After slow end to 2022, the business travel outlook is turning more positive for 2023

There is a growing sense that lower levels of business flying are here to stay, with many still expecting top executives to set corporate flying reduction targets, driven by cost savings, changing travel habits and sustainability needs.

Messaging regarding the recovery of the business travel segment remains mixed.

Since the onset of the COVID-19 pandemic, a number of the industry's leading voices have claimed that business travel will never fully recover due to changing working habits - namely, remote working and digital nomadism; company cost reduction; and a growing awareness of environmental issues.

Indeed, international business travel has been recovering at a much slower rate than leisure tourism.

- Recovery in business travel slowed in 2H2022...but rapid recovery is expected for 2023.

- Confidence in business travel nearly fully recovered to the levels from before the COVID-19 pandemic.

- Suppliers are highly optimistic about the outlook for business travel; higher spend trend echoed by travel buyers and procurement professionals.

- Customer meetings and new business prospects to hold weight of business travel investment.

- A large part of the recovery in US business travel spending has been due to the growth of prices - such as for airfares, car rentals and accommodation.

- COVID-19 has produced a range of changes that have modified the landscape of demand for business travel globally.

- Hybrid and remote working arrangements have persisted for a large proportion of workforces globally.

- Additional layers of corporate travel approvals and duty of care arrangements introduced during the pandemic have proved stubborn to remove.

- Sustainability considerations are also weighing much more heavily on travel activity.

Recovery in business travel slowed in 2H2022...

The global recovery in business travel experienced a pause over much of 2H2022.

After a rapid bounce-back of business travel during 1H2022, the expectation had largely been that the sector would have a continued, if steady, recovery over the second half of the year. However, in the face of rising travel costs due to inflationary pressures, airline operational chaos across multiple regions, and wider concerns about the macroeconomic outlook - businesses revised their plans and travel and budgets were largely static.

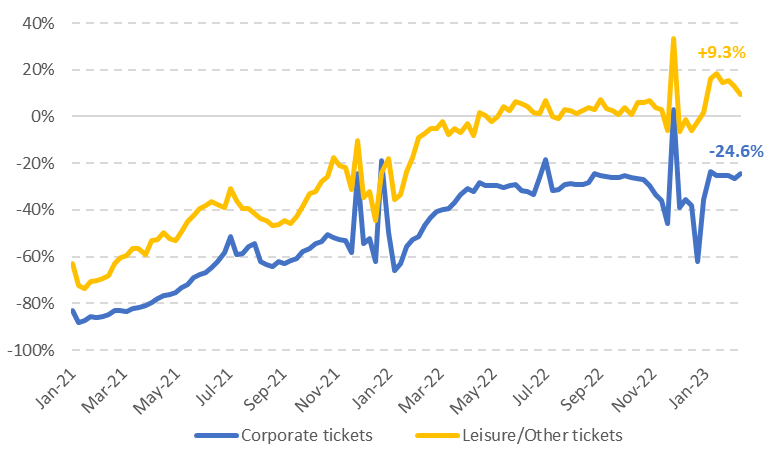

This was clearly evident when listening to comments from some of the leading airlines in the US , where business travel recovery had been strong.

In early Dec-2022 United Airlines CEO Scott Kirby stated that business travel had "plateaued" in late 2022, adding that this was "indicative of pre-recessionary behaviour". Delta Air Lines President Glen Hauenstein reported at the start of Jan-2023 that corporate travel demand had been "steady" over 4Q2022, with domestic corporate sales recovering to 80% of 4Q2019 levels.

Alaska Airlines CEO Ben Minicucci reported that large Silicon Valley technology companies had largely "turned off" business travel in late 2022.

Airlines Reporting Corporation : US corporate and leisure ticket bookings (percentage vs 2019), 2021-2023

Source: Airlines Reporting Corporation .

...but rapid recovery expected for 2023

Despite the recent slowing performance, there is an increasing undercurrent of positive expectations for business travel for 2023.

Airlines, corporate travel management organisations, travel agencies and business travel associations are now pointing to a rapid recovery for 2023, particularly when it comes to business spending.

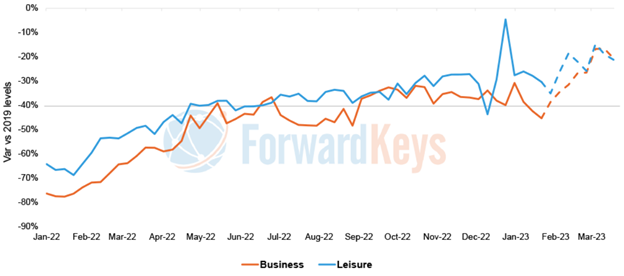

Global forward-ticketing data from Forward Keys indicates that after a slowing in business ticket sales over 2H2022, forward sales indicate that corporate air travel is due to accelerate through the early part of 2023.

ForwardKeys: forward business and leisure air ticket data, 2022-2023

Source: ForwardKeys.

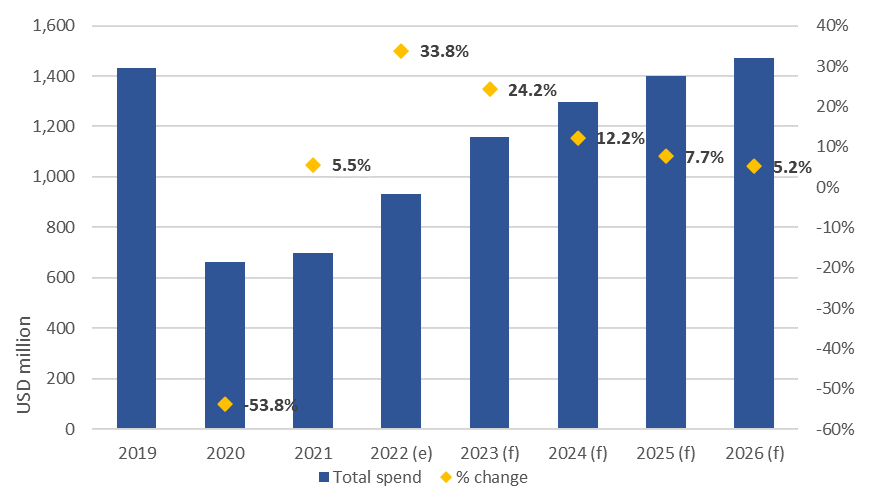

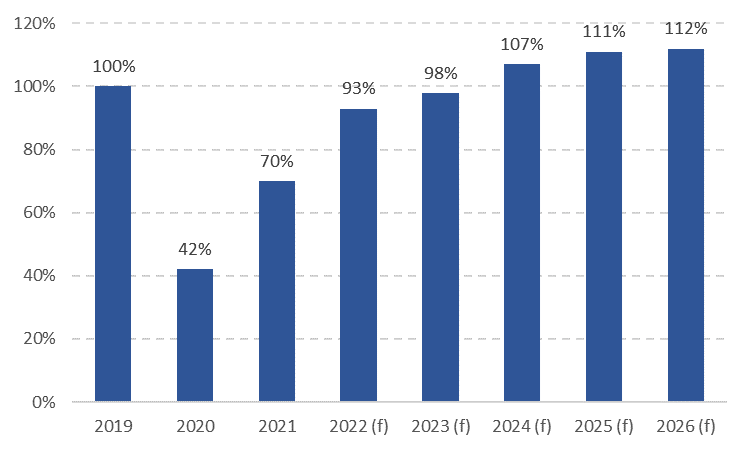

The Global Business Travel Association (GNTA) projects global business travel spending of just under USD1.2 trillion in 2023.

While this is still down, around USD273 billion down on 2019 levels (-19.1%), the outlook is for overall spending to increase 24.2% year-on-year for 2023.

GBTA : business travel spending outlook, 2019-2026

Source: Global Business Travel Association .

Confidence in business travel nearly fully recovered to levels before the pandemic

GBTA 's Business Travel Outlook Poll for 1Q2023 found expectations for business travel in 2023, with confidence nearly fully recovered to levels before the COVID pandemic.

Of travel buyers - 91% reported that they feel that employees at their company are now either 'somewhat willing' or 'very willing' to travel for work in the current environment.

This is up from just 64% of reported workers who were willing to travel in Feb-2022, and 86% in Oct-2022.

