- SMB Technology

- Mobile Productivity

- Mobile Security

- Computing & Monitors

- Memory & Storage

- Digital Signage

- Trending Tech

- Hospitality

- Manufacturing

- Transportation

- Food & Beverage

- Live Events & Sports

- Spectaculars & DOOH

- Gaming & Esports

- White Papers

- Infographics

- Assessments & Calculators

- Case Studies

- About Samsung Insights

- Our Experts

Subscribe to Insights

Get the latest insights from Samsung delivered right to your inbox.

See our Privacy Policy

Samsung Business Insights

Featured posts in

Retail Banking

5 compliance challenges for financial institutions and how to solve them

How digital tools help banks enhance employee and customer experience

How financial services can turn to tech-first solutions to support sustainability

Why branch visits are essential for a great bank experience.

As banking becomes increasingly digital, the banks that operate a combined 90,000 U.S. branches are asking: Do we still need branches? But while some see branch banking as an anachronism in the digital age, many banking experts believe a well-designed and properly staffed branch provides essential strategic value.

The financial industry has evolved tremendously to satisfy consumer banking preferences, and omnichannel strategies have given customers many choices for how and where they bank. Digital banking provides unprecedented convenience, but financial institutions must understand the nuances of customer preference.

Branches as an Engagement Tool

Contrary to expectations, branches continue to be the strongest engagement tool for banks. The importance of branches becomes clear when financial institutions understand that transaction is not the same as engagement, and that customers expect a great in-person experience for many services.

A recent Celent study shows that more than half of U.S. adults (55 percent) prefer in-person interactions with their banks when a conversation is needed and only a small minority (six percent) are looking for a fully digital banking experience. The study further shows that customers may still go to branches even when they only have a quick question.

Predictably, the study shows that customers over 60 are the most branch-centric (84 percent). More surprising, however, is the finding that younger customers, including millennials, are widely (70 percent) using bank branches and in-person interaction for substantive matters as well, including loans, financial advice and opening a new account.

Many banking experts believed that branches would disappear due to the digital nature of younger generations, considering their daily digital habits, but millennials instead appear to place high value in face-to-face consultations for important decisions such as investment portfolios, financial goal-setting, and account origination.

Creating Personalized Customer Experiences

Get your free guide to when, how and why consumers want face-to-face interaction with their banks. Download Now

Furthermore, an interesting correlation exists between branch visits and bank profits: The operations and products that normally drive higher profitability are the ones most likely to be performed at the branch. For example, 63 percent of U.S. adults have reported going to a branch for investment advice, and 52 percent have set up financial goals or a budget in a bank office.

Many of these operations are for life’s bigger moments, where customers find in-person interactions meaningful, not only because they’re dealing with large sums of money, but because they recognize the value of expert, personalized advice over algorithmic targeting. While many of these decisions may begin digitally, they’re likely to be concluded in the flesh, which makes branches — and well-prepared associates — more important than ever.

The Importance of a Hybrid Approach

Although mobile banking usage has accelerated significantly for routine transactions, it doesn’t deepen or strengthen the bank-customer relationship, because current digital channels don’t accommodate the advice-based approach that’s essential to enhance customer loyalty. Banking platforms that provide holistic advice through digital or mobile frameworks may be a natural evolution, but moving customers to digital channels as a primary engagement strategy and shutting down branches would be a risky choice for any financial institution. Research shows that digital-only customers are the least satisfied ones, while those that use a combination of physical and digital channels have the highest satisfaction rate . That means that bank branches are the key to driving engagement higher, and banks should utilize branches as relationship servicing centers in an omnichannel strategy.

The future of banking involves the successful merging of associates and technology. Branch automation benefits go beyond increasing cost savings and enhancing efficiency, to providing tools that enable associates to improve customer experience. Mobility, for example, can streamline customer decision-making processes regarding products through fast simulations and interactivity, and even enabling bank associates to serve customers remotely.

It’s undeniable that customers are adopting mobile and digital banking at a pace that the financial industry has never seen before, but the importance of making branches into technologically augmented service hubs is critical. Investments in technology and mobility shouldn’t be aimed only at cost reduction, but should address consumer experience through agility, interactivity and engaging services. Technology and mobility investments need to follow a long-term branch strategy of building a compelling in-branch sales and service experience for customers.

The math is simple: there won’t be a good digital banking journey without a physical bank branch experience.

Explore how Samsung’s banking technology improves customer engagement by mobilizing associates and automating services.

Marco Antonio Cavallo

- Bank Experience

- IT Strategy

Related Posts

How retail banks can transform through technology to win in the branch

Retail banks must turn to technology to transform the branch experience to satisfy customers who desire face-to-face interactions from their banks.

Future of mobility: Finance and banking report

Samsung surveyed 1,000 finance professionals about the future of mobile tech. Here's what they said.

HSBC improves retail bank operations with smartwatch pilot

HSBC's wearables pilot is an innovative effort to transform the retail bank experience with the Samsung Gear S3 smartwatch.

Featured Posts

Learn how Samsung's suite of mobile devices and platforms can help financial institutions handle five of their most critical compliance challenges.

Learn how one piece of mobile technology can help retail bank branch associates serve clients in a changing industry.

Financial firms can make sustainable changes by reassessing the technology and digital solutions they use.

How can we help you?

Shop special offers.

Find out about offers on the latest Samsung technology.

Speak to a solutions expert

Get expert advice from a solutions consultant.

Who are you buying for?

I'm buying for myself

I'm buying for a small business

I'm buying for a large enterprise

Our solutions architects are ready to collaborate with you to address your biggest business challenges.

- Mobile Phones

- Laptops/2-in-1

- Business Services

- Displays & Digital Signage

- Hospitality TVs

- Wireless Networks

- Public Safety

A member of our solutions architect team will be in touch with you soon.

9 Reasons Why You Still Want a Bank With Branches

Online banking has become increasingly common and popular among consumers of all ages.

According to the Federal Reserve, about half of adults in the United States used a mobile app to access their bank accounts in the past year, and that number continues to rise.

Online banks offer a lot of value and convenience.

You can manage your finances right from a website or an app, all from the comfort of your own couch.

With your bank information accessible right from your smartphone, physical bank branches might seem unnecessary or even outdated.

But before you transition to banking exclusively online, you should know there are occasions when bank branch services can come in handy .

Here are nine times when visiting a bank in person is essential:

1. You want access to a safe deposit box

Keeping important documents or valuables around your house is risky. So, if a thief breaks in or your home is damaged by a storm or fire, you could lose those essentials.

That’s why a safe deposit box can be a much better location for those items than your home.

A safe deposit box is a locked metal container in a physical branch of your local bank, behind vault doors. In return for an annual fee, you can store your valuables in the safe deposit box, protecting them from theft or damage.

Why it's so secure:

Safe deposit boxes are locked with two keys -- one that is held by you and one that is held by the bank. And, you need to sign in with a bank teller before you can access your box.

Safe deposit boxes are often more affordable than buying a safe for your home that you bolt to the floor.

Depending on the size, the cost of a safe deposit box can be quite low -- you may pay as little as $15 per year.

And, if something were to happen to you, your loved ones would be able to go to a secure, central location to get necessary documents.

2. You need to make a cash deposit

Whether you sold a couch on Craigslist or received cash as a birthday gift, dealing with paper bills can be cumbersome.

Keeping a large amount of cash in a drawer at home is risky; you could lose it or it could be stolen.

Depositing it into your bank account is safer, and you can use it to pay your bills or even invest it so your money grows over time.

The reality is:

While most online banks allow you to deposit checks through an app, depositing cash into your account is more complicated.

Some banks permit you to deposit cash through a partner ATM, but that option is limited and you may not be able to find an eligible ATM near you.

Instead, you’ll have to deposit your cash by visiting a physical branch and completing the transaction through a bank teller or through the bank’s lobby ATM.

