement given to an employee based on actual business travel (“reimbursement”).

The travel allowance “deduction” operates on the premise that an allowance is included in a person’s taxable income (see section 8(1)(a)(i) of the Income Tax Act No. 58 of 1962 (“the Income Tax Act”)), to the extent that the allowance has not actually been expended on business travel (see section 8(1)(a)(i)(aa)). The general position is private travel is taxable and business travel is not taxable.

Travel allowance

Where the employee is granted a travel allowance, paragraph (cA) of the definition of “remuneration” under the Fourth Schedule to the Income Tax Act provides for two inclusion rates for purposes of deducting employees’ tax (PAYE), namely 80% or 20%.

The standard withholding rate is 80%, unless the employer is satisfied that at least 80% of the use of the motor vehicle in question will be for business purposes, in which case the inclusion rate is only 20%.

In certain cases, employers are cognisant that the employee will not expend their travel allowance on business travel to any degree, which prompts a 100% withholding rate. It is important to note, however, that since the release of the 2019 SARS BRS Change – Patch Phase 3, the 100% inclusion rate is no longer applicable and should therefore not be implemented on payroll.

This position aligns with the purpose of a travel allowance, which is to defray costs of business travel. Technically, where it is known at the outset that the employee will not use the allowances for business travel expenses, the amount is not a “travel allowance” as envisaged by section 8(1)(a)(i)(aa), read with the definition of “remuneration”.

Reimbursive travel allowance

An alternative to providing an employee with a monthly travel allowance amount is to provide the employee with a reimbursive travel allowance. A reimbursive travel allowance is an allowance paid to an employee for actual business kilometres travelled, according to either the SARS determined rate – which is R 3.82 per kilometre from 1 March 2021 (down 4% from R3.98) – or as determined by the employer.

The taxing of the reimbursive allowance has fundamentally changed from 1 March 2018. Where an employee is reimbursed using a rate higher than the SARS prescribed rate, the differential between the SARS prescribed rate and the rate utilised by the employer will be subject to employees’ tax (PAYE), regardless of the number of business-related kilometres travelled.

It is advisable that employers prudently consider their reimbursement rates against the prescribed rate. An unintended consequence of reimbursing an employee on a higher rate will increase the employee’s PAYE liability and may result in lower employee take-home pay. An alternative to avoid this possible occurrence would be for the employer to reimburse the employee at a rate below the prescribed rate of R 3.82 per kilometre. The reimbursement will not attract PAYE and will also not be taxable on the employee’s personal tax return.

In our practice we have a golden rule when it comes to employee travel debates, i.e. company car vs. travel allowance vs. reimbursive structure: an apples-with-apples computation must always be done. Each employee’s factual matrix will be different, and one can only determine the most optimal outcome once calculations for every scenario has been done.

Although the reimbursive changes have not altered an employee’s ability to claim against a travel allowance, they have introduced an additional record-keeping requirement. This especially becomes complex where travel reimbursive rates have changed during the tax year.

The Commissioner for SARS is alive to the fact that most employees’ circumstances have changes as a result of the pandemic, where business travel would generally have decreased to great extent. Building on their 2020 tax season approach, SARS will most likely enhance their robust stance on verifications and audits of tax returns. It is now, more than ever, particularly important to maintain an accurate and detailed travel logbook and to adopt good tax filing and compliance strategies.

Must I own the vehicle or motorcycle?

In certain circumstances, employees who receive travel allowances can find themselves travelling with a vehicle that is not self-owned, for example a relative’s motor vehicle. Will this disqualify the employee from claiming against the travel allowance? No, it is not imperative that the car in question should be owned by the employee. Section 8 of the Income Tax Act does not limit or disallow the claim against the travel allowance in this instance. Obviously, this can lead to an enquiry by the SARS auditor, possibly to check that there is only one person claiming against the same vehicle.

Travel allowance with the right of use of motor vehicle

Where an employee receives a travel allowance and has made use of a company-provided car, a tax claim against the travel allowance (in terms of travel for business purposes) will not be allowed (see section 8(1)(a)(i)(aa)).

This will raise a concern with the employee, as the use of a company motor vehicle is considered a taxable fringe benefit, according to paragraph 7(2)(b)) of the Seventh Schedule to the Income Tax Act. Taxes on the fringe benefit may also be withheld at either 80% or 20% of the benefit. Does this mean that even where the employee travels for business, he or she may not claim against taxes on the travel allowance and the company car fringe benefit? No, there is a way out.

Tax deduction against a right of use of motor vehicle

Although a deduction against a travel allowance is not possible under section 8, a reduction of the fringe benefit constituted by the use of an employer-provided vehicle can still be claimed. Like section 8(1)(a)(i), the claim against a fringe benefit under paragraph 7(2)(b)) of the Seventh Schedule has been worded similarly. The reduction of the fringe benefit operates on the premise that the fringe benefit should be excluded from a person’s taxable income to the extent that it is expended on business travel.

In other words, the fringe benefit can be reduced to the extent that the benefit has been actually expended on travelling on business, and not on private travel. To reiterate: private travel is taxable and business travel is not taxable. Similarly, the COVID-19 restrictions will have a direct impact on the business claim lodged against the fringe benefit. This may very well create an employee’s tax exposure for those employers who apply the 20% rule or otherwise will cause an unwelcome surprise in relation to the employee’s tax liability.