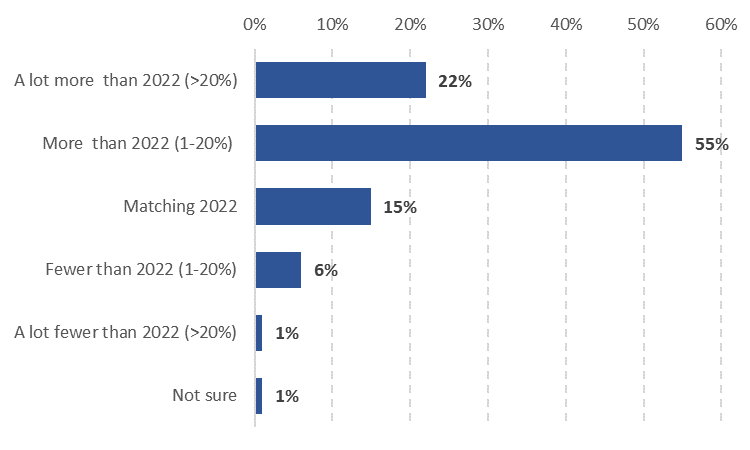

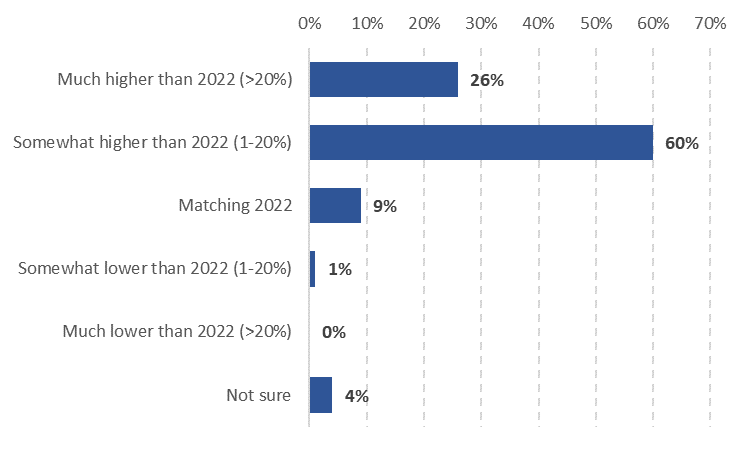

According to GBTA 's polling, 78% travel managers globally expect their companies will engage in more business travel in 2023.

Expectations about travel volumes increases are almost uniform between the North America , Latin America , Europe and the Asia Pacific regions.

Just 7% of travel managers expect reduced travel.

Reduced travel expectations are lowest with travel managers in North America (6%) and the Asia Pacific (7%), and higher with managers in Europe (10%) and Latin America (13%).

Travel buyer/procurement: professional expectations for 2023 business travel volumes

More travel suppliers expect increased spending on travel by their corporate customers

Further to this, GBTA 's data shows that 86% of travel suppliers expect spending on travel by their corporate customers will increase in 2023 - up from 80% in the association's Oct-2022 survey.

This confidence is high, regardless of region - all travel suppliers surveys in the Asia Pacific expect spending to be somewhat or much higher than it was in 2022, followed by 91% in Latin America , 90% in Europe and 85% in North America .

Just 1% expect reduced spending by corporate customers.

Travel supplier/travel management company: expectations for 2023 business travel spending

Suppliers are also highly optimistic about the outlook for business travel.

According to GBTA polling, 24% report feeling 'very optimistic' about the industry's path to recovery, and 65% are optimistic. Just 3% report they are pessimistic about the outlook.

Travel suppliers expectations about higher spend are echoed by travel buyers and procurement professionals. Of those polled, 46% expect a higher budget for travel programmes for 2023 when compared to 2022, while 41% expect budgets will be about the same as the previous year.

Customer meetings and new business prospects to hold weight of business travel investment

The key area for business travel spending in 2023 is expected to be for trips for sales staff or account managers to meet with customers or new business prospects.

On average, travel managers estimate that their companies will allocate 28% of their travel spend for these purposes in 2023. This is followed by spending on trips for internal company meetings (19%) and spending on attending conferences, trade shows and other industry events (18%).

North American business travel to return to close to normal in 2023

The US Travel Association (USTA) project that the volume of business travel by air will recover to around 98% of pre-pandemic levels in 2023, with recovery back above 100% in 2024.

Domestic travel is at or above pre-pandemic levels, but international arrivals are still in recovery mode.

For 2022, inbound arrivals by foreign nationals into the US were down 24% compared to 2109. This was chiefly due to the slow rebound of traffic from the Asia Pacific , as well as some sluggishness in the early part of the year in Europe and parts of Latin America .

As of the start of Feb-2023, arrivals from mainland China were down 97% when compared to 2019, and arrivals from Hong Kong were still down by 80%.

Inbound travel from Japan was down 41.6%, and from Australia it was down 30.4%.

From Europe , UK arrivals were down 18.5%, while arrivals from Italy were still 14.2% below pre-pandemic levels and German arrivals were down 7%. Of the main Latin American markets, arrivals from Brazil were still a third below 2019 levels.

USTA estimates for Dec-2022 were that US business travel spending would be USD97 billion, which was an increase of 3% compared to pre-pandemic levels.

US business travel forecast: volume, percentage of 2019 levels, 2019-2026

Source: US Travel Association.

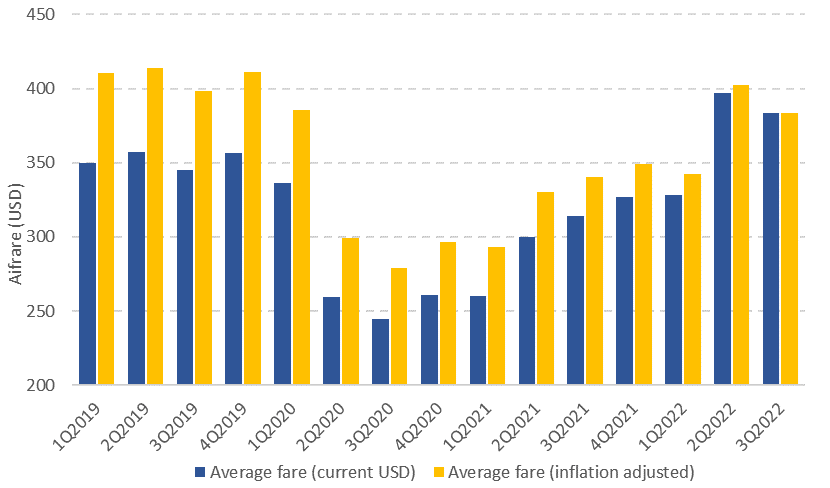

A large part of the recovery in US business travel spending has been due to the growth of prices, such as for airfares, car rentals and accommodation.

According to the USTA, airfares rose 28.5% year-on-year for the full year 2022.

US Bureau of Transport Statistics data shows US domestic fares averaged USD384 in 3Q2022. This is up from an (inflation adjusted) average domestic fare of USD279 in 3Q2020, an increase of 37.4% over the two-year period, and up 12.8% over the past 12 months.

US average domestic round trip airfares, by quarter, 1Q2019- 3Q2022

Source: US Bureau of Transportation Statistics.

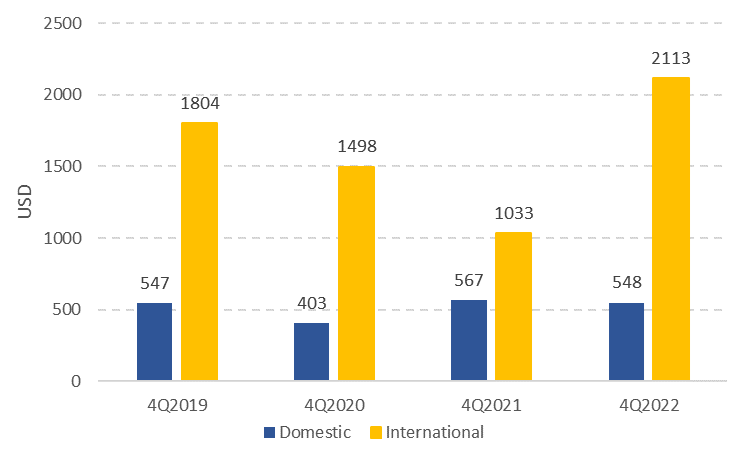

Data from the corporate travel solutions provider Emburse shows that average spend per round trip domestic business travel by air for 4Q2022 was USD548, putting it just ahead of 4Q2019 levels.

Spend per round trip on international business travel was significantly higher: USD2113 in 4Q2022, vs USD1804 in 4Q2019 (an increase of 17.1%).

Domestic and international air travel: average spend per round trip, 4Q2019-4Q2022

Source: Emburse.

New hope for full recovery in 2023

COVID-19 has produced a range of changes that have altered the landscape of demand for business travel globally - some of which have slowed the recovery, and others that are contributing to business travel coming back, albeit in modified form or with higher spending.

Hybrid and remote working arrangements have persisted for a large proportion of workforces globally, cutting into historical business travel volumes, while at the same time creating greater demand for 'bleisure' travel.

Although video conferencing technology became ubiquitous during the pandemic, enterprises continue to report strong demand for face-to-face meetings, particularly given the uncertainties in global supply chains and the need to train new staff working from remote locations.

Additional layers of corporate travel approvals and duty of care arrangements introduced during the pandemic have proved stubborn to remove - particularly in large corporations. The response has been to consolidate multiple smaller business trips into larger - and often more costly - single trips.

In this same vein, sustainability considerations are also weighing much more heavily on travel activity, but businesses have also shown greater willingness to spend money to be good corporate citizens and offset the impact of their travel.

Despite the structural trends and concerns about an economic slowdown in developed economies, business travel has renewed its upwards trend.

