- Today's news

- Reviews and deals

- Climate change

- 2024 election

- Fall allergies

- Health news

- Mental health

- Sexual health

- Family health

- So mini ways

- Unapologetically

- Buying guides

Entertainment

- How to Watch

- My Portfolio

- Latest news

- Stock market

- Premium news

- Biden economy

- EV Deep Dive

- Stocks: Most Actives

- Stocks: Gainers

- Stocks: Losers

- Trending Tickers

- World Indices

- US Treasury Bonds

- Top Mutual Funds

- Highest Open Interest

- Highest Implied Volatility

- Stock Comparison

- Advanced Charts

- Currency Converter

- Basic Materials

- Communication Services

- Consumer Cyclical

- Consumer Defensive

- Financial Services

- Industrials

- Real Estate

- Mutual Funds

- Credit cards

- Balance transfer cards

- Cash-back cards

- Rewards cards

- Travel cards

- Personal loans

- Student loans

- Car insurance

- Morning Brief

- Market Domination

- Market Domination Overtime

- Opening Bid

- Stocks in Translation

- Lead This Way

- Good Buy or Goodbye?

- Fantasy football

- Pro Pick 'Em

- College Pick 'Em

- Fantasy baseball

- Fantasy hockey

- Fantasy basketball

- Download the app

- Daily fantasy

- Scores and schedules

- GameChannel

- World Baseball Classic

- Premier League

- CONCACAF League

- Champions League

- Motorsports

- Horse racing

- Newsletters

New on Yahoo

- Privacy Dashboard

Yahoo Finance

2024 state of the cruise industry report shows cruise tourism has surpassed historical levels, demonstrates its significant economic contribution and leadership in environmental sustainability and responsible tourism.

New Oceans of Opportunities publication highlights the global cruise workforce and the growth of careers in cruising.

WASHINGTON , April 9, 2024 /PRNewswire/ -- Today, Cruise Lines International Association (CLIA), the leading voice of the global cruise community, has released its annual State of the Cruise Industry report and a new publication, Oceans of Opportunities workforce skills report.

The annual state of the industry report includes the release of 2023 passenger volume, which reached 31.7 million— surpassing 2019 by 7%. The report also shows continued demand for cruise holidays, noting intent to cruise at 82%. The forecast for cruise capacity shows an increase of 10% from 2024 through 2028, as cruise lines make ongoing, concrete progress in pursuit of net- zero emissions by 2050.

"Cruise continues to be one of the fastest-growing and most resilient sectors of tourism— rebounding faster than international tourist arrivals—and a strong contributor to local and national economies. In 2022, cruise tourism cruise generated 90% of economic impact compared to 2019, despite passenger volumes that year at 70% of 2019 levels. Over the past 50 years, cruise tourism has demonstrated its leadership in managed tourism and is an industry that has plenty of room for continued responsible growth given cruise travel comprises just 2% of overall travel and tourism," said Kelly Craighead , president and CEO of CLIA. "The industry also continues to lead the way in environmental sustainability and destination stewardship, with cruise lines making advancements in technology, infrastructure and operations, and in green skills training for crew."

Highlights from CLIA's 2024 State of the Industry report include:

Cruise is Thriving:

Cruise tourism reached 107% of 2019 levels in 2023, with 31.7 million passengers sailing – almost two million more than 2019.

2024 is forecast to see 35.7 cruise passengers sailing.

Intent to cruise is 6% higher than 2019, with Millennials being the most enthusiastic cruise travelers of the future.

Global cruise capacity is forecast to grow from 677K lower berths in 2024 to 745K lower berths in 2028.

Each year, the fleet becomes more efficient, as cruise lines invest in propulsion technologies with conversion capabilities for future alternative fuels and utilize a range of technologies and innovations to advance their sustainability initiatives.

2022 Global Economic Impact . In 2022, cruise generated:

$138 billion to the global economy

1.2 million jobs – up 4% compared to 2019.

$43 billion in wages

63% of those who have taken a cruise say that they have returned to a destination that they first visited via cruise ship for a longer stay, extending the economic impact.

For 2023, the economic impact is forecast to be even greater given the 50% increase in the number of passengers sailing in 2023 compared to 2022.

Trends in Cruise:

The number of new-to-cruise is increasing – 27% of cruisers over the past two years are new-to-cruise, an increase of 12% over the past year.

Cruises are a top choice for multi-generational travel – with more than 30% of families traveling by cruise with at least two generations and 28% of cruise travelers traveling with three to five generations.

Expedition and exploration are the fastest-growing sectors of cruise tourism, with a 71% increase in passengers traveling on expedition itineraries from 2019 to 2023.

Accessible tour excursions are on the rise—with 45% of cruise passengers booking an accessible tour for their most recent cruise.

73% of cruise travelers say that travel advisors have a meaningful influence on their decision to cruise.

"Cruise is the best vacation value there is, with incredible guest experiences delivered by a talented and dedicated multinational workforce of nearly 300,000 seafarers. To highlight the tremendous employment opportunities that cruise tourism supports around the world, CLIA has published a new skills and workforce publication, Oceans of Opportunity . With at least 56 new ships coming online between 2024 and 2028, there are vast opportunities for careers in cruise, which boasts an impressive employee retention rate upwards of 80%," said Craighead.

Highlights from CLIA's Oceans of Opportunities workforce report include:

In 2024, cruise lines will employ a multinational workforce of nearly 300,000 seafarers representing more than 150 countries, as well as tens of thousands of employees on land.

94% of women seafarers work in the cruise industry.

Around 40% of senior leadership roles at cruise companies are held by women.

Among current and future workforce needs are green skills.

To view the full 2024 State of the Cruise Industry Outlook report, see here . To view the full Oceans of Opportunities publication, see here .

About the Cruise Lines International Association (CLIA)

CLIA is the world's largest cruise industry trade association, providing a unified voice for the industry as the leading authority of the global cruise community. On behalf of its members, affiliates and partners, the organization supports policies and practices that foster a secure, healthy, and sustainable cruise ship environment, promoting positive travel experiences for millions of travelers who cruise annually. This year, CLIA forecasts that annual the number of passengers will reach 34.7 million passengers. The CLIA community includes the world's most prestigious ocean, river, and specialty cruise lines; a widespread network of stakeholders, including ports and destinations, ship development, suppliers, and business services; and a highly trained and certified travel agent members that represent the largest network of travel professionals specializing in cruise travel. The organization's global headquarters are in Washington, DC , with regional offices located in North and South America , Europe , and Australasia.

For more information, please visit cruising.org or follow us on Facebook , Instagram, Twitter , and YouTube with our handle @CLIAGlobal—or on LinkedIn .

View original content to download multimedia: https://www.prnewswire.com/news-releases/2024-state-of-the-cruise-industry-report-shows-cruise-tourism-has-surpassed-historical-levels-demonstrates-its-significant-economic-contribution-and-leadership-in-environmental-sustainability-and-responsible-tourism-302111983.html

SOURCE CRUISE LINES INTERNATIONAL ASSOCIATION

- Share full article

Advertisement

Supported by

The Cruise Industry Stages a Comeback

After watching thousands of passengers get ill and more than a year of devastating financial losses, the global cruise industry is coming back to life. And it says it knows how to deal with the coronavirus.

By Ceylan Yeginsu and Niraj Chokshi

Nothing quite demonstrated the horrors of the coronavirus contagion in the early stages of the pandemic like the major outbreaks onboard cruise ships , when vacation selfies and videos abruptly turned into grim journals of endless days spent confined to cabins as the virus raged through the behemoth vessels, eventually infecting thousands of people, and killing more than 100.

Passengers on the Diamond Princess and Grand Princess, two of the worst-hit ships, were forced to quarantine inside their small staterooms — some without windows — as infections on board spiraled out of control. Every day anxiety and fear mounted as the captains of the ships announced new cases, which continued to spread rapidly through ventilation systems and among crew members, who slept in shared quarters and worked tirelessly throughout the day to deliver food to guests.

At the time, it was difficult to imagine how the ships, which carry millions of passengers around the world each year, would be able to sail safely again. Even after the vaccination rollout gained momentum in the United States in April, allowing most travel sectors to restart operations, cruise ships remained docked in ports, costing the industry billions of dollars in losses each month.