Banks have no limits on how much cash you can deposit in person, but there are reporting rules that apply for cash deposits of $10,000 or more .

3. You need to make a large cash withdrawal

If you need to make a large purchase — such as buying a car from a private party — the seller will likely request that you pay in cash. If that’s the case, you’ll have to visit a bank in person. That’s because most banks have limits on how much money you can withdrawal from an ATM in a single day.

For example, Capital One 360 Checking customers can only take out $1,000 per day from the ATM. If you need more money than that, you’d have to spread out your withdrawals over several days. When you’re making a big purchase, timing is important, and taking multiple days to make withdrawals may not be an option.

If you visit a bank branch in person, you can withdrawal the full amount you need, without having to complete several transactions. You can get the money right away, so you can pay the seller immediately.

4. You need a notary

If you’re buying a home, making a sworn declaration, or are signing a rental agreement, you’ll need to get that document notarized.

You could visit a private notary’s office, but they can be expensive.

If you have a document that needs a notary’s stamp, most banks offer notary services in their branches.

If you’re a customer, you may not have to pay any fee at all , making it a quick and convenient option.

5. You want to exchange currency

While you can usually exchange currency at the airport, you’ll likely have to pay costly fees.

Travelex is one of the most common exchange currency companies, with over 200 locations in the United States. But if you place an order for currency through Travelex, you could pay far more than the current exchange rate, costing you money.

A cheaper option could be to visit your local bank or credit union. You can exchange foreign currency for U.S. dollars at most full-service locations.

For example, Wells Fargo allows you to exchange currency from over 100 countries. And, when you return, Wells Fargo will buy back all unused currency at any branch location in the United States.

6. You need a medallion signature guarantee

If you want to sell stocks or bonds that you hold in a physical certificate form, the process is more involved than just selling stocks online or even getting a document notarized.

Instead, you’ll need to get a medallion signature guarantee (MSG): a stamp that certifies your securities as authentic .

A medallion signature guarantee is verification that you are who you say you are, that you have ownership of the securities you want to sell or transfer, and that the guarantor institution is responsible if the signature is fraudulent.

You can’t get an MSG online or over the phone.

Instead, you generally have to make an appointment and visit a bank in person.

You’ll have to show identification, such as a driver’s license, and documentation that proves you own the stocks or bonds you want to sell.

7. You need a cashier’s check

If you’re making a large purchase or putting down a deposit on an apartment, you may be required to pay with a cashier’s check .

With a personal check, money is pulled from your own bank account. If you don’t have enough money in the bank, the transaction can’t go through, and the check will bounce.

Cashier’s checks work very differently.

With a cashier’s check, the money is withdrawn from the bank itself rather than your personal account, guaranteeing that the check is valid and that the seller gets their money.

To get a cashier’s check, you have to visit a bank in person and request one from the bank teller.

8. You want to cash in your coins

If you have a jar of coins stashed away, you can turn them into cash.

While you could go to a coin exchange kiosk at the local grocery store, they often charge hefty fees, eating away at your money.

For example, CoinStar charges an 11.99% service fee. If you cashed in $100 worth of coins, that means you’d only actually get $88.01 in cash; the rest would go toward paying Coinstar’s fee.

Instead, consider exchanging your coins for cash at a regular bank. Not all banks offer coin-counting machines , but there are some that still do. And, all will accept rolled coins as long as they’re in coin wrappers.

9. You have a major problem

If you have a major problem — such as a case of identity theft or a fraudulent check written in your name — you may not be able to easily resolve it online or even over the phone.

You may get better results by going to a branch in person and working with a bank representative.

While technology has come a long way, it’s hard to replace the value of face-to-face interaction.

If your issue is complicated or requires you to show documentation or proof, you’ll get faster results by visiting a branch.

If you do the majority of your banking online, you may not feel like a bank account with a physical branch is important.

But these are some key occasions when having a local branch can be helpful, especially in an emergency.

If you've already run into such occasions, it's worth considering an account with a bank in the neighborhood. As long as you're able to waive any monthly fees , it's a good idea to keep this account alongside your online bank accounts.

You might also like

Advertiser Disclosure:

We believe by providing tools and education we can help people optimize their finances to regain control of their future. While our articles may include or feature select companies, vendors, and products, our approach to compiling such is equitable and unbiased. The content that we create is free and independently-sourced, devoid of any paid-for promotion.

This content is not provided or commissioned by the bank advertiser. Opinions expressed here are author’s alone, not those of the bank advertiser, and have not been reviewed, approved or otherwise endorsed by the bank advertiser. This site may be compensated through the bank advertiser Affiliate Program.

MyBankTracker generates revenue through our relationships with our partners and affiliates. We may mention or include reviews of their products, at times, but it does not affect our recommendations, which are completely based on the research and work of our editorial team. We are not contractually obligated in any way to offer positive or recommendatory reviews of their services. View our list of partners.

MyBankTracker has partnered with CardRatings for our coverage of credit card products. MyBankTracker and CardRatings may receive a commission from card issuers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Research report

Banking Consumer Study: Reignite human connections

5-minute read

- Banks can strengthen fraying customer connections with life-centric solutions and better engagement across digital and physical channels.

- Most digital channels today are less than helpful in forging personal connections with customers.

- Our research reveals bank customers across generations still value branches, which they use for specific, important transactions.

- By taking steps to build more meaningful personal relationships, banks could boost revenue from primary customers by up to 20%.

Banks have a golden moment on their hands

Powerful forces, from rising rates to breakthrough technology, are converging to create an opportunity for banks to transform their relationships with customers. The revenue boost from higher interest rates may induce complacency, but forward-thinking banks can use it to ignite product innovation. Beneath the hype, advanced tech like generative AI might have enormous potential to revolutionize the customer experience.

Banks can harness these forces to explore the art of the possible and increase their relevance to set a new performance frontier. This golden moment is an opportunity for banks to redefine consumer banking in the 2020s; to play a more meaningful role in customers’ lives by understanding the forces that affect their individual lives and helping them achieve their aspirations.

RELATED: It’s 2023. Do banks still need branches?

Understanding the ever-changing customer and new competition

Accenture's latest global study of 49,000 consumers reveals crucial details about today’s banking consumers—chief among them growing customer dissatisfaction and industry fragmentation, leading consumers to seek out new providers.

of respondents rate their main bank's customer service as excellent

rate their main bank highly for its range of products and services and for the competency of its tailored financial advice

recently acquired a financial services product from a provider other than their main bank

Consumers’ relationships with their banks are becoming increasingly impersonal. The survey shows that most consumers use their bank’s digital channels for quick functional tasks only. This suggests that digital channels are functionally correct but emotionally devoid. They don’t help a bank turn a transactional relationship with a customer into a genuine human connection.

Consumers still value the branch

Our survey found that consumers across all generations and nearly all geographies still value physical bank branches in their neighborhoods. This surprising affinity for branches is clear evidence of consumers’ desire to have a personal interaction with their banks.

In addition, more than six in 10 turn to branches to solve specific and complicated problems. Pain points are set to become more acute as the economic impact of the rising cost of living sets in. As consumers navigate those challenges, they will want to have genuine conversations with their banks. Most digital channels today don't offer that.

Three pivots to reimagine the customer relationship and unlock value

Banks can respond to these trends and boost their customer relevance with three distinct but related pivots. Each helps replicate what customers appreciate about the branch: an opportunity to have a personal conversation, discuss their needs, and receive tailored advice about products and services and ways to improve their finances.

From journey to intent

Moving from a frictionless digital customer journey to understanding customers’ motivations is as rewarding as it is challenging.

Personal conversations

Deeper understanding of customers' circumstances can enable advice that’s relevant. Next-gen tech like generative AI can play a crucial role.