Although the recovery is happening more slowly than expected, and is still well below where most airlines would like it to be, there is renewed confidence in the recovery outlook for 2023.

Want More Analysis Like This?

What post-pandemic business travel looks like now

How will the pandemic and business travel recovery change corporate travel programs going forward? Are pandemic-related changes to company travel policies likely to remain permanent? Will the business travel ecosystem and travel programs in 2022 look vastly different than they did in pre-pandemic 2019?

These topics are explored in a new report released today — ”The Return to Business Travel: A New Paradigm on the Evolution of Buyers and Stakeholders Post-Covid”— from The Global Business Travel Association ( GBTA ), the world’s largest business travel association, and made possible by travel and expense technology company, Serko . Based on survey responses from U.S. and Canadian travel managers, t he study outlines how the return of business travel might look post-pandemic from the lens of corporate travel managers and especially for managed online business travel bookings.

“ Now is the moment that corporate travel managers are moving from triage and temporary solutions that may have been required to address business travel during the pandemic, to a longer range, more considered view based on new requirements—from technologies to policies to processes — that will be the basis for the next chapter and best outcomes for companies , business travelers and managed business travel programs,” said Nick Whitehead , CMO, Serko.

“When the pandemic brought almost all travel to a halt there was a recognition of the important role of business travel in helping companies grow their revenue, workforces and share prices. But as we get back to business travel, the landscape has changed. Travel managers are actively embracing evolution to determine what will be needed next,” said Suzanne Neufang, CEO, GBTA.

Here are survey highlights on what’s next for post-pandemic corporate travel management:

- TEMPORARY TIGHTENING. OR IS IT? The pandemic forced many corporate travel programs to introduce more booking policy restrictions. Seven in ten (71%) travel managers report their company’s booking-related travel policies have become stricter due to the pandemic — however, six in ten (61%) of those expect the changes to be temporary.

- UPTICK IN ASSISTED BOOKINGS . Booking business travel via an online booking tool (OBT) has declined during the pandemic, forcing a greater reliance on agent-assisted bookings. Pre-pandemic, only 9% of travel managers said their company had a “high touch” model where travelers typically made “managed” bookings directly with a travel agent. Now, one in five (20%) say their company has a high touch model.

To restore confidence in moving bookings back online, travel managers most pointed to the need for key features such as integrated destination health and safety information (85%), automatic ticket credits (77%), contextual policy applications (57%), and visually highlighted hotels that meet COVID safety protocols (53%).

- APPROVALS GO MANUAL AND MULTIPLE . In the current COVID-19 environment, travel programs not only require manual approval of business trips, but many require manual approval by multiple people. Of those that do, two in five (42%) respondents say most of their manual processing requires multiple approvers (e.g. employee’s manager and HR employee).

- REELING BOOKINGS BACK IN . Addressing leakage – i.e. business travel bookings made outside a company’s preferred channels – has become an even greater priority. Half of travel managers (46%) say reducing leakage is a “greater” or “much greater” priority than before the pandemic or equal priority (40%) today as before the pandemic. Travel managers identified OBT features that would help reduce leakage including rich airfare information and imagery and NDC-enabled bookings.

- OBT EVOLUTION . A sizeable number of travel managers are open to changing their company’s OBT in the next two to three years. Four in ten report they are likely (13%) or considering (31%) changing their company’s OBT. Key features of most interest include enhanced user experience and innovations, enhanced content, easier management, and increased traveler satisfaction.

When it comes to OBT innovation, travel managers are seeking to streamline the booking process and ensure alignment with corporate policies and goals. OBT features of most interest include personalized itinerary recommendations (78%) and conversational chatbot booking (73%) using intelligent technology (i.e., artificial intelligence) as well as insights into the environmental impact of the travel itinerary (61%).

The survey was conducted from September 20-October 3, 2021 , by GBTA with full or partial responses received from 161 corporate travel managers in the U.S. and Canada. Those respondents indicated they were involved in managing or procuring travel on behalf of their company and whose business travelers used corporate online booking tools prior to the pandemic .

GBTA members can access the complete survey report and infographic in the GBTA Hub.

About Zeno by Serko

Don’t just return to travel. Come back safer, leaner, smarter with Zeno.

As this report highlights, the way we book, manage and travel for business has fundamentally changed. There is no return to travel, only a unique opportunity to come back better.

Zeno helps travel managers seize this unique re-set opportunity to upgrade your travel program with a platform built around the priorities of the new world of travel.

Zeno is the online booking tool built for the needs of modern business travel, and we’re continuing to innovate and iterate our solution to meet the evolving needs of travel managers and their organizations; empowering you to deliver a safer, leaner and smarter travel program. www.zeno.com

Related Articles

Business travel is back, but corporate customers are more demanding than ever

GBTA welcomes European Parliament’s Inclusion of Sustainable Aviation Fuels in the Net Zero Industry Act

FREENOW and GBTA examines the evolution of ground transportation in Europe for business travel

GBTA expands presence in Asia Pacific with new advisory board

Related courses.

You might also like:

Educating Gen Z on benefits and how to do it

The shift from room-centric to guest-centric revenue management

The 3 types and the implementation of training and development

4 tips to attract and retain Gen Z employees

Hospitality workers and addiction – statistics, recovery and treatment options

Join over 60,000 industry leaders.

Receive daily leadership insights and stay ahead of the competition.

Leading solution providers:

Book Me Bob

Softbank Robotics

FCS Solutions

Eigen Payments

Advertisement

Supported by

Business Travel’s Rebound Is Being Hit by a Slowing Economy

By the early fall, domestic business travel was back up to nearly two-thirds of its prepandemic level. But companies have now begun to cut back.

- Share full article

By Jane L. Levere

Business travel came back this year more strongly than most industry analysts had predicted in the depths of the pandemic, with domestic travel rebounding by this fall to about two-thirds of the 2019 level.

But in recent weeks, it appears to have hit a new hurdle — companies tightening their spending in a slowing economy.

Henry Harteveldt, a travel industry analyst for Atmosphere Research, said that corporate travel managers have told him in the last few weeks that companies have started to ban nonessential business travel and increase the number of executives needed to approve employee trips. He said he was now predicting that corporate travel would soften slightly for the rest of the year and probably remain tepid into the first quarter of 2023.

Mr. Harteveldt also said his conversations led him to believe that business travel would “come in below the levels airline executives discussed in their third-quarter earnings calls.”

Airlines were bullish on those earnings calls, a little over a month ago. Delta Air Lines, for one, said 90 percent of its corporate accounts “expect their travel to stay the same or increase” in the fourth quarter. United Airlines, too, said its strong third-quarter results suggested “durable trends for air travel demand that are more than fully offsetting any economic headwinds.”

Hotels, too, were optimistic. Christopher J. Nassetta, president and chief executive of Hilton, said on his earnings call that overall occupancy rates had reached more than 73 percent in the third quarter, with business travel showing growing strength.

The change in mood has come as the economy has more visibly slowed. Technology companies, in particular, have been announcing significant layoffs. Housing lenders have also been reducing staff, as rising mortgage rates cut into their business.

The travel industry has long relied on business travel for both its consistency and profitability, with companies often willing to spend more than leisure travelers. When the pandemic almost completely halted business travel in 2020, people were forced to meet via teleconference, and many analysts predicted that the industry would never fully recover.

But business travel did come back. As the economy reopened, companies realized that in-person meetings serve a purpose. In a survey taken in late September by the Global Business Travel Association, a trade group, corporate travel managers estimated that their employers’ business travel volume in their home countries was back up to 63 percent of prepandemic levels, and international business travel was at 50 percent of those levels.

One reason international business travel has not come back as strongly, Mr. Harteveldt said, is that some employers have imposed restrictions on high-priced business-class airline tickets for long-haul flights. He said employers are instead requiring travelers to take a cheaper connecting flight or to fly nonstop in premium economy or regular economy class.

“Travelers are telling managers they won’t fly long-haul in economy if they have to go directly to a meeting when they arrive,” Mr. Harteveldt said.

What will business travel look like in the next year?

Pandemic travel restrictions will probably play less of a role. A survey by Tourism Economics, U.S. Travel Association and J.D. Power released in October found that 42 percent of corporate executives had policies in place restricting business travel because of the pandemic, down from 50 percent in the second quarter. Over half expected pandemic-related business travel policies to be re-evaluated in the first half of 2023.

With Americans able to work remotely, many are combining professional and leisure travel, airline and hotel executives said on recent earnings calls. That was a big reason travel did not drop off in September, when the peak vacation period ended, as it used to in years past.

Jan Freitag, national director for hospitality market analytics at CoStar Group, said hotel occupancy by business travelers currently varies by market, with occupancies high in markets like Nashville, Miami and Tampa, Fla. — places where business travelers may well be taking “bleisure” trips. But hotel occupancies by business travelers are low in markets like Minneapolis, San Francisco and Houston.

Mr. Freitag said the lower hotel occupancies in some cities may reflect a lower return-to-office rate in those places, which reduces the ability to have in-person business meetings.