How does one prove or illustrate that travel was for business v private?

Section 8(1)(b)(iii) provides that “ where such allowance or advance is based on the actual distance travelled by the recipient in using a motor vehicle on business … or such actual distance is proved to the satisfaction of the Commissioner to have been travelled by the recipient … the amount expended by the recipient on such business travelling shall … be deemed to be an amount determined on such actual distance at the rate per kilometre fixed … in the Gazette for the category of vehicle used ”.

It is interesting to note that the word “logbook” is not specifically mentioned in the Act. Rather, reference is made to a travel allowance claim being allowed to a taxpayer that proves business distance travelled to the satisfaction of the Commissioner.

Nonetheless – and in practice – a taxpayer can discharge the onus of proof that travelling with a private vehicle was travel for business purposes through keeping a logbook and recording the necessary information related to business travel (see SARS Interpretation Note 14, paragraph 5.4.2). SARS has provided an acceptable format.

According to the SARS eLogbook Guide for 2021/2022 on the acceptable format, the bare minimum information required to claim a tax deduction is the following:

- The date of business travel

- The business kilometres travelled

- The business travel details (where to and the reason for the trip)

It is not necessary to keep record of the details of private travel. This format and the requirement to record only business kilometres travelled have remained consistent since the 2018 year of assessment. This was not the case during the 2015, 2016 and 2017 years of assessments, as per the respective 2015, 2016 and 2017 SARS eLogbook Guides. Furthermore, the SARS eLogbook Guide for 2020/2021 and 2021/2022 continues the same chorus and requires record of business travel only – continuing to provide taxpayers with administrative relief.

Whilst the law does not specifically require a format in which the onus must be discharged, the SARS logbook format is generally recommended as the path of least resistance. Nonetheless, as long as the logbook can discharge the taxpayer’s onus of proof it will be acceptable.

What is defined as business travel?

The Income Tax Act does not define what is regarded as travel for business purposes, and what constitutes private use of a travel allowance. The “travel between home and work” exclusion has caused interpretation problems for as long as can be remembered. The law clearly determines that private travelling includes “travelling between … place of residence and … place of employment or business” (see section 8(1)(b)(i)). In alleviating any further uncertainty, SARS has published Interpretation Note 14, noting the examples below to distinguish between business and private travel. (These should only be used as a guideline. It must be noted that SARS is not bound by Interpretation Notes and may deviate from them.)

- Where an employee travels from the office to attend a conference.

- Travelling from home to a client and the travel after the meeting to the office.

- Travelling from a home office to a client’s premises.

- Travelling from home to another branch of your employer where you are not ordinarily working.

- Travel between the home and office.

- Travelling from a friend’s house to the office.

- Regularly travelling from home to different places of work on different days.

Could the current context of COVID-19 restrictions introduce an added interpretation problem on what constitutes business travel? Where an employee falling under the essential services category has travelled for business purposes during the lockdown periods, one would not anticipate any dilemma in claiming against a travel allowance. Considering that the restrictions announced by Government were legally binding, it will be interesting to see whether a claim for business kilometres travelled by a non-essential service employee, during the same period, will also be considered as valid business kilometres. This may only find application in the periods where the country operated under very strict lockdown restrictions but may very well become an added SARS audit requirement.

Calculating the claim

There are two methods of calculating the deductible amount against the travel allowance: the actual costs method and the deemed costs method. Each method has its own set of requirements.

1. The actual costs method

This method requires accurate information in the form of receipts, tax invoices and other relevant source documents. For the purpose of finance charges (section 8(1)(b)(iiiA)(bb)(B)) and wear-and-tear expenses (section 8(1)(b)(iiiA)(bb)(A)) the maximum vehicle value is R665 000.

The qualifying deduction is based on computing actual expenditure per kilometre and multiplying it with the business kilometres. To illustrate this, let us consider the below example:

Mr X owns a vehicle valued at R280 000 and incurred the following expenses:

Mr X travelled a total of 32 000 km, of which 8 000 km were for business purposes, as evidenced by his logbook. Mr X received a total travel allowance of R48 000 for the 2020 year of assessment. As a result, Mr X would be able to claim R21 637,50 (8 000 km ÷ 32 000 km x R86 550) as a deduction against his travel allowance.

2. The deemed costs method

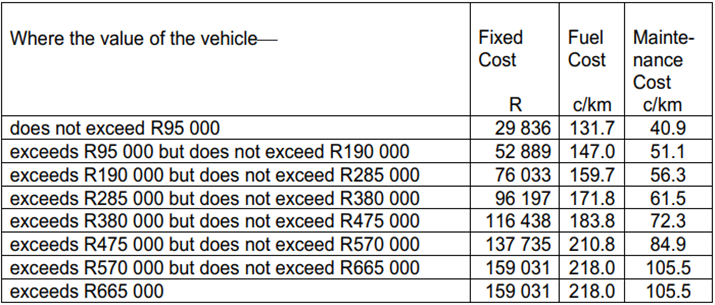

The deemed costs method comprises three components: the fixed costs, the fuel costs and the maintenance costs. SARS provides a table from which the taxpayer determines the appropriate deemed cost elements based on the vehicle value. The table can be found on SARS’ website and is revised annually, per notice in the Gazette . Taxpayers who want to claim using this method must bear maintenance costs and fuel costs themselves.