Holistic experiences

Banks that remove silos can offer holistic propositions that mix products—including non-banking ones—through physical and digital touchpoints.

Together these pivots can build a more human connection, activating what we call the “multiplier effect,” where banks maximize the power of their relationships to achieve top-line growth.

Read the full report for more details, including four strategic plays for success that can help banks transform their customer relationships for future relevance and growth.

A multiplier effect can help banks increase revenues from primary customers by up to 20%, depending on the market. In the US, this translates to $100B in annual retail banking revenue at stake.

Related insights

- Top 10 banking trends for 2023

- Read our life centricity playbook

Michael Abbott

Senior Managing Director – Global Banking Lead

Kim Kim Oon

Managing Director – Accenture Strategy, Banking

Future Branches EU 2022

What do today’s customers want from a bank branch.

Fact: Today’s customers (particularly millennials) are moving their banking online, and visiting local branches much less often. In the UK alone, this shift has seen nearly 6,000 branches shutting up shop since 2010 – and the story looks much the same across Europe and indeed the rest of the world.

It’s easy to understand why. Closing branches means real savings for banks, many of which are finding themselves with extensive (i.e. expensive) networks of increasingly redundant real estate. In 2017, Forbes released figures showing that setting up a new branch typically costs between USD 2 million and USD 4 million, and keeping a branch running costs between USD 200,000 and USD 400,000 per year.

Arguably then, banks would do well and save an awful lot of money by closing as many branches as possible. A sticking point remains, however – customers still want branches. Though many customers now prefer to complete everyday transactions on smartphones and banking apps, there comes a point when they feel the need to speak to a financial professional in person. Perhaps they want to start a new business, make plans for retirement, or organise a loan or mortgage. At these times, there’s simply no substitute for talking to a real person in a real bank.

This leaves us with something of a dilemma – banks can’t afford to maintain their branch networks, but they can’t afford to close them either. Customers still value their local branch, and so closing the doors on branches means closing the door on customers, too.

Clearly, a more innovative solution is required. But what will it take to keep branches relevant in the digital age, and justify their existence for banks? What is it customers want and expect from the modern bank branch?

Branch Customers Want Personal Attention and Less Friction

It’s easy to think that the shift towards online banking equates to a decrease in the importance of in-branch customer interactions. In fact, the opposite is true. The rise in digital banking actually increases the importance precisely because those in-branch customer interactions are far less frequent.

Recent research from Samsung reveals that while 77% of customers still seek out face-to-face interactions when dealing with complex financial matters, poor branch experiences make them more likely to defect to a competitor. The biggest pain points cited by customers included unprepared banking associates (68%), long wait times (55%), impersonal service (49%) and the unavailability of specialists (43%).

When a customer visits a branch, they want to be engaged, receive personal attention, and not have to wait around in order to be seen. This all comes down to branch experience. Young people in particular, have grown up using Facebook, Google, Amazon – companies which have devoted billions of dollars into creating intuitive and frictionless customer experiences. They expect the same when they visit a branch, and nothing less will do.

Branch Customers Want Digital Experiences

Most customers begin their journey online. Many will end it there, too. But for those that still prefer to come into a branch to handle certain aspects of their personal finances face to face, the digital experience can’t be left at the door.

Unfortunately, however, the retail banking experience can often leave a lot to be desired on this front. A recent McKinsey article suggested that many physical branches are “old, under-occupied, and poorly maintained.” This causes frustrations for customers when they must continuously explain to an employee who they are and what they need, when they know the bank already has this information.

Technology solutions could be used to improve customer service here. The Samsung study reveals that customers would be most excited by in-branch greeters who were prepared for their arrival with personalised information (62%), an expanded mobile app where they could check-in or compare wait times at local branches (55%), and interactive touchscreen displays to explore products and get advice while they wait (53%).

This chimes with further research from Accenture , which reveals that customers are demanding the branch goes digital – 64% said that it’s important to have devices that allow them to access their online banking in the branch, and 66% said it’s important for branches to have advanced ATM machines.

Final Thoughts

In order for the branch to remain relevant to modern customers, banks need to ensure that their physical locations are well-maintained, well-staffed, and equipped with the technology to deliver the personalised and prompt experiences today’s customers crave.

Commenting on the findings from the Samsung report, Bob Meara, Senior Analyst at Celent, sums up the situation succinctly. “These results highlight the continued premium placed on face-to-face interactions when it comes to banking, and yet as these institutions continue to modernise, they must continue to invest in delivering excellent customer service. Investments in technology and staffing must reinforce the branches’ current and future strategic role. If banks do not provide a compelling sales and service in-branch experience to customers, it may be costly.”

Return to Blog

Our Sponsors:

*Processing your payment may take a moment. Please click submit payment only once, and do not refresh this page. Doing so may result in your credit card being charged more than once.

- October 4, 2022

Close-by, Convenient & Consultative – What Consumers Want from Branches

How consumer expectation and experience are driving our next normal in branch banking .

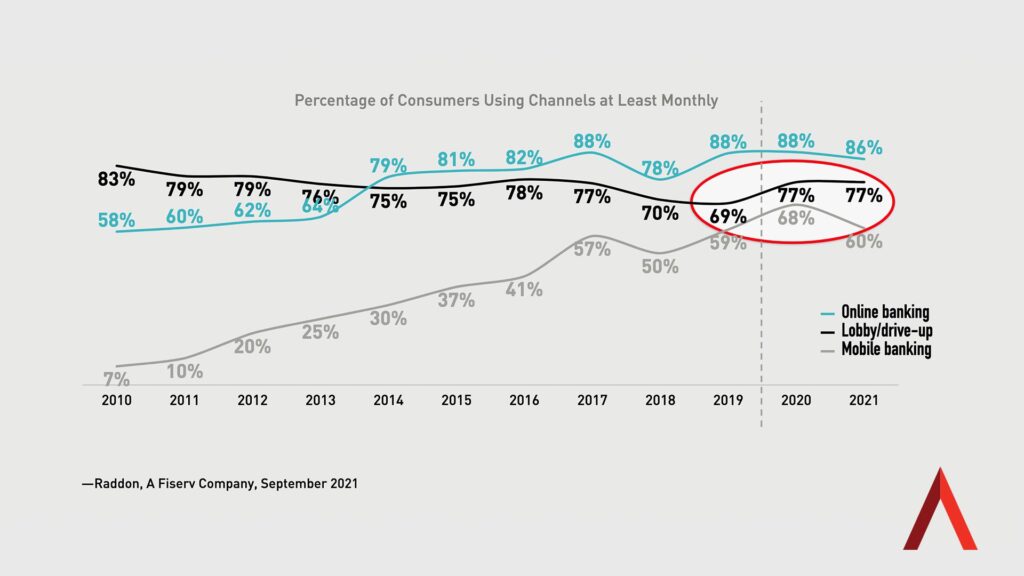

No matter where you look across financial services today, you’ll undoubtedly find news of doom and gloom about the bank branch – including warnings of widespread shuttering of locations across the country. While it’s true that banks continue key closures of branches started during COVID, consumers actually visited branches more during the pandemic, and we’re watching those levels stay steady as we transition to a post-pandemic normal. In fact, Raddon Research reports that 77% people are visiting branches at least monthly, up eight points from 2019, a rate that’s projected to remain after COVID.

Branch Banking Trends

Overall, big banks shut down the largest number of branches in 2021, with Wells Fargo, U.S. Bancorp and Bank of America leading the way in closures. Even Chase, which is known for its branch expansion plans, ranked fourth in closures. On the other hand, community banks shuttered only underperforming branches in metro markets that same year, with 84% of these community institutions not closing a single one of their branches in 2021. Even more, 56% of community banks have reported they’re augmenting their suite of services with additional products, like Wealth Management, and have plans for even more in the coming year.