Together, Carnival , the world’s largest cruise company, and the two other biggest cruise operators, Royal Caribbean and Norwegian Cruise Line , lost nearly $900 million each month during the pandemic, according to Moody’s, the credit rating agency. The industry carried 80 percent fewer passengers last year compared to 2019, according to the Cruise Lines International Association, a trade group. Third-quarter revenues for Carnival showed a year-to-year decline of 99.5 percent — to $31 million in 2020, down from $6.5 billion in 2019.

And yet in June, Richard D. Fain, chairman and chief executive of Royal Caribbean Cruises, was beaming with excitement as he sat sipping his morning coffee onboard Celebrity Edge, which became the first major cruise ship to restart U.S. operations, with a sailing out of Fort Lauderdale, Fla. “At the beginning we didn’t have testing capabilities, treatments, vaccines or a real understanding of how the virus spread, so we were forced to shut down because we didn’t know how to prevent it,” he said.

Several epidemiologists questioned whether cruise ships, with their high capacities, close quarters and forced physical proximity, could restart during the pandemic, or whether they would be able to win back the trust of travelers traumatized from the initial outbreaks.

Now, said Mr. Fain, the opposite has proved true. “The ship environment is no longer a disadvantage, it’s an advantage because unlike anywhere else, we are able to control our environment, which eliminates the risks of a big outbreak.”

Cruise companies restarted operations in Europe and Asia late last year, and, after months of preparations to meet stringent health and safety guidelines set by the Centers for Disease Control and Prevention, cruise lines have started to welcome back passengers for U.S. sailings, where demand is outweighing supply, with many itineraries fully booked throughout the summer.

Carnival said bookings for upcoming cruises soared by 45 percent during March, April and May as compared to the three previous months, while Royal Caribbean recently announced that all sailings from Florida in July and August are fully booked.

Several coronavirus cases have been identified on cruise ships since U.S. operations restarted in June, including six passengers who tested positive on Royal Caribbean’s Adventure of the Seas recently, testing the cruise lines’ new Covid-19 protocols, which include isolating, contact tracing and testing passengers to prevent the virus from spreading. Most ships were able to complete their itineraries without issues, but American Cruise Lines, a small ship company, cut short an Alaska sailing earlier this month after three people tested positive for the virus.

The industry’s turnaround is far from guaranteed. The highly contagious Delta variant, which is causing surges of the virus around the world, could stymie the industry’s recovery, especially if large outbreaks occur on board. But analysts are generally optimistic about its prospects and the potential for passenger numbers to recover to prepandemic levels, perhaps as soon as next year. That optimism is fueled by what may be the industry’s best asset: an unshakably loyal customer base.

Even during the pandemic, huge numbers of people who had booked opted against taking refunds , instead converting payments already made into credit for future travel, which the companies often offered at a higher value as an incentive. Last fall, Carnival reported that about 45 percent of customers with canceled trips had opted for credit instead of cash back. About half of customers in a similar position with Royal Caribbean Cruises did the same by the end of last year, the company said at the time.

“The demand is there,” said Jaime Katz, an analyst with Morningstar. “You know that there have been 15 months of people who have had cruises booked that have been canceled.”

No U.S. bailout for the cruise companies

By April 2020, the industry was in crisis. Cruises were halted around the world after the alarming outbreaks on ships, leading to sailing bans from the C.D.C. and other global authorities.

While they employ many Americans, the major cruise companies are all incorporated abroad and were ultimately left out of the $2 trillion federal stimulus known as the CARES Act, with lawmakers chafing at the prospect of bailing out foreign corporations largely exempt from income taxes. Environmentalists lobbied against the aid, citing the industry’s poor track record on climate issues. And criticism over how the companies handled early virus outbreaks on board ships sapped any remaining political will to help. Huge losses mounted as questions swirled about whether cruise lines could avoid bankruptcy.

“All our conversations here were, ‘At this cash burn rate for each of these companies, how long can they survive?’” said Pete Trombetta, an analyst focused on lodging and cruises at Moody’s.

Cruise lines were forced to send most cruise workers home, keeping small skeleton crews on board to maintain their ships. After months without work or an income, many of the workers, who are frequently drawn from countries like the Philippines, Bangladesh and India, fell into debt and struggled to provide for their families.

The timing couldn’t have been worse for Virgin Voyages , the new cruise company founded by the British billionaire Richard Branson, which had planned to launch its inaugural ship, Scarlet Lady, with a sailing from Miami in March 2020. The ship’s official U.S. debut has been delayed until October, but a series of short sailings will take place in August out of Portsmouth, England, for British residents.

“It’s been a very difficult 15 months and we had to make some very tough cuts along the way like the rest of the industry,” said Tom McAlpin, president and chief officer of Virgin Voyages.

In the end, most cruise companies made it through the pandemic intact, but only after receiving help. That came in the form of assistance from governments abroad or money raised from investors emboldened by efforts to backstop the economy from the Federal Reserve and others. The cash wasn’t cheap, though. When Carnival Corp. sold $4 billion in bonds in April 2020, it agreed to interest on those bonds of 11.5 percent — more than half of which it recently refinanced at a more reasonable rate of 4 percent.

Carnival, which operates under nine brands globally, has lost more than $13 billion since the pandemic began and said in a securities filing last month that it expects those losses to continue at least through August. The company amassed more than $9 billion in cash and short-term investments as of the end of May — enough, it said last month, to pay its obligations for at least another year. It says it expects to have at least 42 ships carrying passengers by the end of November, representing just over half of its global fleet.

The industry faces a long road back to normal. Moodys downgraded ratings for each of the big three cruise companies during the pandemic and says it will probably take until 2023 for the major cruise operators to start substantially reducing their debt, which had nearly doubled during the pandemic.

The companies have also been caught up in a series of legal battles in Florida, the biggest base of operations in the United States, that has them sometimes allied with the administration of Gov. Ron DeSantis, and sometimes opposing it.

In June, Florida sued the C.D.C., saying the agency’s guidelines for how cruising could restart were burdensome and harmed the multi-billion-dollar industry that provides about 159,000 jobs for the state. The C.D.C. guidelines require 98 percent of crew and 95 percent of passengers to be fully vaccinated before a cruise ship can set sail, otherwise the cruise company must carry out test voyages and wait for approval.

So far, the state has prevailed in the courts, with a ruling from a federal judge that prevented the C.D.C.’s vaccine requirements from going into effect after July 18. A federal appeals court upheld that ruling on July 23.

Despite the court’s decision, Cruise Lines International Association, the trade group, said cruise companies will continue to operate in accordance with the C.D.C. requirements. The cruise lines found the C.D.C.’s initial guidance too onerous, but once the agency made revisions to factor in the U.S. immunization program, the companies agreed to comply and said they preferred passengers to be vaccinated, because it simplifies the onboard experience.

As that suit was making its way through the courts, Norwegian filed suit on July 13 against the state of Florida, saying that a law banning business from requiring proof of immunization from people seeking to use their services prevented the company from “safely and soundly resuming passenger cruise operations.”

There has yet to be a ruling in the case.

Hurdles remain

Several other hurdles could also derail the rebound of the industry. While cruising has resumed, operators still have to contend with a patchwork of domestic and international rules, some of which impose strict conditions on passengers who go on shore excursions. A serious and widespread outbreak aboard a ship, or a broader communitywide surge in virus infections, could drive away potential customers and stall the momentum of the cruise comeback.

But despite the delays and potential for further disruptions, Virgin Voyages is hopeful for a successful launch of its new brand. Virgin’s Scarlet Lady adult-only ship, which was inspired by a superyacht design, aims to attract a hip and younger crowd, offering 20 different buffet-free dining options and a range of entertainment, including D.J. sets and immersive experiences.

“We have a fantastic set of investors behind us, and I think we are well positioned to make a big comeback because people are ready to travel and cruise again and we are launching a very attractive new onboard product right in the middle of it all,” Mr. McAlpin said.

Two new cruise ships, Carnival’s Mardi Gras and Royal Caribbean’s Odyssey of the Seas are set to launch in the U.S. this week.