Considering the information provided in the previous example, the fixed cost, fuel cost and maintenance cost components can be referenced as follows. Figures below are relevant for a vehicle fitting into the R285 000 to R380 000 cost bracket.

In using this method, Mr X would be able to claim R39 224 (8 000 km x R4.903 per km) as a deduction against his travel allowance.

In our experience, the deemed costs method requires less administration and is almost always more favourable than the actual costs method. It is critical to note that the fuel and maintenance components can only be factored in where the employee has borne the full costs of fuel and maintenance. Where these are reimbursed to any degree, the relevant component cannot be factored in to calculate the cost per kilometre.

COVID-19 and travel allowances

The travel allowance will become a contentious item where employees are receiving a travel allowance for business travel and such business travel is not possible, or required as a result of the pandemic. In the initial stages of the pandemic, travelling was prohibited to a large extent. Since then, the restrictions have eased significantly, but this does not mean that the situation has changed. Company culture and practices have changed considerably, where employees are still precluded from working at the office or are given the option to work at home. The result is that meetings are held virtually and the need to travel to clients have diminished. The upshot is that business travel is, for the most part, no longer required. This reality was reflected in the 2021 Budget Review, where government noted that the efficacy of travel allowances will be reviewed:

“Reviewing tax provisions for travel and working from home In light of the large-scale migration to working at home over the past year, the National Treasury will review current travel and home office allowances to investigate their efficacy, equity in application, simplicity of use, certainty for taxpayers and compatibility with environmental objectives. In recognition of the potential effect on salary structuring, this will be a multi-year project, starting with consultations during 2021/22.”

Consequently, employees will be required to take extra care in preparing their logbooks and employers must consult with their employees on how their allowances should be structured and taxed.

In determining the taxing rate of the travel allowance – that is whether taxes should be withheld at a rate of 80% or 20% of the travel allowance – the employer and employee would have adopted a rate based on the actual travel performed in previous years, and on which much anticipation has been placed for the 2022 year of assessment. Regardless of the rate adopted by the employer, the sudden impact of COVID-19 and the limitations placed on the employee’s business travel may translate into a 2022 tax liability for the employee on submission of the related return.

Employers that have resolved to taxing 20% of a travel allowance paid to an employee who is not an essential services employee, or one that will no longer travel as normal, should perhaps consider adopting the 80% rate. This will likely assist the employee to “prepay” the pending tax liability resulting from an expected reduced travel allowance claim.

In case of a reimbursive travel allowance, the above dilemma appears to be conveniently avoided, even where a tax liability arises. A reimbursive allowance is paid to an employee at a rate multiplied by business kilometres travelled. This thus creates a relationship between the allowance and the business kilometres travelled. Employees will find that the risk of a deferred 2022 tax liability is eliminated, as their business travel claim will be directly aimed at the reimbursive allowance. The importance of a well-maintained travel logbook, for such employees, must be emphasised.

It is best practice that the employer’s resolution to tax more of the allowance be performed on a case-by-case basis and based on the factual circumstances of the employee, as opposed to a blanket approach. The change in withholding taxes will reduce take-home pay and will be felt immediately in the employee’s pocket, although preventing a cash flow burden in the long run.

Travel allowance deduction: The independent contractor perspective

What is the difference between employees’ and independent contractors’ deductions?

Due to the nature of the contract between an independent contractor and a client, the provision of a travel allowance would be unusual. An independent contractor would usually recover business travel costs incurred by invoicing or charging a disbursement fee.

An independent contractor, as explained in Interpretation Note 17, is an individual or person similar to an entrepreneur – someone clearly distinguishable as an “employer” and not an “employee”.

Implications of travel costs deduction

Section 8 does not cater for an independent contractor. Consequently, an independent contractor can rely on section 11(a) to obtain a deduction for travel costs – as well as section 11(e), in terms of claiming a capital allowance on the wear-and-tear incurred on his or her vehicle. The burden of proof is placed on the independent contractor (section 102 of the Tax Administration Act). This means relevant source documents, including a logbook, would need to be provided. The position may be summarised as follows:

- The independent contractor does not need a travel allowance or reimbursement to claim, and any amounts received by the independent contractor for business travel will form part of their gross income.

- The tax deduction is effectively claimed in the same way as an employee would claim against a travel allowance, by using the actual costs method, with a logbook indicating the portion of business travel.

Further to the above, the R665 000 limit for wear-and-tear and finance costs per section 8(1)(b)(iiiA)(bb)(A) and (B) is not applicable to an independent contractor. As mentioned above, the vehicle wear-and-tear expense is claimed separately as a capital allowance under section 11(e).

Example (based on the details provided above):

Mr X owns a vehicle valued at R280 000 that he bought on 1 March 2018. He incurred the following expenses:

Wear-and-tear expenses (claimed under section 11(e) – see below)

Mr X travelled a total of 32 000 km, of which 8 000 km were for business purposes, as evidenced by his logbook. As a result, Mr X would be able to claim R11 637.50 (8 000 km ÷ 32 000 km x R46 550) as a business travel expense against his gross income. In addition, Mr X would be able to claim a R14 000 wear-and-tear capital allowance – according to section 11(e), read together with Interpretation Note 47.

