4 Best Long-Term Travel Insurance in 2024 (w/ Prices)

Home | Travel | 4 Best Long-Term Travel Insurance in 2024 (w/ Prices)

When traveling abroad, get a policy from one of the best travel insurance companies . Y ou can get a 5% discount on Heymondo , the only insurance that pays medical bills upfront for you, HERE!

Planning on taking an extended trip soon? Long-term travel insurance is the perfect choice for travelers who are embarking on a long-term trip and need medical- and travel-related coverage.

Of course, insurance for long-term travel isn’t necessary for every traveler, particularly if you don’t take trips that are longer than three months. However, long-stay travel insurance is useful for anyone who is studying abroad, working abroad temporarily, taking a gap year, or simply traveling for a long period of time.

When I first moved to the US, I wasn’t sure if I would stay permanently, so I purchased a long-term travel insurance policy from Heymondo , knowing that it would save me money and give me coverage if I experienced any medical emergencies. It was exactly what I needed at the time.

5% OFF your travel insurance

As soon as I decided to live in the US permanently, I switched to insurance with more medical coverage beyond emergency situations since extended-trip travel insurance is not suitable for expats who want routine medical care.

If extended-stay travel insurance is what you need, keep reading, because we have compared the best long-term travel insurance plans (Heymondo, World Nomads, Travelex, and SafetyWing) and can help you choose which of these is best for your trip.

What is long-term travel insurance?

Long-stay travel insurance coverage comparison

- Long-stay travel insurance price comparison

- Best long-term travel insurance companies

Long-term travel insurance is insurance for anyone taking a long-term trip who needs medical expenses and trip-related coverage. Any trip that lasts a minimum of 90 days and a maximum of one or two years (depending on the long stay travel insurance company) is considered a long-term trip.

Like other travel insurance, insurance for long-term travel provides medical- and travel-related coverage for incidents like emergency medical care, trip delays, baggage loss, and repatriation. It is not suitable, however, for anyone who is permanently living abroad, especially because it only covers emergency medical expenses and not routine medical care.

Long-term travel insurance vs. annual, multi-trip travel insurance

So, is long-trip travel insurance the same thing as annual, multi-trip travel insurance ? They might sound similar, but actually, insurance for long-term travel and annual travel insurance is completely different.

Long-term travel insurance is insurance for long trips that last three months or more, while annual travel insurance covers multiple shorter trips that happen within one year. With annual travel insurance, trips are restricted to 30-90 days, so it’s not a useful option if your trip will last any longer than that. Annual travel insurance is also only helpful if you’ll be taking at least four or more trips a year.

If you are going on a single, long-term trip or are taking multiple trips within a year that will last longer than 90 days, long-stay travel insurance is the best choice for you.

Who is insurance for long-term travel for?

There are several reasons you might need insurance for long-term travel . You might be taking an extended trip, working abroad, embarking on a gap year, or more. Below are the most common and useful reasons for buying travel insurance for long-term travel :

Extended stay travel insurance for long trips

If you’re about to take a long trip that will last at least three months, you will definitely want to have travel insurance coverage, particularly for emergency medical expenses.

Long-term travel insurance will work out to be the most affordable option for your trip, especially if you don’t plan on returning to your home country before 90 days have elapsed. If you plan on going back home before 90 days have passed, then annual, multi-trip travel insurance might be more helpful for you.

Long stay travel insurance for working abroad

Are you about to be working from another country for an extended but temporary period? Having travel insurance for working overseas is a must, as it’s very possible that you’ll need emergency medical care at some point during your time abroad.

Remember to put your country of residence as your home country, not the country you will be working in temporarily. Otherwise, you will not be covered since long-term travel insurance usually does not provide coverage in your designated country of residence.

Travel insurance for expats

Although it may seem like a great idea to use long-term travel insurance as travel insurance when moving abroad , long-stay travel insurance is not intended for expats. Long-stay travel insurance only covers emergency medical expenses, so it’s not suitable for someone who lives abroad permanently and will need routine medical care and check-ups.