Mr. Freitag said he was “very bullish on group travel, trips for meetings, association events, to build internal culture.” Those trips will recover more quickly, he predicted, than individual business travel.

“It’s all about building relationships,” he said. “It’s very hard to do that online.”

On the other hand, short business meetings and employee training sessions may continue to be conducted online, which is less expensive than in person, said Grant Caplan, president of Procurigence, a consulting firm in Houston that advises companies on their spending for business travel, meetings and events.

Even as business travel has resumed, hotels, airlines and airports still have inadequate staffing. A survey of hoteliers by the American Hotel and Lodging Association, a trade group, released in October found that 87 percent of respondents were experiencing staffing shortages. Although that was an improvement over May , when 97 percent of respondents said they were short-staffed, the current findings do not bode well for smooth hotel stays.

Disruptions in flying, particularly in the United States and Europe — because of weather delays, inadequate flight crews or air traffic control and security issues at airports — have been notoriously high, particularly earlier this year.

Although “we can’t say that these disruptions have discouraged business travel, they have clearly complicated” the experience for travelers, said Kathy Bedell, senior vice president of the Americas and affiliate program for BCD Travel, a travel management company.

Kellie Kessler, a pharmaceutical clinical researcher in Raleigh, N.C., said the travel disruptions she faced this year were too much. She changed jobs recently to take one that requires her to travel on business 10 percent of the time, compared with 80 percent in her previous position.

“The reason I took a nontravel position is that I can count on one hand the number of on-time flights I had this year,” she said.

And flight disruptions have led to a decline in some road warriors’ loyalty to airlines, even those who have accrued elite status in the carriers’ frequent-flier programs.

“The disruptions overall have caused me to be less loyal to any one airline,” said Trey Thriffiley, chief executive of QIS Aviation Group a consulting company in Savannah, Ga., that advises individuals and companies about their use of private jets. He is also an elite member of the loyalty programs at Delta, United and American Airlines. “Instead of searching by preferred airline or even cheapest price,” he said, “I search for direct flights or connecting flights to cities closest to where I live that I can drive home from if I need to.”

Airlines’ bullish forecasts notwithstanding, some experts find prospects for business travel this fall and next year extremely murky.

They say they cannot accurately predict how strong business travel will be and what airfares and hotel room rates will look like because of many unknowns, including the duration of the war in Ukraine and its impact on the European and global economies; increasing gasoline and jet fuel prices; and rising inflation, recession fears and political uncertainty.

Mr. Harteveldt, the travel industry analyst, said the recovery of business travel varies by geographic region, with the United States rebounding faster than Europe.

He said the Chinese government could be using its reopening strategy “in a geopolitical way,” adding, “If a country is more friendly, China will grant access to that country’s business and leisure travelers rather than to travelers from countries with which China has greater political differences.”

He predicted that 2023 would be a “difficult year” for business travel unless the war in Ukraine “comes to an abrupt end and there is more certainty about oil and the price of jet fuel.” Also a factor, he said, could be decisions by companies that may have added too much staff during the pandemic to save money by reducing business travel rather than by laying people off.

“If there’s a symbol that can be used to describe the outlook for business travel in 2023, it’s a question mark,” he said. “No airline, travel management company or travel manager can be 100 percent certain what 2023 will bring right now. It’s one of the most confounding, confusing times to be in business travel, perhaps in decades.”

In a report issued in August, Mike Eggleton, director of research and intelligence at BCD Travel, had a similar take on the immediate future for business travel. “Producing a credible travel pricing forecast in the current environment is incredibly difficult,” he wrote. “The near-term travel outlook is more uncertain than ever. Volatility has never been so high and seems likely to persist. There’s vast variation in market performance and outlook.”

Going forward, Ms. Bedell said, perhaps the overriding question about business travel will be whether the trip is necessary.

“Client-facing and revenue-generating travel is taking a priority over internal meetings,” she said.

Back to the future? Airline sector poised for change post-COVID-19

It’s difficult to overstate just how much the COVID-19 pandemic has devastated airlines. In 2020, industry revenues totaled $328 billion, around 40 percent of the previous year’s. In nominal terms, that’s the same as in 2000. The sector is expected to be smaller for years to come; we project traffic won’t return to 2019 levels before 2024.

Financial woes aside, the pandemic’s longer-term effects on aviation are emerging. Some of these are obvious: hygiene and safety standards will be more stringent, and digitalization will continue to transform the travel experience. Mobile apps will be used to store travelers’ vaccine certificates and COVID-19 test results.

Other effects, though, are more profound. Unlike the 2008 global financial crisis, which was purely economic and weakened spending power, COVID-19 has changed consumer behavior—and the airline sector—irrevocably.

This article will explore five fundamental shifts in the aviation industry that have arisen from the pandemic. For each of these shifts, we also issue a call to action. By responding to these shifts decisively now, carriers should be able to look beyond the pandemic and adapt to the long-term realities of COVID-19.

1. Leisure trips will fuel the recovery

Business travel will take longer to recover, and even then, we estimate it will only likely recover to around 80 percent of prepandemic levels by 2024. Remote work and other flexible working arrangements are likely to remain in some form postpandemic and people will take fewer corporate trips.

In previous crises, leisure trips or visits to friends and relatives tended to rebound first, as was the case in the United Kingdom following 9/11 and the global financial crisis (Exhibit 1). Not only did business trips take four years to return to precrisis levels after the attacks on the World Trade Center but they also had not yet recovered to pre-financial-crisis levels when COVID-19 broke out in 2020. Therefore, we expect that as the pandemic subsides, the rise in leisure trips will outpace the recovery of business travel.

Some carriers are highly dependent on business travelers—both those traveling in business class and those who book economy-class seats right before they need to travel. While leisure passengers fill up most of the seats on flights and help cover a portion of fixed costs, their overall financial contributions in net marginal terms are negligible, if not negative. Most of the profits earned on a long-haul flight are generated by a small group of high-yielding passengers, often traveling for business. But this pool of profit-generating passengers has shrunk because of the pandemic.

A McKinsey Live event on 'Returning to corporate travel: How do we get it right?'

The call: Revisit flight economics

Airlines should reevaluate the economics of their operations, especially long-haul flights. First, a smaller contribution from business traffic could necessitate a different pricing logic. For example, today most carriers price point-to-point nonstop flights at a premium. Travelers who value time over price—mostly business travelers—book these nonstop flights. Leisure travelers, even those traveling in premium classes, are more price sensitive and may choose an indirect routing. This large gap between nonstop pricing and connect pricing may need to narrow.

Second, lower business traffic may require network changes. Airlines added many flights over the past few years between hubs and smaller cities, using small-size widebodies such as the Boeing 787. These flights work because of the high-yielding business demand. With business demand subdued, economics favor larger aircraft flying less frequently. Airlines may find that larger aircraft such as Airbus A350s or Boeing 777s—which have lower unit costs—become the base of the long-haul network.

Third, airlines may also look at reconfiguring the layout of their cabins to address the increased share of leisure traffic. At the simplest level, lower business-class demand may warrant smaller business-class cabins. Taking this further, products may shift to better cater to premium-leisure passengers, such as growth of premium-economy cabins or development of business-class seats more suitable for traveling as couples or groups.

2. Staggering debt levels will lead to ticket price increases and a larger role for government in the sector

Many airlines have had to borrow huge sums of money to stay afloat and cope with high daily cash burn rates. Tapping into state-provided aid, credit lines, and bond issuances, the industry collectively amassed more than $180 billion worth of debt in 2020, 1 “COVID-19 lowers airline credit ratings and raises the cost of debt,” International Air Transport Association, August 21, 2020, iata.org. a figure equivalent to more than half of total annual revenues that year. And debt levels are still rising (Exhibit 2). Repaying these loans is made even harder by worsening credit ratings and higher financing costs.

These costs will need to be recouped. Therefore, we’ll likely see ticket prices rise. By our estimates, this could amount to a rise in ticket prices of about 3 percent, assuming a ten-year repayment window for only the additional debt taken on.

Furthermore, when demand for air travel returns, it will likely outpace supply initially. We see a glut of latent demand of people eager to travel. It will take time for airlines to restore capacity, and bottlenecks such as delays in bringing aircraft back to service and crew retraining could lead to a supply–demand gap, resulting in higher short-term prices.

In many cases, airline rescue efforts come in the form of government bailouts—with strings attached. We’re seeing a reemergence of, or increase in, the level of state ownership and influence. In Europe alone, TAP Air Portugal, Lufthansa Group, and Air Baltic all received state aid combined with an increase or reintroduction of government shareholdings.

The call: Be a constructive collaborator

As the state becomes a more active player—whether as a creditor, a direct shareholder, or as part of the board—airlines will find themselves having to deal more closely with the authorities. Instead of seeing this as a necessary restriction to access much-needed funds, airlines can treat it as an opportunity to shape how the sector evolves with a key stakeholder.

Airlines can work with regulators to set standards across a gamut of issues. These could include committing to reductions in greenhouse-gas emissions in return for more labor flexibility; increasing the cash-on-hand requirements to make airlines more resilient against future shocks; more balanced value sharing between airlines and other sectors such as airports; or changes in the ownership caps to allow greater inflows of foreign capital, reducing the reliance on state capital further down the road.