The wear-and-tear capital allowance is calculated as follows:

(R280 000 ÷ 5 × (12 months ÷ 12 months)) × (8 000 km ÷ 32 000 km) = R14 000

It is important to note that in this instance – as per section 11(e), and read with Interpretation Note 47 – an independent contractor who seeks to claim this capital allowance needs to be the owner of the vehicle or should have borne the cost of purchasing the vehicle. Contrary to section 8, the ownership of the vehicle is one of the important factors that need to be adhered to, in order to claim the section 11(e) capital allowance.

Key take aways

- Maintaining an accurate logbook remains imperative. For verifications and audits on the 2020 tax returns, it appears that SARS will look to build on the stance adopted during 2020, and scrutinise the information included on a travel logbook. A taxpayer must retain a logbook for at least five years, and SARS reserves the right to audit and query the content and information recorded in it. Where documents are not kept for five years, it is a criminal offence.

- Considering that the COVID-19 travel restrictions announced by Government are legally binding, it might be expected for an essential services employee to further support their essential service designation to SARS, in addition to providing a logbook.

- An employee might be facing a tax liability on assessment, where the employee is receiving a travel allowance or company vehicle for business travel and such business travel is not possible or no longer required.

- Similarly, in light of the restrictions and changes brought on by the pandemic, a reimbursive travel allowance might be viewed as a more apt option and suited to the circumstances. Even where an employer withholds taxes on the reimbursive allowance, an employee will be able to align their business travels to the reimbursive allowance and will find themselves more efficient come the 2022 tax submission.

- Where an employer is withholding taxes on 20% of the travel allowance paid to an employee whose business travel will be substantially limited due to the pandemic, the employer should consider adjusting their tax withholding strategy to align to the circumstances, where possible. It should be noted that generally SARS will legally come after the employer (and so they should for collection efficiency) where the 20% withholding is incorrectly applied. In saying that, failure by the employer to withhold the correct employees’ tax does not absolve the employee from a tax liability.

Share to your social feed

- Share on Facebook

- Share on Twitter

- Share on LinkedIn

- Full Name *

- Email Address *

- Contact Number *

- Subject * Select a service (required) Tax Legal Assistance Tax Return Expatriate Tax Remuneration Structuring Accounting Local & Global Work Permits Company Setup & CIPC Foreign Exchange Solutions Law Firm Collaboration Other

- I need assistance with (Tax Legal) * I need assistance with (required) Voluntary Disclosure Programme Remission of Tax Penalties Tax Dispute Resolution Commercial Agreements Cross Border Taxation VAT Disputes/Refunds Trusts SARS Audit Other

- I need assistance with (Accounting) * I need assistance with (required) Monthly Accounting Annual Financial Statements Company Reg. & Tax Advice VAT Reg. & Returns Payroll Services Deceased Estates Tax Administration Independent Audit Independent Review Other

- I need assistance with (Remuneration) * I need assistance with (required) Package Structuring Tool with Flexible Benefits (Only From Employer Perspective, Not Individual) Expatriate Payroll Service Tax & Cost to Company Training Payroll Review/Audit Job Evaluation & Design Cost-To-Conversion Payscale Design Other

- I need assistance with (Expat Tax) * I need assistance with (required) Double Taxation Agreement Tax Returns Financial Emigration Tax Planning & Advice Other

- I need assistance with (Local & Global Work Permits) * I need assistance with (required) Expatriate Tracking System Immigration Audit Business Visa Permanent Residency Undesirable Status Africa Visas Expatriate Tax Planning Police Clearance Certificate Other Visas and/or Permits

- How many years have you been outside of South Africa? (required) *

- Is It Your Permanent Intention To Remain Abroad? * Is It Your Permanent Intention To Remain Abroad? (required) Yes No Not Sure

- Category of Taxpayer * Category of Taxpayer (required) I am South African citizen working in South Africa I am foreign national working in South Africa I am a South African living and working abroad

- Do you have any forms of income besides your employment income? * Do you have any forms of income besides your employment income? (required) Yes No

- Did you receive other worldwide income? * Did you receive other worldwide income? (required) Yes No

- How many years have you been outside of South Africa? *

- Is it your permanent intention to remain abroad? * Is it your permanent intention to remain abroad? (required) Yes No Not Sure

- Travel Allowance

- Retirement Annuity

- Medical Aid

- Do you have access to your own efiling profile? * Do you have access to your own efiling profile? (required) Yes No

- Where did you hear about us? * Where did you hear about us? (required) Facebook Google Search (Search Engine) Google Advert LinkedIn Tax Talk Newsletter Event and/or Conference Recommendation/Referral from Colleague or Third Party Twitter Other None of the Above

- Phone This field is for validation purposes and should be left unchanged.

This Website Uses Cookies

Privacy overview.

- 084 969 0510

- [email protected]

- Our Accounting Services

- Our Tax Services

- Company Secretarial Services and Compliance Services, CIPC Services

- Promotion of access

- Security Policy

South African Tax Guide

Taxation Made Easy by Nyasha Musviba

FAQ – How are travel expenses for which I was reimbursed treated for PAYE purposes?

What is a travel allowance, fixed travel allowance, employees’ tax treatment, income tax assessment treatment.

You are using an outdated browser. Please upgrade your browser to improve your experience.

[FAQ] What is the correct tax treatment of employee travel allowances?

Login to my account, quick registration.