On top of that, whatever country you move to will now be your country of residence. Insurance for long-term travel does not generally provide coverage in your designated country of residence, so you may not be eligible for coverage anyway.

Long-stay travel insurance for students

It’s incredibly exciting to study abroad, but accidents and mishaps can and do happen, so avoid paying for emergency medical expenses and replacing stolen valuables with your own money by getting extended-stay travel insurance .

Having long-term travel insurance coverage will be especially useful if you plan on taking weekend trips to other countries that are close to the country where you are studying abroad; you can still receive the same coverage for those smaller trips (just make sure to select worldwide coverage or, if you’ll just be traveling in Europe, Europe/EU coverage).

Round-the-world trip insurance

Taking a long-term trip around the world is many people’s dream. If you are lucky enough to get to live out that dream, it’s easy to make sure your extended-stay travel insurance worldwide will cover you everywhere you want to visit.

Just make sure you select “worldwide” or “around the world” coverage when you purchase your extended-trip travel insurance . That way, you won’t have to buy individual long-term travel insurance policies for each country you visit. Best of all, you’ll be covered for any spontaneous stops you make while traveling the world.

One-way travel insurance, the best gap year travel insurance

If you’re planning on spending a full year traveling the world, travel insurance for long trips abroad is exactly what you need. You’ll benefit from worldwide emergency medical coverage, so you can receive treatment if you get injured or fall ill, as well as travel-related coverage for baggage loss and trip delays.

I recommend purchasing a one-way travel insurance plan from Heymondo or SafetyWing since both companies allow you to renew your plan from month to month. That way, if you end up coming home unexpectedly early, you won’t lose out on any money.

Insurance for digital nomads

ith so many jobs transitioning to working from home right now, it’s easier than ever to work remotely from anywhere in the world. If you have the opportunity to travel the world while working, take it, but make sure you purchase digital nomad travel insurance before you leave.

You’ll want your insurance coverage to include electronics (laptop, tablet, etc.) so that you can easily replace these crucial pieces of technology for working remotely if they get lost or stolen. Additionally, if you’ll be trying to check a lot of places off your travel bucket list, choose worldwide coverage so that you’ll have the freedom and insurance coverage to go wherever you want.

There can be many considerations to keep in mind when purchasing long-term travel insurance , but coverage is certainly the most important aspect to consider when selecting the long-stay travel insurance you want to buy.

Below, you’ll find a long-stay travel insurance comparison that shows you the differences in coverage among the Heymondo, World Nomads, Travelex, and SafetyWing plans.

Long-term travel insurance price comparison

If you want a better idea of how much long-term travel insurance costs based on the length of your trip and/or the specific coverage you choose, below is a chart comparing the prices of 1-month, 3-month, 6-month, 8-month, and 1-year long-term travel insurance as well as the prices of long-stay travel insurance, annual multi-trip travel insurance, and cancellation insurance.

The price of long-term travel insurance will be impacted by several different factors, including your age, nationality, and state of residence (if you live in the US).

To give you an idea of how much insurance for long-term travel costs, I’ve used the example of a 30-year-old American citizen who lives in Pennsylvania and needs worldwide coverage to generate quotes for this long-stay travel insurance price comparison .

Best long-term travel insurance

As you can see from the charts above, each of the four long-term travel insurance plans I compared has its merits.

Heymondo offers the highest emergency medical expense coverage, plus it’s the only insurance for long-term travel that pays your medical expenses upfront, so you don’t need to file a claim after your trip to get reimbursed. I will say, however, that it’s not the cheapest long-haul travel insurance and it does have a deductible of $100 for emergency medical expenses. Still, I do think it is the best long-term travel medical insurance if you want ease and convenience.

SafetyWing ’s Nomad Insurance also provides very good coverage, but their deductible for emergency medical expenses is $250. In spite of this slight drawback, SafetyWing stands out as the best insurance for digital nomads since you can sign up for a plan and it will automatically be renewed every four weeks.