And cruise workers, many of whom burned through savings and went into debt during their enforced layoff, are thrilled to be back. “I can’t believe the day has come when I have been called back to work,” said Alvin Villorente, a wine steward for Norwegian Cruise Line, who spent the last year at home in the Philippines, carrying out odd jobs to pay his bills.

“It felt too good to be true,” he continued. “I made my wife read the email to make sure I understood correctly and when I saw her smile everything suddenly went from black to bright colors. I could look after my family again.”

At a time when airports are busy and chaotic and hotels and holiday rentals are expensive and booked up, cruise companies hope to appeal to people who wouldn’t normally consider a cruise vacation.

“I’m still on the fence about booking any travel because of the constantly changing rules around the world, but an adult-only cruise with some friends could be fun, especially if it meant not having to fly anywhere,” said Crystal Marks, a 37-year-old personal trainer from Miami who went on a cruise once as a child and has been looking at Virgin sailings for early next year after a friend sent her a promotional video.

“Yoga classes at sunrise, fitness throughout the day, city-style restaurants, spa treatments, it sounds pretty perfect to me,” she added with a laugh. “If everyone on board is vaccinated and tested regularly it’s probably one of the safer options for international travel.”

Follow New York Times Travel on Instagram , Twitter and Facebook . And sign up for our weekly Travel Dispatch newsletter to receive expert tips on traveling smarter and inspiration for your next vacation. Dreaming up a future getaway or just armchair traveling? Check out our 52 Places list for 2021 .

Ceylan Yeginsu is a London-based reporter. She joined The Times in 2013, and was previously a correspondent in Turkey covering politics, the migrant crisis, the Kurdish conflict, and the rise of Islamic State extremism in Syria and the region. More about Ceylan Yeginsu

Niraj Chokshi covers the business of transportation, with a focus on autonomous vehicles, airlines and logistics. More about Niraj Chokshi

Come Sail Away

Love them or hate them, cruises can provide a unique perspective on travel..

Cruise Ship Surprises: Here are five unexpected features on ships , some of which you hopefully won’t discover on your own.

Icon of the Seas: Our reporter joined thousands of passengers on the inaugural sailing of Royal Caribbean’s Icon of the Seas . The most surprising thing she found? Some actual peace and quiet .

Th ree-Year Cruise, Unraveled: The Life at Sea cruise was supposed to be the ultimate bucket-list experience : 382 port calls over 1,095 days. Here’s why those who signed up are seeking fraud charges instead.

TikTok’s Favorite New ‘Reality Show’: People on social media have turned the unwitting passengers of a nine-month world cruise into “cast members” overnight.

Dipping Their Toes: Younger generations of travelers are venturing onto ships for the first time . Many are saving money.

Cult Cruisers: These devoted cruise fanatics, most of them retirees, have one main goal: to almost never touch dry land .

Switch language:

Cruise in 2022: the state of the industry

Using the latest thematic insights from GlobalData, Peter Nilson looks at the state of the cruise industry.

- Share on Linkedin

- Share on Facebook

At the beginning of the year, many companies, governments, and travel authorities had predicted a stronger recovery for the cruise market in 2021. Unfortunately, that was not the case.

The pandemic has proven unpredictable, with many cruise destinations going into second and third lockdowns during 2021 after a global surge in Covid-19 cases .

Go deeper with GlobalData

Innovation in Ship: Anti-fouling Ship Hull Coatings

Environmental sustainability in ship: bio-fuel propulsion marine ve..., premium insights.

The gold standard of business intelligence.

Find out more

Related Company Profiles

The walt disney co, carnival corporation & plc, expedia group inc, norwegian cruise line holdings ltd.

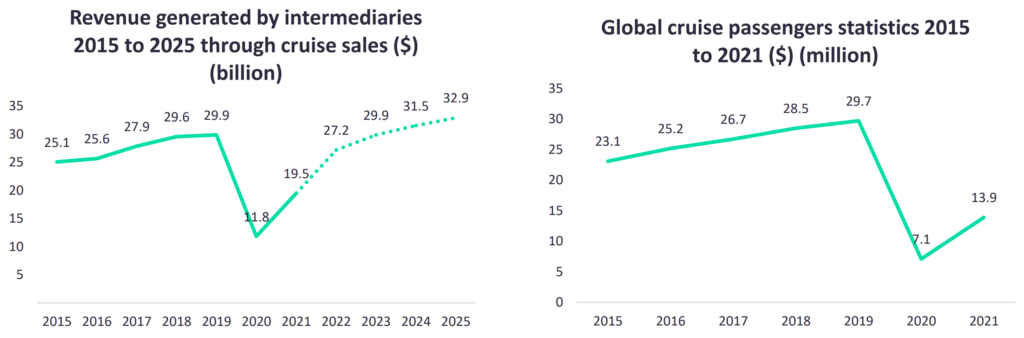

While the cruise industry has experienced a 96% Year-on-Year (YoY) increase of passengers, reaching 13.9 million, it still does not compare to the pre-pandemic levels of 2019, where there were 29.7 million passengers globally. It has been an even worse year for travel intermediaries specializing in cruise holidays.

These companies are the primary selling points for cruise trips and are often responsible for selling upgrades, premium drinks packages and excursions. Global spending across 60 major cruise markets increased by 65% YoY, resulting in total revenues of $19.4bn. Nevertheless, this was still far from pre-pandemic levels in 2019, which were approximately $29.8bn, 35% higher than 2021’s figure.

To reduce costs, many ships were retired between 2019 and 2021. Cruise ships are the most expensive assets, making this practice a necessity for many firms to stay afloat.

However, more optimistic times lie ahead for the sector. During the pandemic, the cruise industry has witnessed new innovative cruise ships and a brand-new competitor in the form of Virgin Voyages . Many cruise liners have come good with orders for new cruise ships built before the pandemic, resulting in an exciting time for loyal cruise holidaymakers to try new ships, services, and onboard experiences.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

Global cruise passengers and revenue

2021 provided a tough lesson for the cruise industry, with businesses aiming to make a swifter recovery from the latest round of lockdowns.

The cruise industry’s recovery rate was modest in 2021. Although a 96% YoY increase sounds positive, it is still nowhere near pre-pandemic levels. In 2021, only 13.9 million passengers went on a cruise, 53% lower than the pre-pandemic levels of 2019.

With the fluctuations of global passengers, revenues will generally follow a similar pattern unless there is a substantial shift in consumer behaviour. Usually, the most significant impacts on a travel company’s revenues, aside from passenger flows, are an economic recession, foreign exchange, or a change in booking trends.

During the pandemic, it has become clear that the latter affected cruise intermediary revenues. In 2021, revenue generated for cruises from intermediaries reached $19.5bn, a 65% YoY increase from $11.8bn. However, cruise passenger flows increased by 95% YoY, which is a significantly higher rate of improvement.

According to the CEO of the Royal Caribbean Group, Richard Fain, this was not unexpected. The world’s fourth-largest cruise company has seen intermediaries such as online travel agencies (OTAs) and high street agencies lose a proportion of their market share, with customers opting to book directly with the cruise operator rather than a third party.

The same sentiment was echoed by Norwegian Cruise Lines CEO Frank Del Rio, who said the company had witnessed a similar booking pattern. The result is not surprising. Many agencies have had to cut back on their workforce due to poor revenue performance in 2020, resulting in fewer sales agents to capture the rising demand in 2021. This has led to more customers booking directly with cruise companies.

Research from GlobalData also supports this, when comparing two consumer surveys from 2019 and 2021. In 2019, 44% of respondents said they typically book via an OTA. However, in a Q4 2021 survey, only 24% of respondents said they booked their last holiday via this booking method. In addition, respondents who said they booked directly increased from 32% to 36%.

New cruise ships and trends for 2022

There are many new cruise ships scheduled to set sail in 2022. Many of these boast a more contemporary feel to their décor and interior, moving away from the traditional looks of the past cruise ships and moving to a more fashionable boutique hotel design.

The motivation for this stems from the fact that cruise operators need to attract a younger market. This evolution is necessary for making cruise businesses more resilient in the future by drawing the next generation of cruise tourists.