- (1) Negotiating Tax Debt and Payment Arrangements with SARS

- (14) Accounting

- (2) Accounting for Income Tax

- (7) Administration of Estates

- (1) Application of tax rates, s6(2) rebates

- (1) Assessed losses

- (4) Audit, Reviews & Other Services

- (8) Capital Gains Tax

- (1) Capital Gains Tax - Individuals Tax

- (1) Capital Gains Tax Implications of Trusts

- (2) Case study: Home office expense

- (1) Case study: Travel allowances

- (1) Company Formations

- (117) Corporate Tax

- (9) Customs and Excise

- (2) Deceased Estate

- (1) Deductions Pre-trade and prepaid expenses

- (1) Deferred tax assets and deferred tax on equity

- (1) Deregistration

- (2) Employer and Employee (PAYE and UIF Specific)

- (1) Estate Duty

- (5) Faculty News

- (2) Farming

- (142) Individuals Tax

- (1) Input - Customs Duty

- (3) Interest

- (13) International Tax

- (17) Legislation

- (1) Low interest rate loans and loan subsidies

- (1) Nature of the rights of beneficiaries

- (1) Notional input tax

- (8) Payroll

- (2) Practical Payroll

- (2) Provisional tax (Link with other Taxes)

- (1) SARS Dispute Resolution

- (4) SARS Issues

- (1) Salaried Employees

- (126) Tax Administration

- (2) Tax Administration Part 2B: Resolving Problems with SARS using the Tax Ombud

- (1) Tax Administration Part 3B Dispute Resolution - Objection and appeal

- (2) Tax Update

- (2) Tax implications of loans to trusts

- (1) Tax residence

- (1) Tax returns and payments

- (1) Transfer-Pricing

- (1) Trust Income / Gain Allocations

- (1) Trust types and income allocations

- (3) VAT periods

- (1) Wear and tear allowances

- (1) Zero Rated

- Recent Comments

- 28 August 2023

- Case study: Travel allowances

- The Tax Faculty Tax Specialist

This article is based on tax law for the year ending 29 February 2024.

In the 2021 tax year, my client received a non-taxable reimbursed travel allowance under code 3703, resulting in a nice refund. However, for the 2022 tax year, the payroll person changed the code to 3702, making it a taxable allowance, which has impacted the client negatively. Can a company change these codes without informing the recipient, giving them a chance to adjust and avoid owing money to SARS? Furthermore, the allowance for 2022 was unusually high at R 459,000.00 over six months, with a monthly amount of 3 times my client's basic salary of R 3601. I am concerned about my client's situation as they were not made aware of the code change and are now facing a significant amount owed to SARS. Is there any recourse available in this situation?

In the tax context, two specific codes are used to determine the nature of reimbursed travel allowances: code 3703 signifies a non-taxable reimbursed travel allowance, while code 3702 denotes a taxable reimbursed travel allowance. Allow me to elaborate on their distinctions:

- Code 3703 - Reimbursable Travel Allowance (Non-taxable):

This code is applicable when the allowance or advance is calculated based on the actual distance travelled for business purposes, excluding personal use. This code is used when the actual business kilometres travelled remain below 12,000 kilometres and the prescribed rate per kilometre is R4.64. It is important to note that no other forms of compensation are provided to the employee in this context.

- Code 3702 - Reimbursable Travel Allowance (Taxable):

Code 3702 comes into play when the employer's reimbursement rate surpasses the prescribed rate of R4.64, the business kilometres travelled exceed 12,000 kilometres, or the employee receives additional compensation for travel. This code is relevant only for the portion of the reimbursement that exceeds the amount calculated by multiplying the prescribed rate by the actual business kilometres travelled.

The company will select the appropriate code based on the conditions mentioned above for the reimbursed travel allowance. In your mentioned case, the value of R459,000.00 triggers an evaluation of the business kilometres travelled.

For the year 2021, where the prescribed rate was R3.82, it can be deduced that approximately 120,157 kilometres were travelled during that tax year. Considering the application of code 3703, the maximum kilometres must remain at 12,000, and the reimbursement must not exceed R45,840.00.

In 2022, code 3702 was used as the criteria for code 3703 were apparently no longer met. The value of R459,000.00 suggests either an exceptionally high distance travelled or an elevated rate per kilometre.

Payroll utilizes the following codes:

- Code 3702 = R amount (R4.64 x total business kilometres travelled) (not subject to employees’ tax)

- Code 3722 = R amount (Excess over prescribed rate x 1000 km) (subject to employees’ tax)

Please note that this explanation reflects the applicable codes and calculations for reimbursed travel allowances. If you require further assistance or clarification, feel free to ask.

Join Carmen Westermeyer for our September TaxCafé Discussion Forum, where she will focus on resolving current tax issues experienced in practice.

- Click here to intro snippet.

- Click here to for more information

LEAVE A COMMENT

Need help .

We couldn't found any email record. Please create new account Create an account

Ask a Technical Question is available to subscribers. Click here to find out more

STAY IN TOUCH

Subscribe to our mailing list and you will receive our best posts every week on our live CPD webinars , upcoming courses and webinars-on-demand

By subscribing to our mailing list you accept our Terms of Service and Privacy Policy

Verify Cell Number

Explore smarty.