Travelex , on the other hand, has the cheapest travel insurance for long-term travel (for trips of six months or more). For shorter trips, there are other, cheaper options. Travelex’s plan has no deductible, but its emergency medical coverage is also very limited, so I would think twice before going on a long-term trip with such a small amount of coverage.

Last but not least, World Nomads offers the best gap year travel insurance. The emergency medical expense coverage is perhaps a little low, but it is at least higher than Travelex’s medical coverage. There is no deductible for medical expenses, but you will need to pay out of pocket and then file a claim to get reimbursed if you receive emergency medical treatment.

As you can see, the best long-stay travel insurance for you will depend on your needs and type of trip, so keep reading to learn more about each plan.

1. Heymondo , the best long-term travel medical insurance

Personally, I consider Heymondo the best long-term travel medical insurance since its Top plan provides the highest amount of emergency medical expenses and evacuation and repatriation coverage. It’s also one of the only types of travel insurance with COVID coverage that covers COVID testing required by a doctor. Moreover, you can easily extend your plan by anything from two weeks to eight months whenever you want to.

Best of all, you won’t have to worry about waiting to get reimbursed for medical expenses since Heymondo pays your medical expenses directly and upfront for you, removing the hassle of the claim-filing process. Heymondo also makes it easy to tailor your insurance for long-term travel to fit your needs since you can add optional electronic and/or adventure sports coverage to your plan.

Heymondo’s Top plan does have its limitations, though. There is a $100 deductible for medical expenses, which means you’ll have to pay $100 towards any medical bills before Heymondo pays the rest for you. This long-stay travel insurance also lacks trip cancellation coverage; you will need to buy that coverage independently here.

If you want cheap long-term travel insurance , Heymondo is ideal; its plans already provide very good value for the money, plus you can save an extra 5% on their insurance with the discount link below.

Heymondo is also the best travel insurance company for single trips. We currently have their travel insurance and have used their assistance app more than once. Heymondo has always been there to help us when things go wrong during our trips.

2. World Nomads , the best gap year travel insurance

If you’re taking a gap year, you’re probably interested in breaking out of your comfort zone and having a real adventure. In that case, World Nomads is the perfect travel insurance for living abroad for a year and trying new things.

Its Standard plan includes adventure sports and activities coverage, so you can try everything from trekking and ice fishing to hockey and horseback riding and still be covered for accidents and injuries. Moreover, you’ll benefit from solid overall coverage for emergency medical expenses, evacuation and repatriation, trip cancellation, trip delay, and baggage loss.

Even better, there’s a $0 deductible for medical expenses, so you won’t have to pay a cent out of pocket toward your medical bills. However, World Nomads’ long-term travel insurance is the most expensive out of all the ones I compared, so if you want to save a lot of money and get similar or better coverage, Heymondo may work better for you.

3. Travelex , the best travel insurance for long-term travel

Travelex ’s Travel Select long-trip travel insurance has a lower amount of emergency medical coverage than the other insurance plans I have compared, and I personally wouldn’t feel protected traveling with such a low amount of medical coverage on a long-stay trip. However, Travelex is a viable option if you’re traveling on a budget for more than six months because it’s really cheap (and has a $0 deductible for medical expenses)!

Travel-related coverage is another story since Travelex has the highest amount of trip cancellation and trip delay coverage of all the plans I compared. It’s the best plan to choose if you anticipate experiencing any travel mishaps. You’ll also enjoy great baggage loss and evacuation and repatriation coverage.

If you would rather benefit from more medical coverage for a similar price, Heymondo is the best choice for you.

4. SafetyWing , the best insurance for digital nomads

SafetyWing ’s Nomad Insurance lives up to its name by being the best insurance for digital nomads . Not only is Nomad Insurance a cheap long-stay travel insurance , but it also provides a high amount of medical-related and baggage loss coverage.