3. We will see a greater disparity of performance among airlines in the future

Some airlines have responded to the pandemic by restructuring for greater efficiency; others are merely muddling through. Occasionally, this is linked to state-aid programs, which may reduce the incentive for much-needed measures such as cost, organizational, and operational restructuring. Airlines that are not proactively transforming risk failing to set the business up for longer-term structural value creation.

As such, we’re seeing some airlines pull ahead. Before COVID-19, an airline boasted an ROIC well ahead of the overall industry’s rate of 5.8 percent. Not only did its stronger position pre-COVID-19 enable it to navigate the crisis thus far without taking on government loans of the scale relative to other airlines, it also made it possible for it to restructure to emerge with an even more competitive cost base.

Another group of carriers that have an opportunity to transform their business are airlines that have access to a restructuring process, such as Chapter 11 in the United States. These carriers can renegotiate midlife leases, shed excess debt, and emerge leaner. They will be fierce competitors going forward.

The call: Aim higher when it comes to IT and digital investment

Becoming better can necessitate investment. Even though many airlines find themselves in financial straits, we recommend investing more in IT and digitalization, not less. Before the pandemic, airlines spent roughly 5 percent of their revenue on IT. This is relatively low compared with other sectors. By means of comparison, the retail industry spends around 6 percent on average, and financial services 10 percent.

Airlines could consider stepping up IT and automation investment now. For example, airlines can respond to the quicker recovery of domestic and short-haul flights by investing in direct sales and owning the customer relationship. Relationships with IT and distribution providers could be reexplored. Carriers can also invest in the customer experience—such as making check-in and boarding processes more seamless—and support services—from revenue accounting to invoicing—to drive the next level of efficiency. Beyond this, the next horizon is analytics, which involves, among other efforts, using data in smarter ways to enhance decision making, requiring some investment but yielding significant payoffs .

4. Aircraft markets may be oversupplied for some time to come

In the years before COVID-19, aircraft OEMs ramped up production in the anticipation of continued growth. This has led to a glut in aircraft availability. Furthermore, some carriers have returned relatively new aircraft to lessors, such as Norwegian Air Shuttle when it exited the long-haul market. Prices for used-aircraft leases have plummeted and are likely to remain lower. For instance, the monthly lease rate of a 2016 vintage Boeing 777-300ER aircraft was around $1.2 million in 2019. In 2020, the rate fell to less than $800,000. New aircraft are rumored to be available at even deeper discounts.

The call: Act countercyclically now, if you can

If finances permit, carriers can consider acting countercyclically: locking in orders for new aircraft or confirming operating leases now when demand is low. Aircraft are a significant expense for an airline, making up 10 to 15 percent of a carrier’s cost base. As lease rates and OEM pricing fluctuate with supply and demand levels, inking deals during a crisis could allow carriers to enjoy a cost advantage for years to come.

5. Air freight will see undersupply for some time

Over the past ten years, low cargo rates and the unprofitability of the cargo business have led many airlines to relinquish or scale back their dedicated cargo freighter fleets. However, cargo has been a lifeline for the aviation industry during COVID-19. Before the pandemic, cargo typically made up around 12 percent of the sector’s total revenue; that percentage tripled last year. Based on data from the Airline Analyst, only 21 (down from 77 in 2019) of the airlines around the world that disclosed their operating performance achieved positive operating profits for the third quarter of 2020, traditionally the industry’s most profitable quarter. Among these 21 airlines, cargo revenue accounted for 49 percent of total revenues on average.

During the pandemic, e-commerce sales soared while many passenger flights—which are responsible for delivering around half of total air cargo—were grounded. As a result, cargo yields increased by about 30 percent last year. As commercial flights gradually return, belly supply will increase, although not to pre-COVID-19 levels for at least a few years, as the industry is expected stay smaller than before the pandemic for several years.

The call: Bring back freighters, carefully

In response to the high demand and low supply of air freight right now, carriers could investigate short- to medium-term opportunities to boost their cargo services. Airlines can enhance their flexibility through measures such as increasing the deployment of so-called preighters, or passenger airplanes that are used to transport cargo. Airlines may look at freighter conversions, especially as their passenger fleets reduce in number.

Airlines need to be agile. Rushing headlong into developing and maintaining a large freighter fleet again comes with risk. Airlines need to grow cargo in an agile way that allows for quick adjustments; pursuing such a play should be seen as part of a wider theme of establishing a more flexible production setup. High fixed costs combined with unpredictable demand levels outside an airline’s control increase the need for airlines to be able to scale down supply nimbly.

The impact of the COVID-19 pandemic is far from over. There is some relief to be found in various parts of the world now that vaccinations have begun, but the road to recovery for air traffic will take several years. The shape of the post-COVID-19 airline sector is becoming clearer and holds lessons for airlines today. Multiple longer-running trends have been accelerated, such as digitization and the phasing out of less efficient aircraft. Burdened by debt, many carriers have depleted their cash reserves. But the forecast is not without bright spots. Travel will become greener and more efficient, and people are itching to travel again for holidays. Taking steps now will help airlines thrive in this transformed sector.

Jaap Bouwer is a senior expert in McKinsey’s Amsterdam office, Steve Saxon is a partner in the Shenzhen office, and Nina Wittkamp is a partner in the Munich office.

The authors wish to thank Alex Dichter and Vik Krishnan for their contributions to this article.

This article was edited by Jason Li, a senior editor in the Shanghai office.

Explore a career with us

Related articles.

Airline data: What next beyond crisis response?

Will airline hubs recover from COVID-19?

‘Prepare for the marathon and be ready for the course to change’: An interview with the Boston Logan Airport CEO

This is the impact of COVID-19 on the travel sector

A full recovery of the global tourism sector isn't expected until 2024. Image: UNSPLASH/Eva Darron

.chakra .wef-9dduvl{margin-top:16px;margin-bottom:16px;line-height:1.388;font-size:1.25rem;}@media screen and (min-width:56.5rem){.chakra .wef-9dduvl{font-size:1.125rem;}} Explore and monitor how .chakra .wef-15eoq1r{margin-top:16px;margin-bottom:16px;line-height:1.388;font-size:1.25rem;color:#F7DB5E;}@media screen and (min-width:56.5rem){.chakra .wef-15eoq1r{font-size:1.125rem;}} COVID-19 is affecting economies, industries and global issues

.chakra .wef-1nk5u5d{margin-top:16px;margin-bottom:16px;line-height:1.388;color:#2846F8;font-size:1.25rem;}@media screen and (min-width:56.5rem){.chakra .wef-1nk5u5d{font-size:1.125rem;}} Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:.

- The tourism sector is one of the worst affected by the impacts of COVID-19.

- International arrivals have increased by just 4% in the second year of the pandemic; with 1 billion fewer arrivals when compared to pre-pandemic levels.

- 63% of experts from the World Tourism Organization (UNWTO) believe the sector won't fully recover until 2024.

While few industries have been spared by the impact of the COVID-19 pandemic, even fewer have been hit as hard as the tourism sector . As 2021 drew to a close with severe limitations to travel still in place, the World Tourism Organization (UNWTO) reported that international tourist arrivals increased by just 4 percent last year, remaining 72 percent below 2019 levels. That equates to more than 1 billion fewer international arrivals compared to pre-pandemic levels, keeping the industry at levels last seen in the late 1980s.

Prior to the coronavirus outbreak, the global tourism sector had seen almost uninterrupted growth for decades. Since 1980, the number of international arrivals skyrocketed from 277 million to nearly 1.5 billion in 2019. As our chart shows, the two largest crises of the past decades, the SARS epidemic of 2003 and the global financial crisis of 2009, were minor bumps in the road compared to the COVID-19 pandemic.

Looking ahead, most experts no longer expect a full recovery until until 2024 or later. While the UNWTO Panel of Experts is confident to see an uptick in travel activity this year, just 4 percent of the surveyed experts expect a full recovery in 2022. Roughly one third of respondents believe that international arrivals will return to pre-pandemic levels in 2023, while 63 percent think it will take even longer than that. UNWTO scenarios predict that international tourist arrivals could grow between 30 and 78 percent in 2022 compared to 2021. While that sounds like a significant improvement, it would still be more than 50 percent below pre-pandemic levels.

Have you read?

.chakra .wef-1c7l3mo{-webkit-transition:all 0.15s ease-out;transition:all 0.15s ease-out;cursor:pointer;-webkit-text-decoration:none;text-decoration:none;outline:none;color:inherit;}.chakra .wef-1c7l3mo:hover,.chakra .wef-1c7l3mo[data-hover]{-webkit-text-decoration:underline;text-decoration:underline;}.chakra .wef-1c7l3mo:focus,.chakra .wef-1c7l3mo[data-focus]{box-shadow:0 0 0 3px rgba(168,203,251,0.5);} business travel won’t be more sustainable post-covid unless companies take action, a travel boom is looming. but is the industry ready, how virtual tourism can rebuild travel for a post-pandemic world, don't miss any update on this topic.