According to a 2020 GlobalData survey, 37% of Gen Z and Millennials said that they ‘strongly’ or ‘slightly’ agreed with the notion that they would book an international trip this year. In comparison, only 22% of those older than 35 responded with the same sentiment, highlighting that the younger generation may be more likely to travel in today’s travel climate.

Furthermore, cruising has also become more popular with younger adults. In GlobalData’s Q3 2019 and 2021 global consumer surveys, the percentage of Gen Z and Millennial respondents who typically take a cruise holiday increased from 17% to 21%, indicating changes in consumer tastes.

The importance of Covid-19 safety protocols on cruise ships has never been more critical. According to GlobalData, there is a demand from consumers to receive information about Covid-19 initiatives. This data shows that consumers need substantial levels of communication from cruise providers, and that cruise companies will need to develop robust communication strategies, which need to be scaled over the next few years.

Many travellers are opting to book directly with the operator rather than via an intermediary such as an OTA. According to a Q3 2019 GlobalData survey, 44% of consumers said they typically book via an OTA.

However, this has fallen substantially over the last two years. In a Q4 2021 survey, only 24% of respondents said they booked their previous holiday via an OTA.

In addition, respondents who said they booked directly with a travel supplier increased from 32% to 36%, showing that booking directly with the supplier is becoming more trustworthy and popular.

Nevertheless, this booking behaviour could well be a temporary result, with some cruise operators expecting intermediary trade to pick up again in 2022.

Sign up for our daily news round-up!

Give your business an edge with our leading industry insights.

More Relevant

Orient Express adds Brunvoll propulsion to Silenseas sailing cruise ship

Leading robotics companies in the shipping industry, bunker fuels, lubricants and fluids for the shipping industry, ship corrosion prevention: cathodic protection, coatings and insulation for the shipping industry, sign up to the newsletter: in brief, your corporate email address, i would also like to subscribe to:.

Ship Technology In Brief

Ship Technology Global : Ship Technology Focus (monthly)

I consent to Verdict Media Limited collecting my details provided via this form in accordance with Privacy Policy

Thank you for subscribing

View all newsletters from across the GlobalData Media network.

Growth of the Ocean Cruise Line Industry

Worldwide, the ocean cruise industry experienced an annual passenger compound annual growth rate of 5.9% from 1990 to 2024.

While the COVID-19 pandemic brought the ocean passenger cruise industry to a standstill for nearly two years, it also prompted the accelerated retirement of numerous older ships. Simultaneously, new additions to fleets adopted a more modern and environmentally friendly approach. In 2024, passenger numbers are expected to surpass the pre-COVID levels of 2019.

Between 2023 and 2024, a total of 10 new ships, with a combined passenger capacity of 25,450, are set to be added (refer to the tables below). This influx will bring the worldwide ocean cruise passenger capacity to 673,000, spread across 360 ships. These vessels are projected to carry a total of 30.0 million passengers by the end of 2024, representing a 4.2% increase over 2023 and a 9.2% increase over 2019.

Shipbuilding Summary

Sources: Royal Caribbean Cruises, Ltd., Carnival Corporation and plc, NCL Corporation Ltd., Thomson/First Call, Cruise Lines International Association (CLIA) , The Florida-Caribbean Cruise Association (FCCA) , DVB Bank and proprietary Cruise Market Watch Cruise Pulse data.

Royal Caribbean lifts profit view again on cruise boom, higher prices

- Medium Text

Sign up here.

Reporting by Juveria Tabassum in Bengaluru and Doyinsola Oladipo in New York; Editing by Devika Syamnath and Shounak Dasgupta

Our Standards: The Thomson Reuters Trust Principles. New Tab , opens new tab

Business Chevron

Ex-McKinsey partner sues firm, claims he was made opioids 'scapegoat'

A former McKinsey & Co partner sued the global consulting firm on Friday and accused it of defaming him and making him a "scapegoat" to distract attention from its work advising OxyContin maker Purdue Pharma and other manufacturers of opioid pain medications.

- CLIA Cruise Lines

- CLIA Global Executive Committee

- Mercy Ships

- Explore Topics

- Join or Renew

- Professional Development

- Travel Agent Cruise News

- Verify a Member

- Eligibility

- Marketing Partners

- Refund Policy

- Executive Partners

- Fact Sheets

- News and Media Room

- Australasia

- North America

- North West and Canada

- UK & Ireland

- My Certifications

- My Training

- Find a Travel Agent

- Cruising Home

- News and Research

- News Releases and Statements

- Cruise Industry Contribution to U.S. Economy Grew to 55.5 Billion in 2019, Generating More Than 436,000 American Jobs

Press Release | November 19, 2020

Cruise Industry Contribution to U.S. Economy Grew to $55.5 Billion in 2019, Generating More Than 436,000 American Jobs (USA)

Pre-pandemic industry output grew 5.3% in 2019 compared to 2018, fueled by rising popularity of cruise vacations and nearly 14 million passenger embarkations from u.s. ports.

NOVEMBER 17, 2020 (Washington, DC) —Cruise Lines International Association (CLIA), the leading voice of the global cruise industry, announced new economic impact data from its annual report on the contributions of the cruise industry to the U.S. economy. The newly released 2019 U.S. Economic Impact Analysis underscores the tremendous growth of the cruise industry and the corresponding growth of the industry’s contributions to the U.S. economy prior to the global health emergency.

In 2019, the cruise industry generated a total of $55.5 billion in economic activity in the United States, a 5.3% increase from 2018. Moreover, growth in economic activity was accompanied by an increase in industry-supported jobs. According to the report, the cruise industry supported 436,600 American jobs paying $24.4 billion in wages in 2019—a 3.5% and 5.4% increase from 2018, respectively.

The latest figures follow nearly ten years of continued growth in the cruise industry, fueled by the rising popularity of cruise vacations. Over 13.7 million passengers embarked on cruise ships from U.S. ports in 2019, up nearly 8% from 2018 and 26% from just five years ago.

“The pre-pandemic trends clearly demonstrate that cruising has emerged as one of the fastest growing sectors of travel and tourism,” said Kelly Craighead, president and CEO of CLIA. “The cruise industry is proud to play an important role in the creation of jobs and economic opportunity for nearly half a million Americans throughout the country. At the same time, we recognize the devastating impact that COVID-19 has had on our community. A resumption of cruising in the United States in 2021, with stringent measures in place and with the support of health authorities, will be critical to putting people back to work and fueling the greater economic recovery from the pandemic.”

The report highlights the cruise industry’s economic contributions across multiple sectors, from transportation and aviation, to food and beverage, lodging, manufacturing, agriculture, travel agencies and a robust supply chain that stretches across the United States. The top ten states benefitting economically from the contributions of the cruise industry include:

The full report is available here , along with corresponding infographics and fact sheets.

Media Inquiries

Please send media inquiries to - [email protected]

Don’t yet have a login? Create a new account

Forgot Password

If you have forgotten your Password, complete the information requested below and click the submit button.

You will receive an email with a reset token to change your password.

Please allow at least 10 minutes to receive the email before requesting another password reset. Please be sure to check your Spam folder for the password reset email.

Please note: the Email you provide must be the one that is associated with your profile.

If you have difficulty resetting your password please email [email protected] .

Create a New CLIA Account

Set or change password.

Please use the form below to set or change your password. Passwords must be at least 8 characters.

We are sorry. An error has occurred.

Please confirm, select your region to be directed to the correct website.

An official website of the United States government

The .gov means it’s official. Federal government websites often end in .gov or .mil. Before sharing sensitive information, make sure you’re on a federal government site.

The site is secure. The https:// ensures that you are connecting to the official website and that any information you provide is encrypted and transmitted securely.

- Publications

- Account settings

Preview improvements coming to the PMC website in October 2024. Learn More or Try it out now .