On top of that, you can choose to have your insurance renew itself automatically every 28 days. Automatic renewal will save you time and money; ensure you don’t forget to renew so you’re always covered; and provide you with more flexibility if you haven’t decided when to end your trip yet. Just select a start date (but not an end date) when you buy Nomad Insurance and keep renewing until you want to go home, at which time you can select an end date.

Nothing’s perfect, however, and unfortunately, SafetyWing’s Nomad Insurance is no exception. There’s a $250 deductible for medical expenses, which means you’ll have to pay $250 out of pocket for medical treatment before SafetyWing will cover medical expenses for you.

SafetyWing also lacks trip cancellation coverage, which can be very useful if you have to cancel a trip due to weather, illness, injury, or many other reasons. If you want a lower deductible, go with Heymondo instead, and if trip cancellation coverage is important to you, choose World Nomads or Travelex .

What does long-term travel insurance cover?

The best travel insurance for long-term travel will usually include the following types of coverage:

- Emergency medical expenses : This is probably the most important type of coverage as well as the coverage you are most likely to need while traveling. Accidents, injuries, and illnesses can happen at any time, so having emergency medical expense coverage will ensure that you don’t have to pay out of pocket for hospitalization or medical transportation.

- Evacuation and repatriation : Hopefully, you’ll never have to use evacuation and repatriation coverage, but it is useful to have. Insurance for long-term travel with evacuation and repatriation coverage will pay for the transportation costs of taking you from a remote area to the nearest hospital or sending you back to your home country if you fall seriously ill or have an accident.

- Trip delay : Unfortunately, travel does not always go smoothly; your flight could be delayed due to inclement weather or an airline issue. If that does happen, long-stay travel insurance ’s trip delay coverage will cover expenses, such as meals and accommodation, that are incurred because of a several-hour delay.

- Baggage loss : Even when you take precautions to keep your belongings safe, there’s still a chance an airline could lose or damage your bags, or a pickpocket could take your purse. In any case, long-term travel insurance with baggage loss coverage will reimburse you for any valuables that are lost or damaged, so you won’t have to replace them with your own money.

Is long-term travel insurance worth it?

Ultimately, yes, long-term travel insurance is worth it for extended trips, working abroad temporarily, and taking a gap year. It’s also a great alternative for international student insurance . In all of these situations, insurance for long-term travel will ensure that you get the medical- and travel-related coverage you need without having to break the bank.

As you’ve seen in the long-term travel insurance comparison chart above, Heymondo is the best long-stay travel insurance in terms of medical coverage. It offers the highest amount of emergency medical expense and evacuation and repatriation coverage.

Heymondo’s extended-stay travel insurance also provides the convenient flexibility of being able to renew your policy for periods from two weeks to eight months, which is perfect if you haven’t yet decided when you’ll end your trip. To top it all off, you can even get 5% off their insurance just for being a Capture the Atlas reader.

If you’ll be traveling for more than six months and you’re looking for the cheapest long-stay travel insurance, then Travelex may be better for you. Just be aware of their plan’s lower amount of medical coverage.

If you have any questions about long-term travel insurance, feel free to comment below and I will happily help you out!

Don't miss a 5% discount on your HeyMondo travel insurance

and the only one that pays all your medical bills upfront for you!

Ascen Aynat

22 replies on “ 4 Best Long-Term Travel Insurance in 2024 (w/ Prices) ”

Hi Ascen, we are US citizens and plan to spend about 6 months of the year in California and 6 months abroad. We have lived in California and in the past had insurance with our jobs which will now be no more. So the question is when we are are in California what is our insurance option so we can visit doctors, dentists etc. Thank you

Hi Sonu, you need standard health insurance for California and travel insurance for traveling out of the States. Travel insurance won’t cover routinary medical appointments.

Let me know if you have any questions, Ascen

Good day. Could I get overlapping coverages to address different issues? Does any of these cover rental car collision insurance during any portion of the stay? If not, what do you recommend for that?