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

The agenda .chakra .wef-n7bacu{margin-top:16px;margin-bottom:16px;line-height:1.388;font-weight:400;} weekly.

A weekly update of the most important issues driving the global agenda

.chakra .wef-1dtnjt5{display:-webkit-box;display:-webkit-flex;display:-ms-flexbox;display:flex;-webkit-align-items:center;-webkit-box-align:center;-ms-flex-align:center;align-items:center;-webkit-flex-wrap:wrap;-ms-flex-wrap:wrap;flex-wrap:wrap;} More on COVID-19 .chakra .wef-17xejub{-webkit-flex:1;-ms-flex:1;flex:1;justify-self:stretch;-webkit-align-self:stretch;-ms-flex-item-align:stretch;align-self:stretch;} .chakra .wef-nr1rr4{display:-webkit-inline-box;display:-webkit-inline-flex;display:-ms-inline-flexbox;display:inline-flex;white-space:normal;vertical-align:middle;text-transform:uppercase;font-size:0.75rem;border-radius:0.25rem;font-weight:700;-webkit-align-items:center;-webkit-box-align:center;-ms-flex-align:center;align-items:center;line-height:1.2;-webkit-letter-spacing:1.25px;-moz-letter-spacing:1.25px;-ms-letter-spacing:1.25px;letter-spacing:1.25px;background:none;padding:0px;color:#B3B3B3;-webkit-box-decoration-break:clone;box-decoration-break:clone;-webkit-box-decoration-break:clone;}@media screen and (min-width:37.5rem){.chakra .wef-nr1rr4{font-size:0.875rem;}}@media screen and (min-width:56.5rem){.chakra .wef-nr1rr4{font-size:1rem;}} See all

Winding down COVAX – lessons learnt from delivering 2 billion COVID-19 vaccinations to lower-income countries

Charlotte Edmond

January 8, 2024

Here’s what to know about the new COVID-19 Pirola variant

October 11, 2023

How the cost of living crisis affects young people around the world

Douglas Broom

August 8, 2023

From smallpox to COVID: the medical inventions that have seen off infectious diseases over the past century

Andrea Willige

May 11, 2023

COVID-19 is no longer a global health emergency. Here's what it means

Simon Nicholas Williams

May 9, 2023

New research shows the significant health harms of the pandemic

Philip Clarke, Jack Pollard and Mara Violato

April 17, 2023

For the best Oliver Wyman website experience, please upgrade your browser to IE9 or later

- Global (English)

- India (English)

- Middle East (English)

- South Africa (English)

- Brazil (Português)

- China (中文版)

- Japan (日本語)

- Southeast Asia (English)

- Belgium (English)

- France (Français)

- Germany (Deutsch)

- Italy (Italiano)

- Netherlands (English)

- Nordics (English)

- Portugal (Português)

- Spain (Español)

- Switzerland (Deutsch)

- UK And Ireland (English)

Since the start of the COVID-19 pandemic, airlines have undergone three years of non-stop change and adaptation to survive. Labor costs have been rising dramatically. Business travel has recalibrated to a post-COVID world of videoconferencing and concerns about recession, prompting a significant alteration in the passenger mix. Airline networks have transitioned to achieve more efficient operations, while accommodating a post-pandemic resurgence of leisure travel.

In short, the airline industry — particularly in the United States — has adapted swiftly and smartly to constant and unrelenting pressure. It wasn’t painless, but over the last 12 months airline agility has begun to pay off.

Oliver Wyman’s annual Airline Economic Analysis documents and quantifies the trends affecting the airline industry. While relying on the US Department of Transportation reporting and other related sources for in-depth financial and operational analysis of the US-based carriers, this year’s report also looks at global capacity along with shifts in passenger mix, especially as related to business travel, leisure and bleisure, and premium economy categories. It also explores pressures at the airport, including on-time arrivals and airport lounges.

A patch of smooth air amid turbulence

The name of the game for airlines in 2022 was once again transition. New chief executives took over at American and Southwest Airlines. Value carrier JetBlue agreed to acquire the largest ultra-low-cost carrier (ULCC), Spirit, although that merger is now being challenged in court by the US Justice Department. Airline fees and operational performance became political targets, and US airlines may face increased regulation as a result.

As airport crowds multiplied, labor in the cockpit , cabin, and on the ground remained in short supply — continuing to pressure on-time performance and schedules. Labor shortages also plagued air-traffic control, prompting the US Federal Aviation Administration to encourage airlines to limit the number of flights at peak periods in congested airports like those in New York and Washington DC.

Demand recovery and profit recovery have been uneven globally, but more steadily trending up in the US. How well individual carriers can continue to adapt to the transition will determine their success for the next year and likely beyond.

Back in the black for full-service carriers

The three US full-service carriers returned to profitability in 2022, collectively netting more than $2 billion for the full year. The turnaround took hold in the second quarter, with $4 billion in cumulative operating profits for that three-month period. These carriers repeated that performance in both the third and fourth quarters.

Delta has had the strongest recovery so far, with net earnings of $1.3 billion in 2022, compared with $737 million at United and $127 million at American. Still, even Delta’s earnings are a long way from the $4.8 billion the carrier earned in 2019.

International traffic has been a sore spot. For full-service airlines, international capacity was still down 37% from 2019 at the end of 2022. But 2023 summer schedules for international routes are building back with major increases in the number of flights available.

Value and ULCC ups and downs

Results were mixed for both value carriers and ULCCs. Like the full-service group, value airlines generated profitable operating results during the second and third quarters of 2022. For the year, Southwest and Alaska were profitable but JetBlue and Hawaiian posted net losses.

ULCCs as a group continued to post losses in 2022, with net losses at Spirit and Frontier overwhelming small annual profits at Sun Country and Allegiant. ULCCs have continued to expand capacity, despite the red ink, leveraging their cost advantage to capture additional market share.

But operating costs have been skyrocketing for ULCCs. In the third quarter of 2022, for example, ULCC carriers’ unit cost increased more than 41% compared with the same three months of 2019, even though they had added 10% more available seat miles (ASMs) during the period. While every cost category increased during that quarter, fuel took the biggest hit, rising 77% versus the same period in 2019.

It’s worth noting that the two US airlines with the largest 2022 losses — JetBlue, with a net loss of $362 million, and Spirit, with a net loss of $554 million — are looking to merge.

Hub efficiency first

Airlines have reset their networks quickly to put seats where passengers want to go. But they have done more than that. Oliver Wyman’s proprietary network forecast modeling, NetPlan , reveals that carriers are laser-focused on the efficiency of their hubs as they battle to grab more market share despite labor and aircraft shortages and reduced business travel.

Carriers are creating more itineraries per flight, while average journey times are declining. Instead of smoothing out schedules at hub airports, peaks have become more pronounced, increasing connecting opportunities even with fewer total flights.

Worldwide, the number of flights per route has declined 11%, while the number of seats per departure has increased 4%. That’s in part because airlines are providing more capacity by opting to fly larger aircraft on some routes. In 2022, total global flight volume was 18% below 2019 levels. Yet connecting demand opportunity — an indicator of how well a network generates demand for its individual flights — only dipped 4%, as measured by the number of itineraries created by the schedule per flight.

Scheduled journey time declined by 5%. Planes didn’t move faster: The dip was because passengers were able to connect more quickly to their next flight or took advantage of more non-stop service. Even while some airports have lost service altogether, the majority of airports, on average, now have more destinations with non-stop service.

Road warriors still MIA

One of the biggest challenges is the growing acceptance that business travel has changed significantly, and perhaps permanently. The rebound in corporate travel plateaued at about 70% to 80% of 2019 levels, and even airline executives who had bullishly forecast a full recovery now say that may be as good as it gets for some time to come.

The reasons are many. Lifestyles have changed with workers desiring less time away from home. Office routines have changed, with more people continuing to work from home more often. Improvements in video conferencing technology have increased the preference to conduct routine meetings virtually to save time.

A sampling of leisure-oriented airports and select business-heavy airports in Europe and North America, using Oliver Wyman’s PlaneStats data, confirms the change in the travel mix. In 2022, European leisure airports returned to the same levels of seats available in 2019, where business airports only brought back 80% of the 2019 seats. The North American leisure airports had about 10% more seats than they had in 2019, while business-heavy airports only had 90% of the 2019 seat capacity.

Willingness to pay for comfort

Premium economy seats are playing a larger role in airline offerings and seating layouts, with rising numbers of high-end leisure traveler and former road warriors opting for seat choices with more amenities. While business travel was down, the willingness to pay for more amenities allowed airlines to replace some of the revenue lost from corporate purchases of high-fare tickets.

That inclination to pay more for airfare, whether for upgrades or because of the rising cost of travel, has paid off in better yields. In the second and third quarters of 2022, the yield of full-service carriers increased more than 20% over the same 2019 quarters. Value carriers and ULCCs also saw similar double-digit yield increases in those periods.