Yes, an industrywide analysis of FDIC data does project a 3.5% year-over-year decline in physical branches, in tandem with a 3.65% average annual reduction in overall banks, as consolidation continues. But the latest S&P trends data finds U.S. banks are starting to slow the pace of branch network contraction. “If closure activity continued during the remainder of the year at the same pace as in the first six months of 2022, net closures would drop 19% from 2021 levels,” according to the report. This slowdown could very well mark a post-COVID rebalancing in banking, with FIs landing on the ideal mix of digital and physical channels.

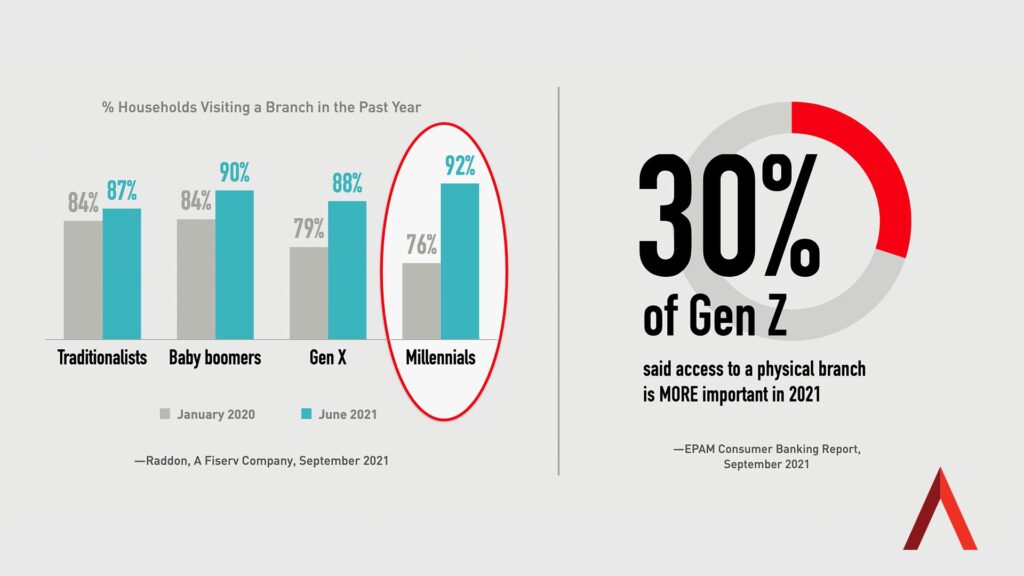

Even as branches close, Morning Consult finds 44% of consumers report they went to their local branch between 1-6 times in June of 2022 alone. For FIs, it may be tempting to assume these branch visits are coming from more traditional, older consumers, and as younger generations become the majority, those branch visits will inevitably wane. However, the reality is that Millennials and Gen Z are key demographic groups driving increases in branch visits, not decreases – with 30% of the youngest banking consumers saying that access to a branch is MORE important than it was before the pandemic.

It’s critical to note that fewer branches doesn’t mean less service. As more branches are closing, each individual branch means more to the consumer and to the financial institution, as well. That’s because what consumers see as the value of the local branch, which is – at its core – consultation and expert advice they will be more likely to act on. “The pandemic has pointed consumers back toward the branches and put pressure on institutions to offer service that is both high-tech and high-touch,” according to Raddon Research, as outlined by Juliet D’Ambrosio in the article, “ Smarter Branching for Growth .” She says, ultimately, what consumers want is “both/and: efficient transactions and valuable advice at the point of need.”

Consultation Close-By

The reality of the role branches play as part of banks’ delivery and growth strategies is highly nuanced – and compelling data points to the fact that they remain a hyper-vital delivery channel. As Insider Intelligence notes, ‘‘Contrary to the plethora of predictions proclaiming the end of the bank branch, brick-and-mortar locations remain an important component of the customer experience.” While 90% of US consumers say they’d visit a bank branch for any banking reason, Ipsos finds that 44% of all generations would be most motivated to visit a branch seeking advice, presenting banks with valuable opportunities to deepen relationships .

Further, a compelling McKinsey report presents a counter-narrative to the digital-first story we hear so often. In fact, the industry future McKinsey predicts is both physical and digital where bank branches remain an essential delivery channel – mostly because people will continue to want and need them. In fact, they note a big behavior gap, with consumers reporting they want to bank digitally, but in practice continue to visit branches. “Although willingness to open a new current account digitally hovers around 75%, only 30 to 35% of customers express an actual preference to do so digitally, and only 15% of such accounts are opened digitally.”

The Takeaway

While each financial institution will have to make decisions about market opportunity and branch performance, ultimately, serving customers – nearby, efficiently and with branch experiences they want – remains job #1 for banks. “There’s a new North Star: It’s beautiful and small ,” says Gina Bleedorn in her presentation at Future Branches . “Realistically, your full-service branches don’t need to be much more than 2,500 square feet.” And smart FIs are leveraging digital and hybrid technologies to support branch experiences, not supplant them. “Look at an enhanced drive up, a mobile branch on wheels, and an ITM only; these are a North Star strategy, extended across multiple format types and self-service technology.”

For more information on branch banking in our new normal, stay tuned to Believe in Banking’s continuing coverage of the industry’s top trends and topics. For insights on best practices in financial services, including optimizing the branch banking channel for growth, contact the banking and credit union experts at Adrenaline via email at [email protected] .

- By Lynn Medcalf

- Topics Banking Industry , Banking Trends , Branch Banking , Community Banking , Future Branches , Retail Banking

Inspiring the Future of Consumer Experiences

- August 10, 2017

- Updated on:

Why Customers are Still Using Branches

With the increasing popularity of online and mobile banking, it’s been predicted that the bank branch will soon become obsolete. And yet, there are signs that the branch will continue to be relevant but may need to offer a different role than in the past. In a 2016 North American survey by Accenture , 87% of respondents said that they would like to use a branch in the future. The most common reasons for these future visits were reported to be increased trust and value from speaking to someone in person. These insights reveal a need for human connection that is not currently being met by digital channels. Branches also seem to be preferred channels for advice and complicated financial tasks, or for consumers that have firmly ingrained habits. These reasons behind visited branches will be discussed in more detail below.

Reason #1: Human Connection & Reassurance

Interacting with someone face-to-face is a richer experience than communication through digital channels. There are more sensory cues involved, such as looking someone in the eye, watching body language, listening to tone of voice, and shaking hands. Messages through digital communication, such as email and texting, are often misinterpreted without these additional cues. It is also easier to develop a bond and relationship in-person, leading to feelings of connection, familiarity, and ultimately trust. Trust is especially important in the finance industry, since mismanagement of money is a fearful experience. So, it is understandable that banking customers may prefer face-to-face interaction at a branch more than digital channels when they are feeling uncertain and need reassurance. According to The Financial Brand , many customers report that they prefer visiting a branch to deal with problems, open a new account, or make big transactions.

Dan Geller, a Ph.D. behavioral finance scientist, reports that financial anxiety can also drive people to visit branches. “It’s not for convenience; no one is going to a branch for convenience. When the level of financial anxiety increases, people tend to make more instinctive financial decisions, rather than analytical. This, for many people, means to physically be in the place where the money is. It gives them comfort seeing the place. When people are less anxious about their finances, they are more open to doing things remotely.”

Design Tip: Branches that are designed to allow for private conversations with employees that have strong communication and interpersonal skills can ensure that this human connection and reassurance is available.

Reason #2: Help

No matter what your level of expertise in using digital channels, there often comes a point when you feel like you need a bit of help. For some people, just using online or mobile banking is too overwhelming. They may not understand how to use digital channels, lack the physical ability to navigate them, or simply not have access (or convenient access) to them. For others, it takes more complicated financial tasks to feel like they need help. Many customers have embraced digital channels for routine transactions and everyday banking tasks, but are visiting branches for complex advice. When customers do need help, it is important that there is non-digital channel in which to receive advice and education. Digital resources such as video and articles can offer information, and video-chats provide two-way communication, however in-person meetings and workshops are the most natural ways to educate and help a customer, especially those that are not as familiar with digital methods.