Yes, you can hire different travel insurance to get different coverages. That is no problem.

Hi my husband was diagnosed with mestatic melonma in 2021, Weve been traveling back and forth to Moffitt overvs year now. Weve paid out over $7000 just in lodging. Do you have a plan for this??

I’m sorry about that but there is no insurance that can cover that. That is not an unforeseen issue that occurred during a trip that is mostly what travel insurance cover.

Hi There is an age limit on Heymondo 49+ not included. I am 60. Can you recommend any long stay travel insurance for this age group? Thanks Karan

Hi Karan, I recommend checking our article on senior travel insurance for the best options for you.

Hi! Do you know if you need basic medical coverage from your home country before purchasing any of these insurance plans presented above? My situation is a bit complex. I am a Canadian citizen currently living abroad (non-resident of Canada), therefore I have no basic Canadian health coverage. I am currently covered by the country I reside in (Qatar), however, once I leave, I will no longer have a residency permit and therefore no coverage here either. So when I leave, I won’t have coverage anywhere. I am planning on leaving to travel for a year, so I need long-term travel and medical coverage.

Hi Marisas, please take into account that these long-term travel insurance are travel insurance. That means that they don’t cover routine health checks or chronic diseases. They only cover you under unforeseen problems. For example, if you hire one of these long-term travel insurance and have a car accident during a trip and need surgery, the travel insurance will cover but it won’t cover cancer treatment, for example.

Hi can you recommend a travel insurance for a 7 month European trip for wife and self age 59 CA residents- many thanks

Please check the coverage for the insurance recommended in this article and choose the one that is best for you.

Hi Were planning to travel continuously for one year to Europe, Asia & med cruise. Is there a travel insurance that can cover this? Most insurances will require you to go back to your home country (US) after 60 to 90 days. Thanks

Hi Nate, I don’t believe you need to get back to the US with the Heymondo Long-Term Travel Insurance. Have you checked it out?

Hi Ascen We are a male 57years and female 58 years and we are travelling to south Africa to include Botswana Namibia Mozambique,Angola Zambia and Lesotho, we are shipping our car from Australia into south africa and will be travelling for two years we both hold Australian and UK passports Could you please recommend a medical insurance for this trip , we are not to bothered about trip cancellation baggage etc any help would be appreciated We have used world nomads previously but would consider others as well Thank you ag and rg

Hi Antony, that trip sounds amazing! If you’re doing a long-term trip like that one, I recommend Heymondo since they pay all medical expenses in advance. Just be aware of the 100$ deductible per claim.

Said that their price is very competitive and they have very high coverage.

Looking for long term insurance for cancel for any reason plus Covid coverage.

I recommend purchasing separately a long term travel insurance with Covid Coverage (I recommend this one ), and a cancel for any reason policy.

Interesting that this features Travelex and then notes: “Can get similar or better coverage for a more affordable price” From whom?

As you can see in the different comparison charts (coverage comparison chart and price comparison chart), Travelex is the one with the lower coverage, by far, and it’s only worth checking for 6-month insurance or more.

Let me know if you have any questions,

Hi! Do you know if you need basic medical coverage from your home country before purchasing any of these insurance plans presented above? My situation is a bit complex. I am a Canadian citizen currently living abroad (non-resident of Canada), therefore I have no basic Canadian health coverage. I am currently covered by the country I reside in (Qatar), however, once I leave, I will no longer have a residency permit and therefore no coverage here either. So when I leave, I won’t have coverage anywhere. I am planning on leaving to travel for a year, so I need long-term travel and medical coverage. Thanks!

Hi Melanie, no you don’t need it. You will need just long-term travel insurance and you will be covered wherever you go. Also in your home country as long that you’re traveling there and use the insurance just for emergencies (not regular checks, ongoing problems, chronic diseases, and things like that). In your situation, I think the long-term travel insurance of MONDO is your best bet.