- Advanced Search

- Journal List

- Elsevier - PMC COVID-19 Collection

The global cruise industry: Financial performance evaluation

The global cruise industry has experienced persistent growth dynamics over the last two decades, with an impressive rebound after the 2008 financial crisis, unlike commercial shipping. Globalization, restructurings, mergers and a diverse bundle of travel and tourism services to cater for different passenger profiles have boosted robust revenue and profitability growth. Major cruise companies deploy ambitious investment plans to expand and renew their expensive fleet with larger modern vessels of high value. The mix of funding sources to finance these capital-intensive projects is critical and exerts a direct impact on the cost of capital. The paper contributes a rigorous corporate financial performance evaluation in the cruise sector and attempts to shed light on managerial financial efficiency, capital structure options, solvency conditions and corporate value dynamics. A sample of leading cruise companies, jointly holding a dominant market position, is incorporated to empirically investigate and assess their financial, accounting and stock market performance, based on convenient financial ratios and established market metrics. The detrimental impact of the recent coronavirus pandemic on the cruise sector is also discussed. This original study attempts to bridge the relevant research gap, as past literature remains surprisingly thin on this critical topic. A set of challenging and innovative contributions is delivered for the financial performance of major cruise companies, for the first time to the authors' knowledge, in support of efficient managerial implications and recommendations.

1. Introduction

Cruise tourism business is a form of traveling for leisure purposes that involves an all-inclusive holiday on a cruise ship. According to UNWTO, cruise tourism includes ‘a wide range of activities for travelers in addition to its traditional function of providing transport and accommodation’. The cruise industry is the fastest growing sector of the travel industry, with demand estimated to grow at 7.0% per annum over the past decade, and cruise passenger surpassing the threshold of 30 mln. in 2019 ( CLIA, 2020 ; Wondirad, 2019 ). At the same time, the business is seen to be extremely volatile and ever more highly capital-intensive. Newbuilt cruise vessels can cost multiples in value compared with commercial ocean ships, estimated at $1.3 bln. per vessel, accommodating up to 6000 passengers, albeit at lower operating unit costs ( Dowling, 2006 ; Lester & Weeden, 2004 ; Wood, 2004 ). Nevertheless, in the 1990s, the cruise industry has experienced extensive restructuring, following a wave of failures and consolidations. Larger holding cruise companies acquired smaller peers that continued operating as ‘brands’ withing the new business ventures though, serving repeat customer loyalty and offering diverse quality and service levels.

Financial empirical research on cruise shipping remains surprisingly thin. Few earlier studies investigate, selectively, topics such as, the translational partnership organization of the industry ( Hall & Braithwaite, 1990 ); cruise impact on and implications for regional and local market development ( Hobson, 1993 ); cruise market globalization trends ( Wood, 2000 ); cruise strategic capacity investments ( Byung-Wook, 2005 ; Wie, 2005 ); cruise line and passenger challenges ( Veronneau & Roy, 2012 ); cruise line supply chains and logistics ( Daly & Fernandez-Stark, 2017 ; Veronneau and Roy, 2009 , Veronneau and Roy, 2011 ; Veronneau, Roy, & Beaulieu, 2015 ); fund raising approaches for newbuilding cruise ships ( Kiziellewicz, 2017 ; OECD, 2007 ); and mergers, acquisitions and restructurings ( Charlier, 2004 ; Hobson, 1994 ); inter alia.

This study focuses on the financial performance evaluation of the global cruise business and attempts to fill this research gap in the field by contributing a set of challenging and innovative findings, as well as managerial implications and recommendations. To the authors’ best knowledge, this appears to be the first attempt to investigate in depth the critical issues of managerial efficiency, profitability, and growth prospects, financing sources and capital structure, leverage, solvency, and value creation dynamics in the context of the global cruise industry. Initially, a concise overview of prevailing key developments and trends in the cruise business over recent years is provided. Subsequently, critical key financial metrics and performance indicators are estimated and evaluated over time and against major peer competitors for a sample of leading cruise players.

The theoretical framework and the stream of literature that the paper is grounded on relates to critical investment and financing decisions and their financial implications for managerial performance, corporate profitability, value creation, and firm growth. To this end, in a broader context, a core set of seminal reference papers investigate key managerial decisions on funding source options (debt and/or equity), capital structure mix priorities, (weighted average) cost of capital (WACC) shifts, and share price volatility, inter alia, as well as their interrelated implications for investment decisions and overall corporate financial performance (e.g., Baker & Wurgler, 2002 ; Donaldson, 1961 ; Hovakimian, 2006 ; Kisgen, 2006 ; Modigliani and Miller, 1958 , Modigliani and Miller, 1963 ; Myers, 1984 , Myers, 2001 ; Myers & Majluf, 1984 ). It remains an innovative, challenging and fruitful empirical task to investigate the financial implications of these decisions and evaluate the managerial efficiency and financial performance of major global cruise companies, as depicted and reflected on the evolution of critical and widely established financial ratios and metrics. Indeed, these issues are not seen to have been investigated yet in the relevant empirical literature. Nevertheless, they remain important for a highly capital-intensive sector, such as the cruise industry, taking, indicatively, into consideration that the cost of a newbuild cruise vessel can now surpass the $1.0 bln. threshold ( CLIA, 2020 ).

The empirical approach is based on a blended financial methodology, including preliminary data mining and collection, financial statement analysis and comparative assessment and evaluation of critical cruise financial ratios and indices. Based on that, a set of focal policy recommendations is finally provided. The information input is obtained from financial statements and annual reports, stock market datasets and company financial analysis reports, over a recent five-year horizon.

The paper is structured as follows. Section 2 provides a concise summary of recent developments in cruise demand and supply sides, identifying critical growth drivers, economic implications, and prospects ahead. Section 3 overviews major cruise company investment decisions; and Section 4 analyses the complex topic of financing decisions and fund-raising approaches, based on alternative capital structure options that eventually shape the critical cost of capital indicator. Section 5 investigates, analyses, and evaluates a set of key financial ratios, metrics, and indicators to assess cruise company financial performance and value creation dynamics. Finally, Section 6 concludes.

2. Cruise business growth drivers

2.1. demand for cruise services and economic impact.

Cruise shipping business offers a bundle of combined global shipping and tourism services to cruise passengers, as it caters for vacation services on board and ashore, with a full package of diverse recreational tourism-related services. However, a fundamental strategic shift is seen in global cruise business over time ( Garin, 2005 ). Whereas in earlier days, cruise shipping services were mainly targeting higher net-worth luxury customers at substantial price cost, the industry has gradually diversified to demonstrate market segmentation and to attract massively average-income cruise passengers of different age and social profiles. This trend has been supported by attractive cruise service packages at reasonable prices, as massive newbuilt vessel capacity has resulted to extensive economies of scale benefits. Broadly, cruise shipping is perceived as a ‘customer's market’, shaped by shifting consumer tastes and trends. Cruise passengers appear to increasingly prefer ‘paying more for experiences than for possessions’.

Cruise shipping is the fastest-growing segment in the leisure travel market with high capacity utilization rates. The prime cruise business actors include more than 55 cruise line companies, offering ocean, river, and specialty cruise services, and covering more than 95% of global cruise capacity. Business members include also more than 340 executive partners that are key suppliers and cruise line partners, including ports and destinations, ship development suppliers and business services; around 15,000 travel agencies, including the largest players, hosts, franchises and consortia; and, 25,000 travel agent members worldwide ( CLIA, 2019 ).

Contrary to commercial ocean shipping, the global cruise business has shown robust growth rates and persistent recovery, after the 2008 financial crisis. In terms of total revenue, the cruise industry generated $46.6 bln. in 2018, exhibiting a spectacular rebound since revenue had declined abruptly below $25 bln., due to the recession spread after 2008 ( CLIA, 2020 ). The economic output generated by the global cruise industry is estimated at $150 bln. in 2018 against $126 bln. in 2016 (+20%, 2018/2016), with 28.5 mln. cruise passengers, offering 1.17 mln. jobs (full-time equivalent employees; +6.2%, 2018/2017), and distributing $50.2 bln. in wages and salaries ( CLIA, 2018 , CLIA, 2019 ). In view of global passenger spending capacity, estimates indicate aggregate direct purchases of $7.97 bln. (+11.4%, 2018/2017), corresponding to $376 average passenger spending before boarding a cruise and to $101 in port visiting during a cruise. Furthermore, 65% of cruise passengers is seen to spend a few extra days at embarkation or debarkation ports. Cruise business is seen to develop around Caribbean, Australasia, Brazil, Europe, North America, Asia, Canada, UK, and Ireland. The worldwide income multiplier effects of the cruise industry have wider economic implications, as these disseminate to a wide spectrum of related business sectors and activities.