The persistence of regional jets

The three largest US carriers — which employ approximately 45% of the global regional jet fleet — have significantly reduced regional jet capacity. The cutback is sometimes triggered by regional airline decisions to make routes more efficient and profitable by cutting flights and substituting larger aircraft so the remaining flights will have more seats to fill. More often, it is linked to the industry-wide shortage of pilots and the hiring away of regional pilots by larger carriers.

Higher fuel prices make regional service more costly, too, on a per-seat basis. When demand is high, larger airplanes become more economical. In 2022, the regional jet fleet in the US stood at 1,396 planes, down 14% from 2019 .

But cutbacks to the regional jet fleet are nothing new. As far back as 2010, large airlines started reducing the share of regional capacity in favor of mainline capacity. Analysis and modeling using Oliver Wyman’s NetPlan support an additional cutback of 7% in regional jet capacity from 2022 levels, or another 104 aircraft, to hit the optimal profit level. If a shortage of pilots or increasing pilot costs drive even further regional jet fleet reductions, airlines could potentially tolerate a 22% decline before the loss of regional capacity begins eroding airline profits. That would take the fleet down to 1,087 aircraft.

The NetPlan modeling suggests that a drop of between 7% and 22% in regional jet capacity is likely. Further reduction would depress profitability. Current order books suggest carriers could reach that level in one to four years. While this portends continued contraction, it also supports the notion that a large number of regional jets — more than 1,000 in the US — will remain economically viable for the foreseeable future.

The airport squeeze

Strain on capacity is not only being felt by airlines. Crowds of travelers have descended on many airports before they were fully staffed and prepared to handle the masses post-COVID. That’s put a strain on airport services — from food operations to maintenance staff as low unemployment, especially in the US, has made it hard to find workers.

It also hurt airport on-time performance, as measured by flights departing within 15 minutes of scheduled gate departure time. In 2022, on-time performance at Hartsfield-Jackson Atlanta International Airport — the world’s busiest — was 78% versus 83% in 2019. Meanwhile, Toronto Pearson Airport dropped to 55% in 2022 from 71% in 2019; London Heathrow fell to 55% from 75%; and Singapore dropped to 77% from 86%.

Contributing to those declining on-time numbers has been a widespread shortage of baggage handlers and other ground personnel at airports. Bottlenecks, such as delays in employee screening and badging and challenges in training, have exacerbated frontline worker shortages. Further aggravating operations has been the shift to a greater mix of leisure passengers and those who fly less frequently. Generally, they require more processing time by airline personnel because, for example, they have more baggage to check.

Long lines to the lounge

Another post-pandemic trend at airports: increased use of high-end credit cards with lounge perks, driven by bank partnerships that sustained many airlines financially through the pandemic. The rush to gain access to lounges has created long lines and a spate of social media outrage over wait time.

Airports and airlines are addressing the staffing challenges by offering higher pay and wage supplements, working with government to fast-track work permits, visas, and background checks, and even sending office personnel to the front lines. Some airports even capped the number of passengers at times because of labor shortages, forcing airlines to cancel flights.

Increased collaboration between airports, airlines, and key third-party suppliers can help lessen the impact of the labor struggles. Enhanced data sharing and planning for travel peaks can also reduce disruptions. In addition, identifying best practices and sharing them across airports can improve efficiency and ease the transition.

- Aerospace and Defense

- Harnessing Risk

- Transportation and Services

- Travel and Leisure

- Tom Stalnaker,

- Khalid Usman,

- Grant Alport,

- Andy Buchanan, and

- Aaron Taylor

Global Fleet and MRO Market Forecast 2023-2033

A ten-year forecast for the global commercial airline fleet and aftermarket.

Not Enough Aviation Mechanics

A shortfall of aviation mechanics will persist through the rest of the decade and threaten aviation's ability to grow profitably if it remains unaddressed.

Airline Economic Analysis

Oliver Wyman’s Airline Economic Analysis explores the economic fundamentals that drive airline profitability, as well as the forces that are undermining it.

Global Risks Report 2023

The Global Risks Report draws on experts, policymakers, and industry leaders to understand windows for action on serious threats and collective action.

clock This article was published more than 2 years ago

The return of ‘revenge travel’: As omicron wanes, Americans eagerly book vacations

The country is on the verge of a mini spending boom just as the federal reserve is trying to rein in inflation.

Americans are preparing to spend big — again — as omicron cases subside and states across the country loosen covid restrictions.

Travel agents, hotel operators and restaurateurs say they’ve seen dramatic spikes in demand in the past week, following a drop of more than 40 percent in daily U.S. coronavirus cases and spates of warmer weather in some parts of the country. People are booking spring break trips and summer vacations. They’re splurging on Disney vacations, private tours of Hawaii and cruises to Antarctica.

Unlike earlier in the crisis, when it seemed the pandemic would end with a celebratory boom, the reality has been more uncertain and filled with fits and starts. Many say that’s given them a sense of urgency to lock in “revenge travel” during this window of relative calm before it possibly disappears again. And though the Food and Drug Administration has delayed a decision on a vaccine for children under 5, families are holding their breath and booking anyway.

“People really want to make sure they travel while they can,” said Mark Matthews, marketing manager for Maui Seasons, a private tour company in Hawaii where bookings are up 65 percent so far this year. “Who knows when the next strain is going to come and what it’s going to look like? Everything is so unknown.”

What 4 health experts say about travel after covid-19 recovery

Pandemic patterns show that consumers rush out after each coronavirus wave, eager to splurge on flights, hotels, amusement parks and other services they had forgone.

That surge in spending was most evident last summer, when households were emboldened by a lull in coronavirus infections and widespread vaccine availability. Subsequent rebounds have been less pronounced, though economists say they still provide a notable jolt to the economy.

This time around, the expected burst of spending comes just as the Federal Reserve prepares to raise interest rates to slow inflation, fueled by consumer demand that is widely seen as unsustainable. Prices are rising at the fastest rate in 40 years, which Fed officials have said is the biggest threat to the economic expansion.

A new wave of spending could further complicate the Fed’s plans while also raising broader questions about whether restaurants, hotels and airlines — which are already struggling to find enough workers — will be able to staff up in time to meet demand. Addressing worker shortages, leisure and hospitality employers raised wages an average 14 percent last year, making it the only sector where wage growth outpaced inflation.

Economists say it remains to be seen just how sustained or widespread a spring spending boom may be. Unlike in previous reopening surges, there are no government stimulus checks or extra child tax credit payments padding Americans’ bank accounts. And while the economy continues to add jobs, wage growth has been largely eclipsed by inflation.

‘That raise meant nothing’: Inflation is wiping out pay increases for most Americans

“I do expect things to bounce back, but in a broader context, spending has already been very strong,” said Mark Zandi, chief economist at Moody’s Analytics. “Omicron dented the economy but did less damage than previous waves.”

Consumers spent heavily on furniture, cars and groceries in January, sending U.S. retail sales soaring 3.8 percent even as omicron roiled many parts of the economy. That’s on top of record holiday sales, which jumped 14 percent to $886.7 billion, according to the National Retail Federation. Now, as coronavirus cases subside, economists say Americans are likely to shift more of their spending from goods — such as electronics and exercise equipment — to services including travel and leisure.

To that end, airline bookings are rising. Hotels are filling up. And at Five Star Travel, demand for luxury cruises and European vacations has reached a fever pitch this week, according to Jay Shapiro, who owns the high-end travel agency with offices in Las Vegas, Honolulu and Fort Lauderdale, Fla.

“Clients who were sitting out the last few years — because they were old and had comorbidities — are calling now, saying ‘We’re ready to start cruising again,’” he said. “Business has picked up tremendously, just in the last day or two.”

Customers are also spending considerably more after having been cooped up for the winter, Shapiro said. And for the wealthiest, couples who may have budgeted $25,000 on a luxury vacation before the pandemic are suddenly willing to spend three or four times that, he said. A $150,000 family vacation to South Africa is no longer out of the question for some. And many summer cruises to Europe are already sold out.

“People still have the means to spend; they just needed a catalyst, and now they have one,” said Aneta Markowska, chief economist at Jefferies, who is planning a spring vacation, her first in two years, to Turks and Caicos. “They are sitting on the biggest cash cushion they’ve seen in years — and that’s not just the wealthy; it’s 80 percent of the population.”

Americans have set aside roughly $2.4 trillion in extra savings during the pandemic, in part because they’ve cut back on dining out, travel and entertainment, according to Wells Fargo. But data shows spending on those services tends to pick up rapidly as coronavirus cases subside.

Airline bookings for both domestic and international travel are on the upswing, according to Bank of America. Flight searches on the travel site Kayak have picked up in February, with interest in flights to the Philippines and Morocco more than doubling from a month ago.

Meanwhile, in Orlando, hotel bookings have almost fully returned to pre-pandemic norms in the past two weeks, according to the city’s tourism association.

“This isn’t our first rodeo. We know that the minute we get the opportunity, everybody rushes out,” said Diane Swonk, chief economist at Grant Thornton. “We are going to see quite a strong catch-up in spending as we go into spring.”