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

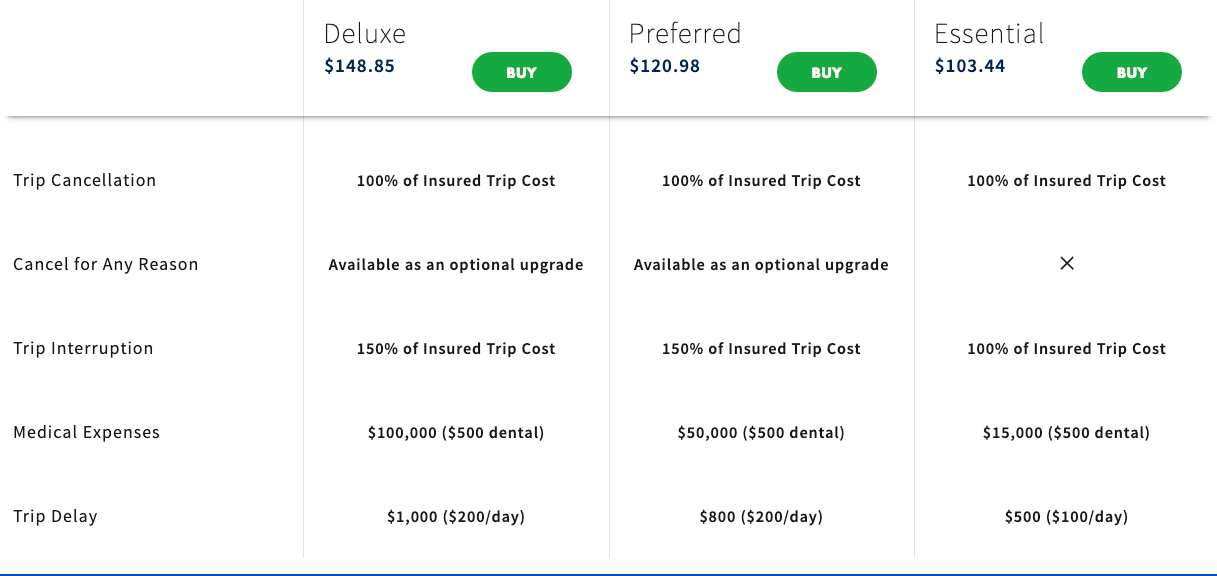

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

Allianz Travel Insurance