Over 2008–2018, the global cruise business has experienced an unprecedented 10-year average growth above 45% in sourced cruise passengers ( CLIA, 2019 ; Florida Caribbean Cruise Association, 2019 ). This performance is attributable predominantly to the spectacular passenger growth from European markets (60.4%), followed by North American markets (39.4%). This figure raises up to nearly 75% if passenger growth of the rest of the world is also counted ( Table 1 ). The number of total cruise passengers came up to 30 mln. in 2019 from 16.3 mln. in 2008 (+84%). A steady cumulative annual passenger growth rate (CAGR) at 7% is estimated over 1990–2020.

International demand for cruises (sourced passengers, mln).

Source: CLIA (2019) .

Initial estimates on the number of annualized worldwide cruise passengers carried indicate 32.0 mln. passengers for 2020 against 3.6 mln. passengers back in 1990 (+790%, 2020/1990) ( Fig. 1 ).

Global cruise passengers carried (mln.)

Cruise passengers originate from a diversity of geographic regions and source markets ( Table 2 ). North America remains by far the largest source region of cruise passengers, contributing more than half of global cruise passenger flows (50.2%); its share, though, has dropped compared with 2007 (66%). Europe follows at a distance (23.7%) and has also seen its share slightly on the decline. Asia, on the other hand, is a robustly upcoming cruise passenger source region (15.0% in 2019, up from 9.2% in 2018).

Worldwide cruise passenger by source region (%).

Europe: Benelux, France, Germany, Italy, Scandinavia, Spain, Portugal, UK. Source: CLIA (2020) .

The breakdown of preferred destinations, as depicted by cruise line deployment by region is presented for 2018 and 2019 in Table 3 . The Caribbean remains by far the prime cruise destination of high demand (32%) with the Mediterranean (17%) and Europe (excluding Mediterranean; 11%) following at a distance ( Table 3 ).

Cruise line deployment by region (%).

Source: CLIA (2020) .

The cruise market share distribution among major cruise players is presented below ( Table 4 ). Three leading players are seen to dominate the global cruise market. Carnival Corporation holds a dominant position with passenger and revenue market shares at 47.4% and 39.4%, respectively. Royal Caribbean Cruise ranks second with passenger and revenue shares at 23.0% and 20.2%, respectively. Norwegian Cruise Line Holdings follows at a distance with passenger and revenue shares at 9.5% and 12.6%, respectively. These three major players control a global cruise market share of 80% in passenger terms and 72.2% in revenue terms, respectively.

Cruise line market share.

Source: Authors' compilation; www.cruisemarketwatch.com .

2.2. Growth drivers and prospects

Cruise shipping growth is driven by consistent efforts of all parties involved to explore alternative approaches towards increasing business efficiencies. These include further newbuilding investments to expand and modernize cruise fleet, adding new vessels of larger capacity, diversifying the destination choices offered, increasing penetration in core North American and Latin American markets, attracting more passengers from new source markets and enriching on-board and on-shore activities to meet cruise passenger demands. Furthermore, the inclusion of more local ports has been treated responsibly, based on collaboration with cruise destinations and local communities. The cruise industry is seen to become more conscientious, paying attention towards preservation of local cultures and landmarks and minimization of environmental footprints; exploring alternative creative ways to manage visitors' flows; and, implementing higher standards of responsible tourism. The latter include partnerships with local governments, staggered arrivals and departures, local excursion diversification, shoreside power, and local passenger spending, as more travelers are spending time in and near cruise ports (e.g., Klein, 2011 ).

Broadly, the cruise industry demonstrates promising growth dynamics ahead. This is supported by a global shift in consumer tastes and habits around cruise services, irrespective of passenger generation. For instance, more than 66% of generation ‘X', 71% of millennials, and expanding percentages of generation ‘Z', originating predominantly from the vital US market, are seen to have an increasingly positive attitude towards cruise travel and tourism services compared with earlier years. Generation ‘Z' is anticipated to become the largest consumer generation by 2020 outpacing even millennials. This generation, like the one before, prefers experiences over material items. They appear to prefer cruise travels, including multiple destinations and targeted specialized services (such as music festivals at sea, for instance; CLIA, 2020 ).

Cruise passenger numbers originating from major emerging markets, such as China, India, and Latin America, are anticipated to increase further, supported by improving global disposable income and economic growth conditions. In addition, social demographic shifts indicate that, as global marriage rates are on a decline, increasing numbers of single adults are seen to pursue lone cruise services with a ‘traveling alone’ focus. Cruise lines respond to this upcoming clientele by offering, targeted ‘solo travel’ services, such as studio cabins, solo-lounges, and single-friendly activities. Another upcoming cruise clientele sub-group is female travelers, as their numbers are seen growing. Many tourism and travel companies are creating female-centered cruise itineraries, based on focused interests, and facilitating building women community bonds ( CLIA, 2020 ). Relevant references investigating these issues further include Teye and Leclerc (2003) , Chen, Neuts, Nijkamp, and Liu (2016) , Satta, Parola, Penco, Persico, and Musso (2016) , inter alia.

What is more, cruise travelers are now seen to set sights on destinations that were previously out of reach and some only accessible by cruise ships from the Galapagos Islands to Antarctica. Demand for off-peak season cruise packages also exhibits rising popularity, as travelers may prefer to visit tropical destinations to escape a domestic cold season. The number of modern ‘digital nomads’, that is travelers combining work with leisure time, is also on the rise. This target group can enjoy cruise vacation services in conjunction with remote e-work, cutting down on time-off and still earning an income. On the other hand, micro travel cruise services exhibit upward demand trends as well, as many travelers are interested in quick recreational trips of varied and flexible trip duration alternatives. In response to that, cruise companies offer bite-sized cruise options of three-to-five-days, scheduling shorter itineraries to a variety of destinations.

3. Investment decisions in the cruise business

The cruise companies promote consistently a set of ambitious and capital-intensive strategies to sustain business growth. Newbuilding investment projects target to expand and modernize the existing fleet with vessels of larger capacity. Total cruise industry capacity reached 537 thous. passengers and 314 ships, with about 55 active cruise companies at the end of 2018 ( CLIA, 2020 ). The brand diversification of operations is summarized in Table 5 .

Cruise passenger capacity.

Source: Authors' compilation; CLIA (2020) .

Most cruise players have large investment plans under deployment, scheduled over 2019–2025. For instance, Carnival, Royal Caribbean, and Norwegian plan to invest $4.2 bln., $7.2 bln., and $4.5. bln., respectively, in newbuilding vessels, aggregating to $16 bln. in investments. With total cruise sector investments adding up to $70.3 bln., the joint investment share of these three major players corresponds to 23% of total cruise investment budget ( Table 6 ).

Newbuilding investments – capital requirements (USD bln.), 2019–2025.

Source: Authors' compilation; www.cruisemarketwatch.com (2020).

Broadly, an impressive newbuilding cruise vessel orderbook is under execution over 2019–2025 ( Table 7 ; more details in Table 7A in the Appendix; ( WAC, 2019 )). It is worth noting that the large vessel size in several cases can accommodate more than 6000 cruise passengers. Recent feedback on cruise investment plans indicates that 278 vessels are projected in operation by the end of 2020 and 19 vessels are scheduled to debut in 2020. The average age of cruise fleet is seen at 14.1 years, improved from 14.6 years in 2018.

Cruise ship newbuilding orders, 2019–2025.