Design Tip: Branches that include space for educational sessions as well as well-trained staff to offer them will make them the most effective channel to offer help to customers.

Reason #3: Habit

According to a survey conducted by Bankrate in December 2015, 45% of Americans visited a branch in the past month. Some customers have developed a strong habit of visiting branches, and are resistant to changing that behavior. Branch visits may have become part of their weekly routine, or may reflect a dislike in new ways of banking and a lack of trust online services. Customers also may disagree with the rise of self-service models in many industries, from restaurants to grocery stores, and prefer full-service banking. This group of customers may be becoming more dissatisfied with banking as their local branches close and services begin to prioritize digital channels. Forcing change can result in upset customers and potential switching to other financial institutions that can better meet their needs.

Design Tip: Maintaining access to branches (even if only through kiosks or small-format builds) can meet the needs of customers that are habituated to visiting them.

These reasons of human connection and reassurance, financial help, and behavioral habits show that there is still a need for physical branches. Trust and communication are key drivers behind branch visits. Customers want to know who is handling their money, be able to discuss their concerns, and have peace of mind that everything has been done correctly. Digital channels are faceless and new, which can bring on feelings of uncertainty. They are also more one dimensional compared to in-person interaction in branches that offer complete communication experiences. It will be a challenge in the future to maintain in-person interaction as more efficient and cost-saving digital tools evolve.

Branches also have an advantage of offering immersive experiences as well as in-person interaction. If these reasons to visit and advantages are highlighted in branches of the future, they will continue to be key channels within the financial network.

Who Services Our Work Markets

Insights Connect Team Client 中文

(416) 367-1999

[email protected] +86 15618129532

Proud Member of

© 2024 Shikatani Lacroix Inc.

Industries Overview

Latest articles, republic first becomes the first fdic-insured bank failure of 2024, most teens and parents are comfortable with how much time teens spend on smartphones, social media, consumers view dynamic pricing as price gouging, what marketers need to know about the off-site retail media boom, social media marketers urge others to prepare, not panic, for tiktok ban, meta faces backlash as automated ad system drains budgets with little payoff, retailers leverage store intelligence tech to improve price planning, fintechs secure almost half of all new checking accounts, report finds, retailers lower prices amid rising inflation, google delay gives marketers more time to hone first-party data, identity resolution strategies, about emarketer, accessing a branch is ‘highly important’ to banking customers.

The data: More than a quarter of US adults rank the ability to visit a bank branch as the most important retail bank benefit, according to data collected in a May 2021 Sykes survey .

Further, 55% of respondents indicated they had visited a bank in person this year, and completed various tasks while there:

- 32.22% deposited money into their account

- 19.54% opened a new checking or savings account

- 9.19% met with a banker regarding their personal finances

Industry musings: NCR Digital Banking President Doug Brown—who was recently interviewed by PYMNTS.com CEO Karen Webster—shared his view that, “We’re in the age of the banking re-bundle, with a seismic shift in how banks envision the branch.” Brown described tech savvy, omnichannel users as significantly more profitable and valuable than digital-only customers.

The big takeaway: Customers continue to view the physical branch as a key distribution channel. To attract the kind of users Brown described, banks need a multichannel approach that incorporates important aspects of both physical and digital banking. Banks should therefore leverage technology that best optimizes the customer experience across both worlds. Here are two examples of this dynamic already playing out:

- Digital: Nearly two-thirds of US adults have either had a video call with a banker, or would like to have one. Across the pond, NatWest is already providing this feature to increase access to human bankers—even well into the evening. Users have also begun to warm up to the idea of utilizing artificial intelligence to assist with certain banking tasks: Sykes’ recent study indicated that 48.46% of US adults would feel comfortable interacting with a robot or automated system instead of a human to deposit or withdraw funds from their accounts.

- Physical: Contrary to the plethora of predictions proclaiming the end of the bank branch, brick-and-mortar locations remain an important component of the customer experience. Recognizing this, financial institutions like U.S. Bank have started to optimize their branch network to reflect changing consumer needs. The bank introduced self-service kiosks with digital devices to one of its branches, and repurposed branch employees to help with more complex services, such as technology assistance, lines of credit, and wealth management.

Industries →

Advertising & marketing.

- Social Media

- Content Marketing

- Email Marketing

- Browse All →

- Value-Based Care

- Digital Therapeutics

- Online Pharmacy

Ecommerce & Retail

- Ecommerce Sales

- Retail Sales

- Social Commerce

- Connected Devices

- Artificial Intelligence (AI)

Financial Services

- Wealth Management

More Industries

- Real Estate

- Customer Experience

- Small Business (SMB)

Geographies

- Asia-Pacific

- Central & Eastern Europe

- Latin America

- Middle East & Africa

- North America

- Western Europe

- Data Partnerships

Media Services

- Advertising & Sponsorship Opportunities

Free Content

- Newsletters

Contact Us →

Worldwide hq.

One Liberty Plaza 9th Floor New York, NY 10006 1-800-405-0844

Sales Inquiries

1-800-405-0844 [email protected]

- Commercial Insights

- Philanthropic Solutions

- Wealth Insights

- Online Banking Login

- Regions Total Wealth

- Investment Account Access

- Open an Account

- En Español

3 Good Reasons to Visit a Bank Branch

Content Type: Article

Sure, online banking is convenient, but physical branches serve an important role.

Pop quiz: With the popularity of online and mobile banking, plus omnipresent ATMs, who goes into physical bank branches anymore? A lot of people, it turns out.

Why? Getting cash via checks or ATMs is the main reason for most branch visits, says David B. Sherrill, SVP of Customer Experience at Regions. But it’s not all about cash. “In-person connections can provide peace of mind about one’s finances as well as important insights,” he says, “which are especially valuable in turbulent economic times.”

After all, when dealing with in-depth processes like mortgage applications or financial planning, you’ll receive more personalized advice and support from a face-to-face meeting than an online chatbot. Plus, there are still functions that only a branch can handle.

Here’s why you should consider making bank branch visits part of your routine.

1. Unique Functions

For some banking needs, there’s simply no substitute for being there in person.

- Large cash withdrawals or transfers. Banks have daily limits for how much you can withdraw from an ATM (for Regions personal check cards, the daily limit is $808) or transfer online. To move or withdraw larger sums, you’ll have to show up in person.

- Notaries publics. Getting a document physically stamped means, of course, physically going into a branch. Check to make sure your branch has a notary on staff; you may also need an appointment.

- Safe deposit boxes. While these super secure havens for physical property may not be as prevalent as they once were , accessing them (or renting one) requires a visit.

2. Speedier Transactions

Sure, you can take care of these activities online, but who has time to wait around for the official paperwork to arrive in the mail?

- Cashier’s checks. Order a cashier’s check online, and the bank still has to mail it to you. A teller can cut you one immediately.

- Account openings. Apply online for a checking or savings account, and the approval could take days. In person, most banks let you open one right away.

3. Personal Meetings

Some banks provide more holistic advice that could help align your finances for the future.

Regions, for example, offers personalized Greenprint plans. The process begins with a structured interview in which a banker or advisor will discuss your financial goals, concerns and needs (and perhaps help you uncover some you might not know you had). With a complete picture of present assets and future goals, Regions will then help you build a customized plan to follow and revisit whenever the need arises (say, when there is a change in your life). Kicking off the process could be the beginning of a relationship with a trusted financial professional that can pay dividends in the near future as well as down the road.

So, while mobile banking may be convenient, don’t dismiss the branch. “Most people won’t need an in-person visit for many kinds of transactions,” says Sherrill. “But physical branches still provide a lot of value—they aren’t going away anytime soon.”