- New 2 COLUMNS

FIXING OF RATE PER KILOMETRE IN RESPECT OF MOTOR VEHICLES FOR THE PURPOSES OF SECTION 8(1)(b)(ii) AND (iii) OF THE INCOME TAX ACT, 1962

Prescribed rate per kilometre:

The prescribed rate per kilometre used for reimbursive travel allowance for 2022/2023 has increased from R3.82 to R4.18

Vehicle lookup table for the purpose of calculating a travel allowance (deemed cost rate per kilometre on assessment):

Click here to read the Gazette: Government Gazette 46015

- Associate Login

- Rain Analytics Dashboard

- NowHR PSIber Demo Login

- Newsflashes Archive

The Prescribed Travel Rate per KM increases and the Determined Travel Allowance Rate Table is Updated

The updated information and rates relating to the Prescribed Travel Rate per KM and the latest Determined Travel Allowance Rate Table has been outstanding since the 2022 Budget Speech.

Recently, Finance Minister Enoch Godongwana signed off on the latest rates and they are as follows:

Prescribed Travel Rate per KM

The prescribed travel rate per KM has been increased to R4.18 per KM , up from the previous R3.82 per KM. This rate is effective from 1 March 2022.

Determined Rate for Travel Allowance Table

The latest determined travel rate table is as follows and is effective from 1 March 2022.

About NowHR Author

Related posts.

POSTPONEMENT OF THE SARS VISION 2024 PROJECT

POSTPONEMENT OF THE EFFECTIVE DATE OF THE TWO-POT RETIREMENT SYSTEM

We have made a demo login of PSIber Payroll available to allow you to explore the functionality.

Use the following demo credentials to sign in:

- Username: [email protected]

- Password: Demo123@ (case-sensitive)

Click here to access the NowHR PSIber Demo Login Page

CRS News Flash 3 March 2020 – SOUTH AFRICA – CRS Tax Pocket Guide 2020/2021 Tax Year

MARCH 2020 – SOUTH AFRICA

CRS TAX POCKET GUIDE 2020/2021

It is important that employers note the following:

Tax rates from 1 March 2020 to 28 February 2021

- 80% of the travelling allowance must be included in the employee’s remuneration for the purposes of calculating PAYE (pay as you earn).

- The percentage is reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes.

- No fuel cost may be claimed if the employee has not borne the full cost of fuel used in the vehicle, and no maintenance cost may be claimed if the employee has not borne the full cost of maintaining the vehicle (e.g. if the vehicle is covered by a maintenance plan).

- The fixed cost must be reduced on a pro-rata basis if the vehicle is used for business purposes for less than a full year.

The actual distance travelled during a tax year and the distance travelled for business purposes substantiated by a logbook are used to determine the costs which may be claimed against a travelling allowance.

- AA rate per kilometre

Where the reimbursed rate exceeds the prescribed rate of R3.98 (previously R3.61) cents per kilometre, irrespective of the business kilometres travelled, there is an inclusion in remuneration for PAYE purposes. The full inclusion amount is subject to PAYE, unlike the fixed travel allowance where only 80% of the amount is subject to PAYE.

However, this alternative is not available if other compensation in the form of an allowance or reimbursement (other than for parking or toll fees) is received from the employer in respect of the vehicle.

Retirement fund lump sum benefits consist of lump sums from a pension, pension preservation, provident, provident preservation or retirement annuity fund on death, retirement or termination of employment due on attaining the age of 55 years, sickness, accident, injury, incapacity, redundancy or termination of the employer’s trade.

Severance benefits consist of lump sums from or by arrangement with an employer due to relinquishment, termination, loss, repudiation, cancellation or variation of a person’s office or employment.

- Retirement fund contributions

Amounts contributed to pension, provident and retirement annuity funds during a year of assessment are deductible by members of those funds.

Amounts contributed by employers and taxed as fringe benefits are treated as contributions by the individual employees.

The deduction is limited to 27.5% of the greater of the amount of remuneration for PAYE purposes or taxable income (both excluding retirement fund lump sums and severance benefits).

The deduction is further limited to the lower of R350 000 or 27.5% of taxable income before the inclusion of a taxable capital gain. Any contributions exceeding the limitations are carried forward to the immediately following year of assessment and are deemed to be contributed in that following year.

The amounts carried forward are reduced by contributions set off against retirement fund lump sums and retirement annuities.

Example: If an employee is reimbursed for 17 891 business kilometres travelled at R4.20 cents per kilometre and the prescribed rate is R3.98 cents per kilometre, the amount that will be included in remuneration for purposes of calculating the PAYE is calculated as (R4.20 cents – R3.98 cents) x 17 891. Based on this calculation an amount of R3 936 will be included in remuneration when PAYE is calculated. PAYE will therefore be withheld, on a payment basis, on the amount exceeding the prescribed rate of R3.98 cents per kilometre, irrespective of the total amount of business kilometres travelled.

Employer-owned vehicles

The taxable value is 3.5% of the determined value (the cash cost including VAT) per month of each vehicle.

Where the vehicle is:

- The subject of a maintenance plan when the employer acquired the vehicle the taxable value is 3.25% of the determined value; or

- Acquired by the employer under an operating lease the taxable value is the cost incurred by the employer under the operating lease plus the cost of fuel.

- 80% of the fringe benefit must be included in the employee’s remuneration for the purposes of calculating PAYE. The percentage is reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes.

- On assessment the fringe benefit for the tax year is reduced by the ratio of the distance travelled for business purposes substantiated by a logbook divided by the actual distance travelled during the tax year.