A broader issue of concern for cruise investments relates to the environmental sustainability commitment. While cruise ships comprise less than 1% of global maritime fleet, the entire shipping industry benefits from the adoption of new technologies and practices that were not in play earlier. The development of new technologies and cleaner fuels remains a high priority for the cruise industry. Estimates indicate that the cruise companies have invested over $22 bln. in new energy-efficient ships and technologies to minimize the environmental impact, supporting the goal of reducing carbon emission rates by 40% by 2030 compared to 2008 ( CLIA, 2020 ). As per new emission standards, sulfur in the fuel is limited to 0.5% from January 2020. The cruise industry is also seen to be consistently committed to responsible tourism practices, with a focus on destination stewardship, setting-up partnerships with local governments in key destinations. A complementary concern relates inevitably to cruise hosting port constraints, including market segmentation, vessel size service capacities, seasonality effects and congestion bottlenecks at peak periods. To that end, cruise players are anticipated to invest further into port facilities and related infrastructure.

Having said that, the compliance of cruise companies to environmental protection is associated with high investment costs for the construction of new generation cruise ships. Vessel manufacturing costs also rise as ships incorporate innovative advanced technologies. Although cruise vessel prices are seen, on average, at around half a billion dollars, updated estimates indicate this figure to now surpass the one billion dollars threshold ( CLIA, 2020 ). To that end, the critical questions as to how these massive investments are to be financed and at what capital cost remain to be tackled. Following the global financial crisis, several leading international banks specialized in ship credit, such as RBS and DVB, have decided to exit ship lending entirely, liquidating their ship loan portfolios. On the other hand, an emerging global trend relates to private entry strategies, partnerships, and internationalization patterns of cruise companies entering cruise terminal operations in major destinations, such as the Mediterranean Sea ( Pallis, Parola, Satta, & Notteboom, 2018 ). Plausibly, the deployment of such strategies is anticipated to bring about considerable financial implications for cruise lines and cruise terminals, both in terms of spending patterns as well as of income.

4. Financing decisions in the cruise business

4.1. capital funding priorities.

The financing approach a cruise company is to follow to fund its investments and the contribution of alternative capital source options are of fundamental managerial importance. Obviously, this should have direct implications for this cruise company's optimal capital structure mix and its cost of funding. The investigation of these issues in the context of cruise companies remains a challenging and innovative task. To the authors' knowledge, this appears to be the first empirical study tackling these issues in the cruise industry. This research interest is further reinforced and justified considering that the global cruise industry is a highly capital-intensive business with consistent investment expansion plans under development over the last decades, associated with substantial funding requirements. As noted earlier, most cruise companies plan to expand and upgrade their fleet and have already placed a massive newbuilding orderbook under play. The incorporation of luxury facilities and high-end technological advances and services drive unit vessel prices even higher than $1.3 bln. ( CLIA, 2020 ).

Managerial financing decisions have direct implications for the cruise company's capital structure mix, its cost of capital and, eventually, shareholder value creation and growth prospects. The capital structure mix refers to the percentage weights of equity and debt, reflecting the respective capital source contribution to form the company's total invested capital. As the cost of equity and cost of debt differ, modifications in the capital structure mix also affect the company's overall cost of capital. These focal issues have generated steaming debate among academics and market practitioners over time. A summary of major finance theories on capital structure is now provided and subsequently explored briefly in the context of the cruise business.

Modigliani and Miller (1958) , first, postulate the capital structure irrelevance approach. Assuming perfect markets and absence of taxes and bankruptcy costs, the capital structure mix is irrelevant because firm market value is determined by the company's earning power and the risk of its underlying assets. Modigliani and Miller (1963) incorporate, subsequently, the tax effect on capital cost and firm value. In this case, firm value increases with leverage due to tax shield benefits. Interest on debt capital is an acceptable deduction from the firm's income and thus decreases the firm's net tax payment. Assuming potential tax benefits, debt financing can result to lower cost of capital.

Trade-off theory, furthermore, argues that the optimal level of debt is where the marginal debt benefit is equal to its marginal cost ( Myers, 1984 ). Debt financing up to a certain level contributes interest tax shield benefits, offsetting financial distress costs. A firm can attain an optimal capital structure by adjusting debt and equity weights, thereby balancing tax shield benefits and financial distress costs. Myers and Majluf (1984) postulate the pecking order theory, based on earlier research by Donaldson (1961) , and argue that (assuming perfect capital markets) management prefers internally generated funds rather than raising external funds. A company should prefer internal funding first, then issue debt, and finally, as a last resort, issue equity capital. Firms with higher profit and growth opportunities would use less debt capital ( Myers, 2001 ). If a firm has no investment opportunities available, profits are retained to avoid future external financing. Information asymmetry between insiders and outsiders and separation of ownership can explain why firms avoid capital markets.

Market timing theory of capital structure maintains that companies are more likely to issue equity when their market value is high, relative to book and past market values, and to repurchase equity when their market value is low ( Baker & Wurgler, 2002 ). Share price volatility affects corporate financing decisions, and eventually the firm's capital structure. As the resulting effects on capital structure are persistent, this indicates that current capital structure is strongly related to historical market values. Capital structure is perceived to be the cumulative outcome of past attempts to time the equity market. It is argued though, that market timing does not exert material effects on the firms' capital structure in the long run ( Hovakimian, 2006 ). The credit rating-capital structure (CR-CS) hypothesis is proposed as an extension of the existing trade-off theory of capital structure ( Kisgen, 2006 ). Capital structure decisions are expected to adjust along the relevant benefits and costs associated with shifts between different credit rating levels. When a firm is closer to a rating shift, it may issue less debt compared to the alternative of being far from a credit rating shift.

To sum up, debt financing can offer a lower cost of capital, due to tax deductibility advantages. A company with positive prospects can proceed to raise capital using primarily debt rather than equity, so to avoid ownership dilution (transmitting negative signals to market players). Debt signaling (company announcements of funding with debt) is typically seen as positive news. However, a high debt exposure bears enhanced bankruptcy risks, and increases shareholders' financial risks, thus a higher return on equity is required. To conclude, companies must assess their optimal funding mix at which the marginal benefits of debt equal the marginal costs incurred. The optimal capital structure mix is associated with that combination of equity and debt financing that results to a lower cost of capital, supporting robust value creation prospects.

4.2. Capital structure mix and WACC

Based on 2019 figures, all three major cruise companies have seen their long-term debt exposure increased against 2018, by 22.8% at $9.7 bln. for Carnival, by 8.4% at $9.0 bln. for Royal Caribbean, and, by 5.2% at $6.1 bln. for Norwegian ( Table 8 ). This reflects a debt weight reallocation in the capital structure mix for Carnival and Norwegian, though this remained stable for Royal Caribbean. Over 2016–2019, debt funding contribution increased from 41.9% to 43.7% for Carnival and from 59.2% to 59.9% for Royal Caribbean but declined overall from 65.1% to 61.1% for Norwegian. On average, Carnival is seen to rely more on equity funding (equity/debt mix: 60/40), contrary to Royal Caribbean and Norwegian that are seen to be more dependent on debt (equity/debt mix: 40/60) ( Table 9 ; Fig. 2 ).

Capital sources (USD bln.).

Source: Authors' calculation based on cruise company financial statements.

Cruise company capital structure mix (%).

Capital structure mix components.

As the capital structure of major cruise companies indicates, the funding mix is relatively balanced with a reasonable exposure to debt risk. This comes in contrast to global commercial shipping business that is seen to be typically financed predominantly by bank lending ( Drobetz, Gounopoulos, Merikas, & Schroder, 2013 ; Syriopoulos, 2007 , Syriopoulos, 2010 ).

The weighted average cost of capital (WACC) is a critical metric for a company's aggregate cost of funding from all potential capital sources. It is calculated as the weighted average cost of equity and cost of debt (weighted contribution of equity and debt (plus of any other capital source) in total invested capital), that is:

where: k e = cost of equity; E = Equity; k d = pre-tax cost of debt; t = corporate tax rate; D = Debt; E/(E + D) and D/(E + D) = weights of equity and debt in the company's capital structure, respectively.