Three Things to Do

- Read more about Greenprint plans and make an appointment today at a branch near you.

- Find a Regions branch near you with our locator tool .

- Want to open a new account but can’t make it to a branch? See what options you have online .

Related Insights

Related Calculators

Content Type: Calculator

Label: Home Equity

Label: Budget

Looking for More?

- Open a Checking Account

- Find the Right Savings Account

- Send Money with Zelle®

- Learn about Home Mortgage Options

- Bank Anywhere, Anytime with Digital Banking

- Learn about Mobile Deposit

- Get a Regions Visa® debit card

- Get the Regions Now Card®, a Reloadable Visa® Prepaid Card

- Make an Appointment Today

- Marketplace

- Marketplace Morning Report

- Marketplace Tech

- Make Me Smart

- This is Uncomfortable

- The Uncertain Hour

- How We Survive

- Financially Inclined

- Million Bazillion

- Marketplace Minute®

- Corner Office from Marketplace

- Latest Stories

- Collections

- Smart Speaker Skills

- Corrections

- Ethics Policy

- Submissions

- Individuals

- Corporate Sponsorship

- Foundations

Why is there still a need for physical bank branches?

Share now on:.

- https://www.marketplace.org/2021/11/18/why-is-there-still-a-need-for-physical-bank-branches/ COPY THE LINK

Get the Podcast

- Amazon Music

This is just one of the stories from our “I’ve Always Wondered” series, where we tackle all of your questions about the world of business, no matter how big or small. Ever wondered if recycling is worth it ? Or how store brands stack up against name brands? Check out more from the series here .

Listener Paul Jones from South Portland, Maine, asked:

So much banking can be done online so why are there 40 credit unions and 30 banks in my area? Each year, large shiny brand new branches are opened.

You can now deposit a check, transfer cash and pay your bills with the convenience of a click.

Yet, despite the rise of online banking, physical banks still retain a presence in some communities. There are still many people (especially those who skew older) who aren’t used to managing their finances electronically, while some of the services that banks provide still require face-to-face interaction, according to Jaime Peters, assistant dean and assistant professor of finance at Maryville University of St. Louis.

“Additionally, we’re still a fairly large cash society, and you have to have a branch, especially if you’re a small business, and you’re dealing with cash in and cash out,” Peters said.

In 2020, there were almost 75,000 branches in the U.S., compared to about 85,600 in 2009, according to data from the Federal Deposit Insurance Corporation.

But like Jones from South Portland pointed out, some areas still have plenty of banks and credit unions, and some are even planning to expand.

American Banker, reporting on data from the National Credit Union Administration, said that at the end of September 2020, 745 credit unions had plans to add branches or expand facilities, and that there were a total of 21,000 credit union branches in the U.S.

Paul Legutko, senior principal at the financial-services advisory firm Aité-Novarica, said many financial institutions don’t want to close their branches because they think being embedded in the local community is “a selling point.”

Legutko said cases where banks have tried to enter a market exclusively digitally (i.e. increasing the amount they spend on digital marketing in a certain area) tend to have mixed results. He thinks this is because having a financial center, where you can go to resolve any issues, provides comfort to consumers.

“These are stressful times,” Legutko said. “If I’m applying for a mortgage, I don’t want to just leave that to an online application.”

Legutko said a study Aité-Novarica conducted last year found that 9 out of 10 consumers say having a branch nearby is important to them, even though only 3 out of 10 go to the branch.

Reynold Byers, a clinical professor of supply chain management at Arizona State University, said handling one’s finances can get confusing, which is why having a person step in to explain the process can be helpful.

“A lot of times if you try to find a way to get a good explanation of some detailed or complex loan or account, it’s hard to find that information on the website or the mobile app,” Byers said.

You’ll typically find physical bank branches near shopping areas or industrial areas, explained Peters. (Although Peters noted the ones in industrial areas are more on the decline.) And when it comes to credit unions, Peters said those are typically in places near the employers that are sponsoring them.

Some banks, like Capital One, have attempted to reinvent the concept of the bank to lure customers. Starting in 2015, the bank mixed credit cards with coffee by launching a series of cafés , some of which are still open.

And earlier this year, Citigroup Inc. Chief Executive Jane Fraser said the company was planning to add more branches in the U.S., while Chase announced in October that it’s already opened more than 220 branches since it announced an expansion plan back in 2018. By the end of 2022, Chase is aiming to open 400 new branches.

Byers said banks like Chase are opening up in places where they don’t have an established presence.

While banks may be ubiquitous in some areas, not everyone has access to one.

“You’ve got certain communities where you’ve got lots and lots of banks, and then you have other communities where there are no banks,” Legutko said, noting that these tend to be rural, lower-socioeconomic or underrepresented areas.

The unbanked rate for Black households in 2019 was 13.8% and 12.2% for Latinx households vs. 2.5% for white households, Marketplace reported last year.

Byers said that in banking deserts, consumers are often left to using less certain and more expensive financial services, like payday loans.

Experts agree that going forward, having physical banking in some form is necessary.

Elisabeth Honka, an associate professor of marketing at the University of California, Los Angeles, said that not only do some financial services need to be handled in-person, but there are areas where the internet infrastructure they have is not particularly robust.

“So online banking is not quite working out for consumers,” she said.

And Peters said she thinks physical banking will continue to have a role in the banking system for many years to come.

“There’s still some comfort when you’re talking about something so sensitive as your own money, that you are seeing the person face-to-face, that you feel like you know your banker,” Peters said.

Tell us what you’ve always wondered:

Stories You Might Like

Why does Citibank want to open more branches in the age of online banking?

USPS pilots a public banking program

What do bank branches offer in an online-banking world?

If money doesn’t grow on trees, then why do banks have “branches”?

House approves cannabis banking bill

How will banking change amid wreckage of SVB, First Republic?

There’s a lot happening in the world. Through it all, Marketplace is here for you.

You rely on Marketplace to break down the world’s events and tell you how it affects you in a fact-based, approachable way. We rely on your financial support to keep making that possible.

Your donation today powers the independent journalism that you rely on . For just $5/month, you can help sustain Marketplace so we can keep reporting on the things that matter to you.

Also Included in

- Banking industry

Latest Episodes From Our Shows

Climate change is the focus in shared curriculum for business schools

CHIPS funds are heading to Phoenix, “ground zero for the new economy”

Student protestors have a long history of demanding financial divestment

Could the Fed cut interest rates based on this week's economic data?

10 Incentives to Drive In-Person Visits to Your Local Bank Branch

As customers increasingly performing routine bank transactions online—from depositing checks to opening accounts—relationships between individuals and their local bank branches aren’t as strong or prevalent as they used to be. With decreased customer engagement comes decreased loyalty. Customers may find it easier to switch banks, choose advertised deals for loans or accounts at competing local or national banks, or simply neglect to take advantage of financial products like CDs or IRAs that not only increase deposits, but also help them build wealth and attain long-term financial stability.

A successful method for banks to combat customer disengagement and boost retention is to improve in-person connections. As a small, community bank , you already have a leg up over national banks in providing a convenient, local experience for your customers. In this post, we’ll discuss ways to use this to your advantage, building upon your strengths by utilizing simple steps to increase visitors to local bank branches, and ultimately create loyal and lifelong customer-bank relationships.

Why do banks need to incentivize customers to visit local branches?

Many community-owned banks strive to keep up with their national counterparts by offering competitive and digital banking features—and these features are important to giving customers what they want and need. In fact, more than two-thirds of Americans use digital banking, with numbers expected to continue to rise. However, that doesn’t mean that those digital customers will never visit a branch.

Bringing customers to their local bank branch for in-person interactions can help solidify your banking relationship and help them come to see you as a financial partner rather than a hands-off utility. Not only will creating one-on-one relationships with your customers encourage retention, it can also help you acquire new customers who are not pleased with their current bank, or who are currently unbanked (about 4.5% of US households ) and aren’t sure where to start.