- A further relief is available on assessment for the cost of licence, insurance, maintenance and fuel for private travel if the full cost thereof has been borne by the employee and if the distance travelled for private purposes is substantiated by a logbook.

Deductions in respect of donations to certain public benefit organisations are limited to 10% of taxable income (excluding retirement fund lump sums and severance benefits). The amount of donations exceeding 10% of the taxable income is treated as a donation to qualifying public benefit organisations in the following tax year.

Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax at a rate of 20% are withheld by the entities paying the dividends to the individuals.

Foreign dividends

Most foreign dividends received by individuals from foreign companies (shareholding of less than 10% in the foreign company) are taxable at a maximum effective rate of 20%. No deductions are allowed for expenditure to produce foreign dividends.

Interest-free or low-interest loans

The difference between interest charged at the official rate (currently 7.25% p.a.) and the actual amount of interest charged is to be included in gross income.

Interest exemptions

Interest from a South African source earned by any natural person under 65 years of age, up to R23 800 p.a., and persons 65 and older, up to R34 500 p.a., is exempt from income tax.

Interest earned by non-residents who are physically absent from South Africa for at least 181 days during the 12-month period before the interest accrues and the debt from which the interest arises is not effectively connected to a fixed place of business in South Africa, is exempt from income tax.

Skills development levy

A skills development levy (SDL) is payable by employers at a rate of 1% of the total remuneration paid to employees. Employers paying annual remuneration of less than R500 000 are exempt from the payment of skills development levies.

Unemployment insurance contributions

Unemployment insurance contributions are payable monthly by employers, on the basis of a contribution of 1% by employers and 1% by employees, based on the employee’s remuneration below a certain amount.

Employers not registered for PAYE or SDL must pay the contributions to the Unemployment Insurance Commissioner.

Contact our legislation team at [email protected] if you require any additional information. © 2020 C RS Technologies (Pty)Ltd. All Rights Reserved.

- medical tax

- Retirement fund

- Skills Development Levy

- South Africa

- Tax Pocket Guide

- Tax rebates

- travelling allowance

- Unemployment insurance

One comment

Pingback: How Much Fuel Can I Claim Self Employed Tax? – Almazrestaurant

Comments are closed.

Engage™ Europe, Middle East, Africa distributor.

Quick links

- Participate

- CRS HR Services

- CRS Tax Advisory

- CRS Payroll Bureau

- Engage™ Software

- Engage™ Europe

- Enstruct e-learning portal

- Testimonials

- Partner Portal

- Partner Application

- SCARF Philosophy

- Hipe Agreement

Inspired, Engaged and Rewarded Employees

2024/2025 Tax Guide

2024/2025 Tax Guide download

Download your copy of the CRS 2024/2025 Tax Guide

This will close in 0 seconds

We use cookies to ensure that we give you the best experience on our website.

New to Tax? Start Here

- Do I need to submit a tax return?

- Salaried tax payers

- Provisional tax

- Independent contractors

- Small business (sole proprietors)

Living or Working Overseas

- Foreign employment income

- Foreign trade income

- Other foreign income

Earning Extra Income

- Rental income

- Capital gains tax

- Tax on Investments - What you need to know

Claiming & Deductions

- What can I claim

- Wear & tear / depreciation

- Travel expenses

- Medical expenses

- Donations tax

SARS & eFiling

- How to register

- How to get my tax number

- How to make a payment via eFiling

- How to register for provisional tax

After You File

- Amending details

- Tracking your refund

Company (Pty) Tax

- Company tax guide

- Turnover tax explained

- Register a company for eFiling

Quicks Links

- Tax definitions

- Guides & tutorials

- Tax questions & answers

- Main tax help page

- Ask a tax question

- Tax & Retirement- What you need to know

Travel Deduction Tax Calculator for 2025

Compare actual costs and deemed costs for the maximum tax deduction.

You've logged your mileage, now how about getting a competitive car insurance quote?

We've partnered with Naked to help you get your car covered against theft, accidents and Mother Nature.

Instant, online cover without the call centre chit-chat.

IMAGES

VIDEO

COMMENTS

A reimbursive travel allowance is an allowance paid to an employee for actual business kilometres travelled, according to either the SARS determined rate - which is R 3.98 per kilometre from 1 March 2020 - or as determined by the employer. The taxing of the reimbursive allowance has fundamentally changed from 1 March 2018.

The rate per kilometre determined in terms of the cost scale below applies in respect of years of assessment commencing on or after 1 March 2018. Fixed cost element covers the cost for depreciation, loss of interest, licensing and insurance for the year. The fixed cost element must be divided by the total distance travelled in the vehicle ...

Rates per kilometer. 29 February 2024 - The Minister of Finance has approved the new table of rates per kilometre for motor vehicles in respect of the 2025 year of assessment, for purposes of Section 8 (1) of the Income Tax Act No. 58 of 1962. The Commissioner for SARS has determined the daily amount for expenditure in respect of meals and ...

The automobile allowance rates for 2020 were: 59¢ per kilometre for the first 5,000 kilometres driven; 53¢ per kilometre driven after that In the Northwest Territories, Yukon, and Nunavut, there is an additional 4¢ per kilometre allowed for travel. The automobile allowance rates for 2019 were: 58¢ per kilometre for the first 5,000 ...