A luxury spending boom is reshaping the economy

In North Carolina’s Outer Banks, demand for beach home rentals is higher than it’s ever been, according to Alexis Lowe, marketing specialist at Carolina Designs Realty, which manages about 350 coastal rental properties.

“We’re so booked this summer that our focus is shifting to 2023,” she said. “We filled our prime weeks faster than we ever have. I’m pleasantly surprised by how confident people feel.”

That confidence, many in the industry say, has gotten a boost in the past week. With coronavirus cases on the decline, a number of states, including New York, Nevada, Rhode Island and Delaware, have dropped mask mandates, and many others have signaled that they will follow suit by the end of the month.

In Massachusetts, Gov. Charlie Baker (R) last week announced he would lift mask mandates at schools at the end of February, setting off a flurry of inquiries at the Vacationeer, a travel agency in Watertown, Mass., that specializes in Disney vacations. Owner Jonathan de Araujo says he already has twice as many trips on the books as he did in all of 2021, and expects that figure to triple by the end of the year.

“People are back at it,” he said. “With all of these states dropping mask requirements, it was like a signal that things are getting back to normal. Families are saying, ‘We haven’t traveled in two years. Let’s do it now.’”

But, he says, he’s also prepared for another round of closures and cancellations if coronavirus cases pick back up again. “There could be another spike and my customers could say, ‘I’m not traveling right now,’” he said. “If I’ve learned anything, it’s that things change.”

Traveling to Europe? What to know about requirements for 5 countries.

After canceling a long-awaited European vacation in March 2020, Jenni Solis finally booked another trip — albeit on a smaller scale. She’s planning to fly to Redwood National Park for five days in June.

“Omicron is getting better and I really need to get away,” said Solis, 47, an elementary school teacher in Los Angeles. “We need to unwind even more than we did pre-pandemic.”

But, she added, she’s still not ready to rebook her vacation to Germany, Belgium and the Netherlands just yet, in case it’s derailed by a new variant. “I don’t want to cancel a trip like that again,” she said.

Andrew Van Dam contributed to this report.

America still has the world's busiest airport

- New data on the world's busiest airports in 2023 reveals the latest trends in global travel.

- 8.5 billion passengers traveled by plane last year, almost marking a return to pre-pandemic levels.

- Airports in Asia and the Middle East became busier, but the US has once again clinched the top spot.

International travel is almost back to pre-pandemic levels, according to the just-released list of the world's busiest airports in 2023.

8.5 billion passengers traveled globally by plane last year — up from 7 billion passengers in 2022 .

The rise in air travel marks a recovery to 93.8% of levels in 2019 before the world shut down, according to preliminary data published by the Airports Council International (ACI), a trade association that includes 2,600 airports worldwide.

Increasing travel to airports in Asia and the Middle East was one of the key trends to emerge from the data, with Dubai International Airport jumping from the fifth to the second busiest airport in the world.

Airports in India, Japan, and Turkey also made it into the top 10 and were some of the biggest movers in terms of annual gains in passenger numbers.

As the world's largest domestic market for flights , US airports still make up five of the busiest airports in the world, with Hartsfield-Jackson Atlanta International Airport retaining its No. 1 position.

Despite tough global economic conditions, there was "a growing inclination towards travel," Luis Felipe de Oliveira, the ACI's world director general, said in a press release.

"Airports continue to demonstrate their resilience and adaptability amidst the challenges posed by the ever-evolving landscape of global travel," said Oliveira.

Here's a closer look at the top 10 busiest airports in the world.

10. Indira Gandhi International Airport, Delhi, India

Passengers: 72.2 million

2022 ranking: 9th

Delhi's main airport, Indira Gandhi International Airport, saw a 21.4% increase in year-on-year traffic. While it has dropped a place this year, Delhi has grown significantly as a transport hub since 2019, when it sat at number 19 in the rankings.

9. Chicago O’Hare International Airport, USA

Passengers: 73.9 million

2022 ranking: 4th

Travel through Chicago O'Hare jumped by 8.1% throughout 2023. O'Hare is a hub airport for domestic travel, particularly for United and American Airlines flights. It is also a focus city for low-cost rivals Spirit Airlines and Frontier Airlines.

8. Los Angeles International Airport, USA

Passengers: 75.1 million

2022 ranking: 6th

Travel through LAX was up 13.8% in 2023, however, compared to pre-pandemic levels in 2019, passengers at the West Coast airport decreased by 14.8% — the largest decrease of any airport in the top ten rankings. LAX is a hub for a number of carriers, including Alaska Airlines, United, American, and Delta. But domestic travel at the airport shrunk dramatically as airlines cut the number of flights following a series of meltdowns in 2022.

7. Istanbul Airport, Turkey

Passengers: 76 million

2022 ranking: 7th

Passenger numbers at Turkey's Istanbul airport have increased by 18.3%, making it the only transit hub to keep level with its previous ranking in the top 10. Notably, traffic through the airport has jumped by 45.7% since 2019.

6. Denver International Airport, USA

Passengers: 77.8 million

2022 ranking: 3rd

Denver Airport has dropped down several places on the list but still shows strong signs of growth in terms of passengers. In the last year traffic through the Colorado airport was up 12.3%, and it has also grown 12.8% from pre-pandemic levels.

5. Tokyo Haneda International Airport, Japan

Passengers: 78.7 million

2022 ranking: 16th

Japan's Tokyo Haneda Airport saw the largest increase in traffic by far, with passenger numbers surging by 55.1%. Some of that jump can be explained by a lag in tourism as Japan only reopened its borders in late 2022. Despite the jump, Tokyo Haneda is still 7.9% under its 2019 level of traffic. This January the airport made headlines after a fatal collision involving a Japan Airlines plane and a coastguard vehicle killed five people.

4. London Heathrow, UK

Passengers: 79.2 million

2022 ranking: 8th

Travel through the UK's largest airport shot up by 218% in 2022 and has once again made strong gains throughout 2023, jumping by a slightly more modest 28.5%. The airport has credited travel from the Asia-Pacific region as a major factor in its increased passenger numbers. It hopes to supersede its pre-pandemic level of traffic in 2024 and hit a record 81.4 million passengers, the airport said in a report published in December.

3. Dallas/Fort Worth International Airport, USA

Passengers: 81.8 million

2022 ranking: 2nd

Dallas/Fort Worth airport , known as DFW, is American Airlines' busiest hub and the departure city for many of the airline's international flights. Last year traffic through the airport jumped by 11.4%.

2. Dubai International Airport, UAE

Passengers: 87 million

2022 ranking: 5th

Dubai took the number 2 ranking in the list for the first time, thanks to a significant 31.7% increase in passenger numbers. Dubai's new position reflects the heavy investment that has gone into the aviation industry and boosting tourism in the region.

1. Hartsfield-Jackson Atlanta International Airport, USA

Passengers: 104.7 million

2022 ranking: 1st

Hartsfield-Jackson Atlanta International Airport comes in at No. 1 as the busiest airport in the world, a position it has held for more than two decades. In 2023, the Atlanta airport saw an 11.7% increase in passenger numbers.

Here's a look at what it takes to be an air traffic controller at the world's busiest airport.

- Main content

Russia Looks to India to Fill Tourism Void

Peden Doma Bhutia , Skift

September 28th, 2022 at 7:30 AM EDT

Tourism to Russia has taken an enormous hit since the country's invasion of Ukraine. An economy hurt by sanctions doesn't help in its pitch to travelers either. But Russia sees opportunities with India's outbound travelers.

Peden Doma Bhutia

As Russia engages in the worst fighting in Europe since World War II with Ukraine, tourism is one of the worst hit sectors for the country, especially at a time when destinations are charting their way towards recovery post the Covid crisis.

Travel to and from Russia continues to be hit by sanctions , as a result the destination is aggressively wooing travelers from what it deems as more “friendly countries” and India seems to be high on the list.

At the recently-held Outbound Travel Mart (OTM) in Mumbai, one of the largest travel trade events in India, the Russian contingent descended in full force as it made a strong bid to sell the destination to Indian travelers.

Representatives from the city of Moscow City Tourism Committee and Saint Petersburg Convention Bureau addressed the media and spoke about the “abundant tourism opportunities” that the destinations offer for Indian travelers.

Strangely, Russia, a very important tourist destination, does not have a national tourism organization with their office in India, noted Mahendra Vakharia, managing director of India-based Pathfinders Holidays.

However Vakharia noted that St. Petersburg Tourism and Moscow City Tourism Committee have individually done more than their bit since the last few months and have been aggressively engaging with the travel trade through roadshows, presentations, seminars and workshops.

Russia also plans to launch electronic visa for 52 countries , including India — a resolution that had been passed in 2020, but had been stalled due to the Covid restrictions.

What’s more, Russian President Vladimir Putin proposed a visa-free entry between Russia and India this month, during his meeting with the Indian Prime Minister Narendra Modi, on the sidelines of the Shanghai Cooperation Organisation summit in Uzbekistan.

The easing of visa regulations would certainly be an incentive, especially as the wait for visas keeps getting longer for Indian passport holders, with the waiting time for a U.S. visa appointment going up to two years.