When you provide a thoughtful, useful, or reassuring customer experience, you show your customers the value of banking with a local financial institution—one that is accessible beyond 800-numbers and chatbots. And there are some banking activities that your customers may prefer to do face-to-face, from making special deposits to applying for a home loan.

Additionally, a quality in-person experience can also set you apart from other local banks in appealing to individuals who prefer to do their banking in person or as a hybrid of in-person and online, like customers under the age of 35 . As Deloitte Center of Financial Services explains in a recent banking and capital outlooks report , “Digital interfaces are essential, and desired, but customers tend to need person-to-person experiences to boost loyalty.”

Smart Ways to Increase Local Branch Visits

In past years when most banking was completed through onsite transactions, banks didn’t need to create incentives to increase local branch visits. However, with the rise of digital banking, customers sometimes forget the benefits of the occasional visit to their local branch. Here are ten ways to bring both new and current customers into your bank branches, connect with members of your team, and build beneficial long-term customer relationships.

1. In-person exclusive offers: One of the best ways to encourage visits is to offer special promotions to customers who visit the bank in person. Examples of such promotions could include:

Cash-back offers: Consider offering cash-back to customers who visit their bank branch regularly. You can reserve cash-back for specific transactions, such as making deposits or opening a new account. Or you can offer cash back for completing a set number of monthly or seasonal visits.

Giveaways. From local guides to tickets to area sporting events and gift baskets, giveaways can help boost visits as well as your customer’s experience. Consider teaming up with local businesses to increase publicity and reduce overhead costs (more ideas on community partnerships below). Offer free coffee and tea at certain times of the day or on certain days of the week.

Swag. From water bottles to t-shirts, merchandise affiliated with your bank can increase brand awareness in the community, while also incentivizing bank visits. Raffle a swag bag each month or offer individual items to the first ten visitors of the day.

Special interest rates on loans or CDs. Offering a special rate for in-person applications or account openings can not only pull in new customers, but it can also help you make a connection to them and jumpstart a long-term banking relationship.

Passport programs. For adults or children, offer a passport program with rewards for customers who visit all or a set number of branches within a period of time (for instance, over the summer).

Children’s books. Give out free financial-literacy related books for children of various ages (Like the classic The Berenstain Bears and The Trouble with Money ) when they open an account or make a deposit in person. Take this a step further and create a children’s reading section in your lobby or hold a regular story hour by a team member or member of the community. You might even consider creating a dedicated space in-branch for a financial literacy library.

Feature a local business or artist. Provide space in-branch to a local business who can sell products. You could also allow local artists to display their artwork for sale inside of the branch.

Free coin counting machine. Allow both customers and non-customers the opportunity to use a coin counting machine to convert coins into cash. Give them a free gift for depositing the coins into an account!

Convenience services. Retailers are increasingly offering various convenience services to entice foot traffic, including Amazon Pickup Lockers, FedEx/UPS package dropoffs, Laundry and dryclean lockers, and more.

2. Personalized customer service opportunities: Advertise one-on-one meetings with financial advisors, lenders, or other bankers to discuss financial goals and options. Personal meetings can give you quality face-to-face time with your customers, as well as providing them with information about the tools your bank can offer for their greater financial wellbeing. Consider creating an easy online request form to book these appointments.

3. Convenience and comfort: Make your customers’ branch visits as convenient and enjoyable as possible for customers by taking steps to provide efficient service and short wait times, as well as comfortable waiting areas with free Wi-Fi, refreshments, and activities or treats for small children. Additionally, make efforts for customers to feel at ease, especially when dealing with difficult financial circumstances. Promote empathy, when possible, and provide employee incentives to provide a reassuring and warm environment for all customers.

4. Financial education: Hold onsite workshops, trainings, or courses on financial management, wealth creation, tax strategies, and innovative investment ideas. Financial education can help customers stay engaged and remain informed in their financial management. Advertise refreshments or personal follow-ups or appointments as a further incentive to customers to these events.

5. Community events: Offer free meeting space to nonprofits and local companies, or host specific community events at the bank branch to increase visibility and engagement within your community. Events could include charity drives, networking events, and fun activities like trivia or game nights, cookouts, coin collector meetups with rare coin appraisals, and more. You can also consider something as simple as displaying local artwork and holding an opening event or special exhibition kickoff day with refreshments each time you display a new artist.

6. Community business partnerships: Partner with local businesses to offer discounts on local eateries or retailers, or exclusive offers for customers who use the bank’s services. If your branch is near a local cafe or ice cream shop, work together to offer coupons for a free cone or cup of coffee.

7. Children and teen bank tours. Involving children and teens in your incentives can solidify your relationships with the whole family and encourage lifelong banking relationships. A bank tour that includes a look at the vault, operating the pneumatic drive-thru tubes, and watching the coin-counting machine in action can be a fun experience for children and parents alike, and cement an impressionable mind’s enthusiasm for managing money. Include a coloring book or storybook for younger children. For teens and young adults expand this to education on common financial steps for their age, like opening a checking/savings account, using an ATM, or basic and accessible information about the smart use of credit.

8. Unique branch experiences: Think about what your community represents and what your customer-base would appreciate the most (or ask your customers directly!) and model your branch on these ideas. Consider what amenities (like coffee or tea) your customers would enjoy. Incorporate a children’s play area or a lounge area where customers can relax before an appointment or work between errands. Include local art, maps, or historical displays. The key is to make customers feel welcome to come in and linger.

9. In-branch tech solutions: Provide customers with interactive tools and technology that they can use when they visit your branches. Options could include a kiosk that allows customers to explore various mortgage payment options, or an augmented reality experience that allows people to visualize their financial goals.

10. Digital presence for your locations. Many customers and prospects will first look at your digital presence before visiting your branches. Local search engine optimization will enhance your digital presence for each location, including local listings on online platforms (e.g., Google Maps details, images, and reviews). It can also be useful to create online search ads with location extensions, which can provide users with a clickable link to online maps which provide driving directions.

Lastly, it’s important to make sure that your bank’s website facilitates and encourages in-person visits. Advertise branch events and incentives. And be sure to create a dedicated page on your website for each branch that includes information about each branch’s location and amenities, as well as images of your building and team members, and other special characteristics.

Let Your Digital Presence Be a Bridge to Strong, In-Person Banking Relationships

As a locally owned and operated financial institution, you know your community and how to best relate to and serve your customers. While you work hard to create a robust digital experience, it’s important that you don’t let online capabilities entirely replace those important, one-on-one banking relationships. Using your online presence to not only simplify banking needs but encourage in-person involvement can help foster strong connections, loyal ties, and sound long-term financial choices that can give your whole community a boost.

Many bank websites serve as a wall between their team members and their customers—rather than a bridge to all the personal services and benefits their bank has to offer. Whether it’s creating informative location pages or improving your Google listings, BankBound’s digital marketing services can help your financial institution increase those connections and build partnerships with both new and existing customers. Contact us to see what we can do for you.

How do you do it?

Does your bank or credit union use a novel approach to increase local bank branch visits? Reach out to us to tell us about your community bank marketing ideas! Have you used one of the tips above and seen the impact at your branch? We’d love to share your success with our readers in this post!