Hence, WACC is a key indicator of the minimum after-tax required rate of return which the cruise company must earn for all its investors (capital suppliers, i.e. shareholders and debtholders). At the same time, the company's cost of capital is the expected return to both stakeholders (owners and lenders) and represents investors' opportunity cost of taking on the risk of investing their funds into the company. More specifically, cost of equity is the required rate of return on common stock of the company. It is the minimum rate of return which a company must earn to keep its common stock price from declining. Cost of equity is estimated using alternative models (including, dividend discount model (DDM) and capital asset pricing model (CAPM)). After-tax cost of debt represents the after-tax rate of return debtholders require to earn until debt maturity. Cost of debt is calculated by assessing the yield to maturity of the company's bonds and other loan instruments. If no yield to maturity is available, the cost of debt can be estimated using the instrument's current yield. After-tax cost of debt is included in WACC calculation because debt offers a tax shield (i.e., interest expense on debt reduces taxes and this is incorporated in the cost of debt calculation). The WACC factor for major cruise companies in 2019 is summarized below ( Table 10 ).

Cruise company cost of capital, WACC (%).

WACC: Weighted Average Cost of Capital. Year: 2019.

Source: Authors' calculation based on cruise company financial statements and Bloomberg database.

The next section focuses on the core research objectives and develops the empirical methodology on the financial performance evaluation of major cruise companies to contribute a set of fruitful managerial recommendations, and conclusions.

Fig. 3 illustrates the underlying logical nexus and summarizes the earlier key points, interrelating cruise company investment and financing decisions with critical corporate financial performance ratios and metrics to follow in the next section and highlights the paper's contributions to the topic at hand.

Nexus of investment and financing decisions to cruise company financial performance.

Source: Authors' compilation.

5. Financial performance evaluation: Methodology and key findings

This section deals with a solid quantitative assessment of corporate financial performance dynamics, and trends shaped in the cruise industry, over the period 2016–2019. As mentioned, this topic remains surprisingly unresearched in the relevant academic literature (e.g., Clancy, 2017 ). To explicitly state the research objectives and innovative contributions of this study, the following critical issues are investigated for leading global cruise companies: the ambitious investment plans under deployment; the capital funding priorities and sources, based on the decomposition of the capital structure mix; and, the assessment and evolution of the WACC metric over time. To assess, subsequently, the profitability robustness, value creation dynamics and growth prospects of the sample cruise companies, an integrated financial performance evaluation approach is undertaken, based on a widely applicable, financial ratio analysis, focusing on the following key issues: revenue and profit growth; managerial efficiency, as depicted by ROE, ROA, ROIC ratios; the ROIC-WACC interrelationship and its growth and value dynamics implications; financial leverage exposure and solvency assessment; and earnings per share ratios and share price performance over time.

To serve these research objectives, the empirical methodology is based on a solid corporate financial analysis, assessment, and evaluation of critical financial ratios and established metrics on key cruise market players, built on financial statement, accounting, and stock market inputs. This applied approach can then produce useful empirical findings and policy recommendations for efficient managerial decisions of the cruise companies. Though this methodological framework is standard in different business sectors, to the authors' best knowledge, this appears to be the first empirical application to global cruise corporate players.

A case study company sample is selected, consisting of the major cruise players, namely Carnival, Royal Caribbean, and Norwegian cruise lines. As discussed earlier, these cruise companies hold an undoubtedly dominant market share, as they jointly control more than 80% of the global cruise market in terms of revenue and passengers and set the financial tune in the sector ( CLIA, 2020 ). Hence, by focusing on these companies, a solid, reliable, and sufficiently representative feedback can be gained for the overall cruise sector. Furthermore, these leading cruise companies have their shares listed and traded on international stock exchanges (New York, London); thus, useful empirical reflections can be gained by their stock market behavior, performance, and market value. The consolidated financial statements of the sample cruise companies have been incorporated for the empirical financial analysis. These cruise companies own several subsidiaries (e.g., Carnival Corporation & PLC owns Costa Crociere, and Aida Cruise, through Costa Group; as well as it owns P&O Cruises and Cunard, through Carnival UK, etc.), and the strategies of the parent companies are realized also by their own brands.

As a point of clarification, MSC Cruise is also an important cruise market player, though it holds a relatively lower market share compared with the other sample companies. MSC was initially included in the preliminary sample compilation under study. However, it was eventually excluded from the final sample, to preserve data consistency and convergence, as MSC Cruise is not listed on a stock exchange and a part of the research interest is in the stock market behavior of the listed cruise companies. Due to the dominant market share and economic importance of the sample cruise companies, the empirical analysis and findings are not expected to be affected materially by the exclusion of MSC Cruise. In any case, a relevant follow-up study could enrich and expand on the current sample to include more cruise players.

A brief corporate profile of each sample cruise company now follows.

5.1. Cruise company profile

Carnival Corporation & Plc (CCL) offers cruise services under the Carnival Cruise Lines, Holland America Line, Princess Cruises, and Seabourn brand names in North America; and AIDA Cruises, Costa Cruises, Cunard, and P&O Cruises names in Europe, Australia, and Asia. Carnival runs 100 cruise ships and is a sole dominant cruise market player, as it controls a market share at 48%. This is the only cruise group with its shares traded on dual listing (S&P500 and FTSE100 indices). The company was founded in 1972 and is headquartered in Miami, Florida.

Royal Caribbean Cruises Ltd. (RCL) operates as a global cruise vacation company the cruise brands Royal Caribbean International, Celebrity Cruises, Azamara and Silversea Cruises. The firm also holds interest in TUI Cruises, Pullmantur and SkySea Cruises brands. Royal Caribbean runs 60 ships and holds a significant cruise market share at 23%. The company plans to launch 11 new cruise ships of average vessel capacity over 4500 passengers by 2025. The company was founded in 1968 and is headquartered in Miami, Florida.

Norwegian Cruise Line Holdings Ltd. (NCLH) is a global cruise company and operates the Norwegian Cruise Line, Oceania Cruises and Regent Seven Seas Cruises brands, offering itineraries to more than 490 destinations worldwide. With a combined fleet of 28 ships, and nine ships to be added by 2027 with an average capacity of 3000 passengers per vessel it holds a cruise market share at 10%. The company was founded in 2010 and is headquartered in Miami, Florida.

5.2. Revenue and profit growth

Cruise revenues exhibit consistently robust growth trends for the leading cruise players, over 2016–2019 ( Table 11 ). Contrary to most commercial shipping market segments that experienced abrupt and persistent revenue declines since the outbreak of 2008 global financial crisis, cruise shipping has seen a robust resistance and relatively rapid recovery. In 2019, Carnival recorded cruise revenue at $20.8 bln. (+10.3%, 2019/2018). Similarly, Royal Caribbean also gained robust revenues at $10.9 bln. (+15.3%, 2019/2018). Norwegian Cruise Line, on the other hand, saw comparatively modest revenue growth at $6.5 bln. (+6.6%, 2019/2018).

Cruise company revenue and profits.

EBITDA: Earnings Before Interest, Tax, Depreciation and Amortization.

Source: Authors' calculations; cruise company financial statements; www.macrotrends.net .

Gross profits exhibit an upward trend for all three cruise players, especially for the market leaders, Carnival, and Royal Caribbean. Earnings before interest, tax, depreciation, and amortization (EBITDA) is considered as a critical indicator of operational profitability and is defined as income after operating expenses have been deducted and before interest payments, taxes, depreciation, and amortization have been deducted. This profit component is to compensate subsequently for debtholder claims (interest payments), State claims (taxes) and, lastly, shareholder claims (dividends), with the latter ones perceived as residual claimants, bearing highest risk levels. The leading cruise companies exhibit modest EBITDA and Net Income shifts over 2016–2019.

According to a market motto, ‘if gross profit is not there, there will be no net profit’ as well. Gross profit margin is calculated as the ratio of gross profits to revenue. Assuming a cruise company investing in a sector that exhibits a high gross profit margin but not making bottom-line net profits may be a striking indication of a mismanaged case. Corporate restructuring and operational tuning may be required to turn the business into a profitable venture. Broadly, the level of gross profit margin depends directly on how a business is organized and the other costs it must support. For instance, after gross profit calculation, a cruise company still must pay operating expenses, financial, tax and other expenses. Subsequently, a cruise company must have robust net profits to distribute an attractive return (dividend) to shareholders. In case a cruise company can effectively control operating expenses, it can remain profitable with a lower gross margin ratio. Broadly, a higher gross profit margin is preferred, as it indicates efficient processes and offers flexibility to have money left over to spend on other business operations.