Fixed Cost Table: 1 March 2019 - 29 February 2020 Rates per kilometre, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined by using the following table: Value of the vehicle (including VAT) (R) Fixed cost (R p.a.) Fuel cost (c/km)

A reimbursive travel allowance is an allowance paid to an employee for actual business kilometres travelled, according to either the SARS determined rate - which is R 3.98 per kilometre from 1 ...

Reimbursive travel allowance. 30 April 2020; The Tax Faculty; Important: This article is based on tax law effective from 1 March 2020.. Where an allowance or advance is based on the actual distance travelled by the employee for business purposes, employees' tax will not be withheld on the allowance paid by an employer to an employee if the rate does not exceed 398 (previously 361) cents per ...

Mr X travelled a total of 32 000 km, of which 8 000 km were for business purposes, as evidenced by his logbook. Mr X received a total travel allowance of R48 000 for the 2019 year of assessment. As a result, Mr X would be able to claim R21 637.50 (8 000 km ÷ 32 000 km x R86 550) as a deduction against his travel allowance. 2.

A reimbursive travel allowance is an allowance paid to an employee for actual business kilometres travelled, according to either the SARS determined rate - which is R 3.82 per kilometre from 1 March 2021 (down 4% from R3.98) - or as determined by the employer.

A reimbursive travel allowance can be seen as an allowance or advance which is based on the actual distance travelled for business purposes (excluding private use). These amounts are normally paid by an employer to an employee by multiplying the actual business kilometres travelled by a rate per kilometre.

In 2022, code 3702 was used as the criteria for code 3703 were apparently no longer met. The value of R459,000.00 suggests either an exceptionally high distance travelled or an elevated rate per kilometre. Payroll utilizes the following codes: Code 3702 = R amount (R4.64 x total business kilometres travelled) (not subject to employees' tax)

As from 1 March 2018, PAYE must be withheld on any travel reimbursement calculated at a rate higher than the prescribed rate. Therefore, an employee will now pay tax upfront via the PAYE withholding process on reimbursive travel allowances, if they are reimbursed at a higher rate, rather than only paying tax on assessment of the ITR12.

- You received a travel allowance (source code 3701 or 3702 on your IRP5) or,-You have a company provided vehicle (source code 3802 or 3816 on your IRP5) or, - You are a commission earner, independent contractor or sole proprietor. 2. My employer reimbursed my travel expenses using the SARS prescribed rate per km.

Amount of Tax to be deducted. R 977. Annual tables. An employee under the age of 65 received a salary (retirement funding income) of R15 500 per month and contributes R300 per month to a pension fund as well as R800 per month to a registered medical scheme in respect of himself/herself and one dependant.

A reimbursive travel allowance is where an allowance or advance is based on the actual distance travelled for business purposes (that is excluding private use). The rate per kilometre is fixed by the Minister of Finance and currently is — • R4.84 per kilometre (from 1 March 2024). Pre 1 March 2018 (2018 and prior tax years) -

3.3 Reimbursement 14 3.4 Travel Allowance 14 3.4.1 Reimbursive Travel Allowance 15 3.4.2 Estimating a Travel Allowance for an Employee 16 3.4.3 Establishing the Rate per Kilometre of the Vehicle 16 3.4.4 Travel Allowance on Assessment 17 3.5 Subsistence Allowance 18 3.6 Reimbursements/advances for business travel on day trips 19

Reimbursement travel transactions captured in the 2024/2025 tax year, will be calculated on the 2023/2024 rate R4.64 until the new software is installed - to correct the transactions, they will need to be deleted and recaptured. The Tax and Travel calculator for 2024/2025 has also been updated with the new scale and rate.

The prescribed rate per kilometre used for reimbursive travel allowance for 2022/2023 has increased from R3.82 to R4.18. Vehicle lookup table for the purpose of calculating a travel allowance (deemed cost rate per kilometre on assessment): Click here to read the Gazette: Government Gazette 46015. PERSONEELNUUS REPORTABLE ARRANGEMENTS.

Prescribed Travel Rate per KM. The prescribed travel rate per KM has been increased to R4.18 per KM, up from the previous R3.82 per KM. This rate is effective from 1 March 2022. Determined Rate for Travel Allowance Table. The latest determined travel rate table is as follows and is effective from 1 March 2022.

on the SARS website www.sars.gov.za, under Legal Counsel / Secondary Legislation / Income Tax Notices / 2021. Travelling allowance Rates per kilometre, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined using

AA rate per kilometre. Where the reimbursed rate exceeds the prescribed rate of R3.98 (previously R3.61) cents per kilometre, irrespective of the business kilometres travelled, there is an inclusion in remuneration for PAYE purposes. The full inclusion amount is subject to PAYE, unlike the fixed travel allowance where only 80% of the amount is ...

I receive a Travel Allowance or Taxable Reimbursive Allowance (source code 3701 / 3702 is on my IRP5/IT3a). I am an Independent Contractor / Commission Earner (source code 3606 / 3616 is on my IRP5/IT3a). I run my own business / am a sole proprietor / freelancer. Tax year: Date you started using the car:

In other words, if the estimated business travel is R2 000 per month, the employee could be entitled to a maximum travel allowance of R10 000 per month. This approach may, however, be challenged by SARS. If a R10 000 allowance is granted and coded under 3701, the risk is that the employee could fictitiously claim, say, R5 000 as a deduction for ...