- Everest Fleet Management

- Protect Your Investment

- RDC Help Desk

- MICR & OCR Codeline Reading

- Intelligent Scanning

- Fingerprint Verification

- Multi-functionality & Hybrid

- Branch Transformation

- Check Imaging (Branch)

- Remote Deposit Capture

- Document Verification

- Customer Authentication

- Property Management

- Post Offices

- Company Overview

- Management Team

- Values & Careers

- White Papers

- Case Studies

- search Find a Reseller

- description Product Inquiry

- help_outline General Inquiry

- Driver Policy and Open Source

- Warranty Registration

- Warranty & Maintenance Terms Scanners

- Warranty & Maintenance Terms BioCred

- RMA – Repair Ticket

- Order Supplies

- Contact Tech Support

- EN – Global

Four Reasons why you should visit your Branch

Home / Blog / Four Reasons why you should visit your Branch

With the rise of COVID-19 in 2020, many people stopped visiting banks in person altogether, leading to the closure of 9% of branches in developed markets in 2021 alone.

While it is hard to imagine a world without your local bank, mobile banking has remained popular well beyond the shelter-in-place mandates. With so much of what we do moving and remaining online, the future of the branches we love and trust seems grim – but is it really?

Let’s take a closer look at the top four reasons why you may want to put down your smartphone and negotiate your hard-earned money in person.

People trust banks because they are government-accredited institutions . Your bank has licenses and safeguards to protect your money, should you choose to hold it there. You can go there in person at any time to take out cash from an ATM, open a savings account, or dispute a charge on your account. So long as you arrive during opening hours on appropriate business days, there will be someone who can provide you with what you need , or at least point you in the right direction.

When the 2008 financial crisis hit, customers rushed to the in-person bank to resolve issues with Northern Rock in the UK, even though mobile banking existed and was an available option. Though the internet did not exist in the late 1920s, odds are that even if it had, banking clients would still have found themselves rushing to the physical buildings to find out where their money had gone when the stock market crashed.

We trust banks the same way we make sure our friend gets home safely or we hold the door open when someone else is coming into a building behind us – it is second nature.

Advice from a Human

While AI and search engines offer all the information presently available on a topic, this much information can overwhelm and prevent you from accessing the pieces you really need. Unlike Google or a thread on Reddit, a visit to your bank branch offers specialized knowledge from an expert on the subject.

With over 10 different types of personal loans and 28 mortgage variables available in the current market, it is easy to see why conferring with another human with insider knowledge is an invaluable resource. Their wisdom will save you time and research, which you can spend planning what color to paint the walls of your new home after you get approved.

Convenience

Though banking online would seem to be more convenient than going into a branch, many have had the deeply frustrating experience of consulting with an AI customer service representative, resisting the urge to cry out, “A human, please! I would like to talk to a human!”

Working smarter does not always mean a better customer experience . While online banking has its moments of convenience, miscommunication occurs more readily.

Imagine if someone stole your credit card or gained access to your account: you would not want to be trying to explain yourself to an automated system when experiencing stress and panic. When it comes to your money, it can save you a headache to handle matters face to face .

A Phygital journey

We are seeing the rise of the phygital experience post-pandemic , defined as the merging of the physical and the digital worlds.

While the latter is fertile ground for all businesses right now, the hybrid experiences being generated by major retailers and department stores indicate that there’s something about walking into a store or a business that most of the human population still greatly enjoys.

Banks are leaning towards this style of marketing as well , and if you stay home and glued to your mobile banking account, you may miss out on the opportunity to enjoy some of these immersive digital-meets-physical experiences.

Today, we have the pleasure of getting to know Irene Amasio, Production and Purchasing Specialist at our offices in Turin. Irene, young but already with a significant wealth of experiences, shares her passion for China and a part of her professional journey at Panini.

In today's data-driven world, identity theft has become a pervasive threat. In particular, an insidious form of identity theft that is rapidly gaining ground, called Synthetic Identity Fraud. So, what is it exactly and why should you be aware of it?

Let's meet Becky and Sheila, our amazing office coordinators. What's their secret? Let's find out!

Search for:

BAI gives financial services leaders the confidence to make smart business decisions, every day.

- Board of Directors

- In the News

- Advertising & Sponsorship

Trusted, Accurate & Relevant Online Training Courses for Banks & Financial Institutions

- Compliance Courseware

- Professional Development Courseware

- Professional Skills Library

- Leadership Innovation Library

- Board of Directors Insight Series

- BAI Learning Manager

- BAI Career Pathing

- BAI Training Insights

- BAI Documents & Resources

- System Requirements

- Regulatory Resources

- Quick and Easy Setup

- Focused Processes

- Powerful Communication Tools

- Credit Unions

- Mortgage Lenders

- Customer Benefits

- Tailored Solutions

- Terms of Service

Real Data, Real Insights, Real Results

- Business Banking

- Consumer Banking

- Digital Banking

- Talent Management

- Banking Trends by BAI Banking Outlook

- Small Business Reporting from BQ and BAI

Your trusted source for actionable insights and groundbreaking ideas.

- Compliance, Regulation & Risk

- Customer Experience

- DEI & ESG

- Fraud Prevention

- Marketing & Sales

- Talent & Workforce Management

- Infographic

- Roundtables

- Learning Manager Login

Is the bank branch’s reality virtual?

Proponents say the metaverse is revolutionary. For banks, this might include transactional, retail and gaming VR experiences with a few familiar aspects of traditional branches.

This article first appeared in the March BAI Executive Report. Gain more insights into the value of modern branches as part of omnichannel strategies in that issue, BAI Executive Report: Evolution of Banking Branches .

Imagine going to the bank, but not walking into a physical branch. It might sound impossible, but in banking virtual reality (VR) has the potential to reshape the industry’s long-held traditions and norms.

While still in its nascent stages, VR and other immersive realities—augmented and mixed realities—have the potential to revolutionize how customers interact with banks, offering experiences that transcend traditional banking services.

And yet some VR features harken back to the brick-and-mortar days, such as connecting banking and shopping experiences with an elevator reminiscent of department stores, or pedestrian friendly town centers. VR is an as-yet mostly experimental format that presents opportunities for enhanced customer engagement, personalized financial education and innovative product demonstrations.

To be sure, there are some things that technology can’t outright replace, such as the classic safe deposit box.

To learn more about these transformational beginnings, BAI talked with Teresa Silva Sousa , Portugal-based Banco BPI’s head of innovation and new business, about how the storied industry is being reshaped.

Banco BPI , part of CaixaBank S.A., earned a spot as a finalist in the 2023 BAI Global Innovation Awards for the early inclusion of its banking app, including a VR banking branch, on Meta’s devices.

Some answers have been edited for clarity and length.

BAI: Talk to us about VR in banking. Where are we with this?

Silva Sousa: VR in banking represents a promising frontier in the financial industry that might become a channel of contact with clients and, so, should be explored. However, widespread adoption is still underway, with challenges such as technological limitations, regulatory considerations and customer acceptance needing to be addressed. Nonetheless, as technology continues to evolve and consumer preferences shift, VR holds the promise of reshaping the banking landscape in profound ways, and we, as a bank, want to be ready.

Who is the target customer, and how do they use it?

The target customer of banking in VR comprises individuals seeking innovative and immersive banking experiences, particularly those interested in exploring new technologies and digital solutions.

Banking in the metaverse caters to a diverse audience, including tech-savvy consumers and digital natives who, in the future, will also be met by those seeking convenience and flexibility in their banking interactions. These target customers use BPI VR and banking in the metaverse to access financial services, engage with interactive content, explore virtual banking environments and participate in educational, sporting and recreational activities.

Users access the elevator just off the lobby in Banco BPI’s VR bank branch. Services can be found throughout the bank’s many virtual floors. Credit: Banco BPI

What role does the metaverse play?

The metaverse can be understood as the convergence of immersive realities, such as VR and augmented reality (AR), with virtual worlds (like Fortnite or Roblox) and the principles of Web 3.0, encompassing blockchain and digital assets. No one knows 100% what the metaverse encompasses, but it will likely be a sort of digital universe where users can interact with each other and with digital content in real time, blurring the lines between physical and digital experiences. It increasingly offers a seamless and interconnected digital environment where people can work, play, socialize and transact, opening up new opportunities for businesses and individuals alike.