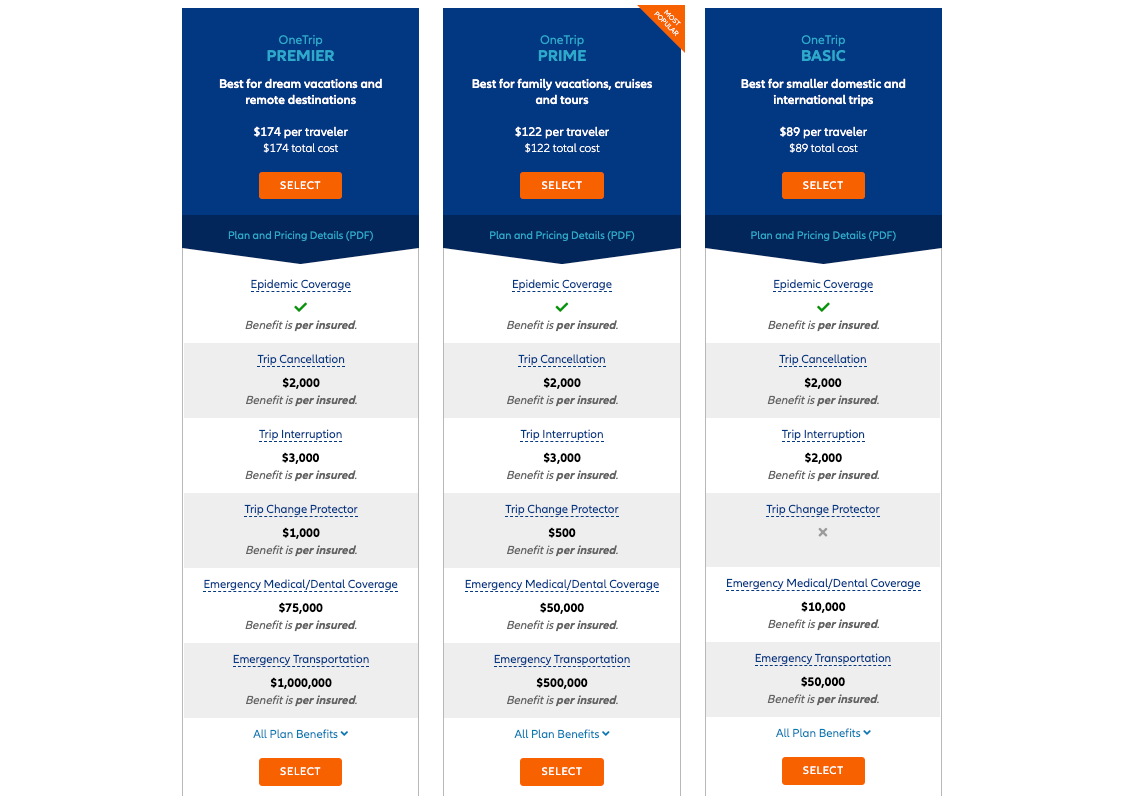

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

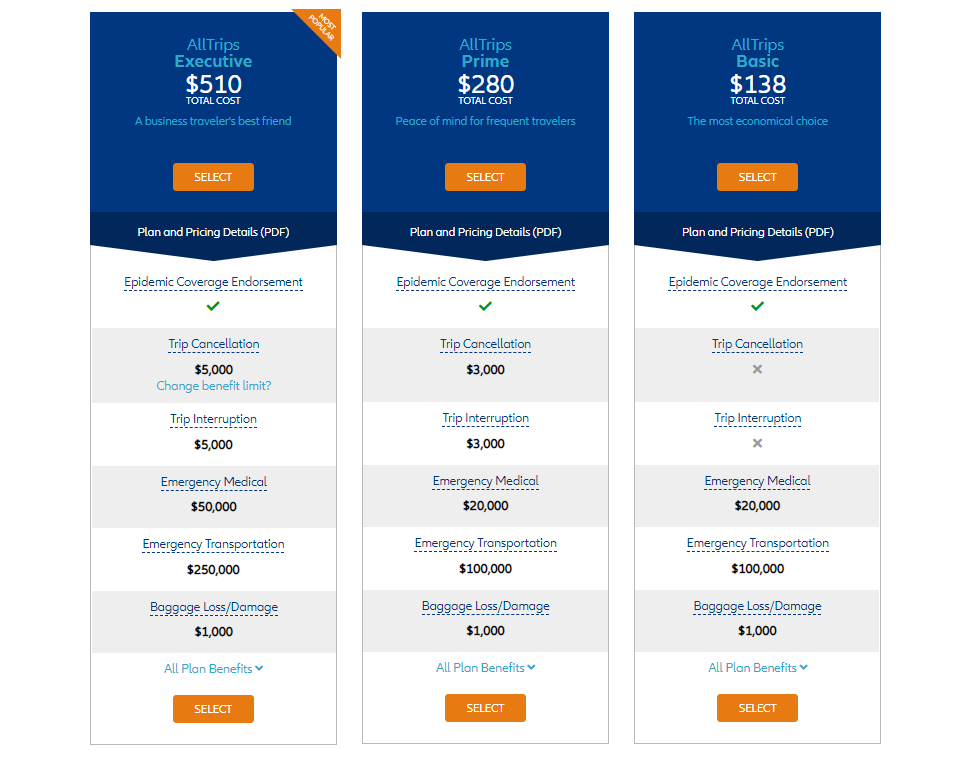

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

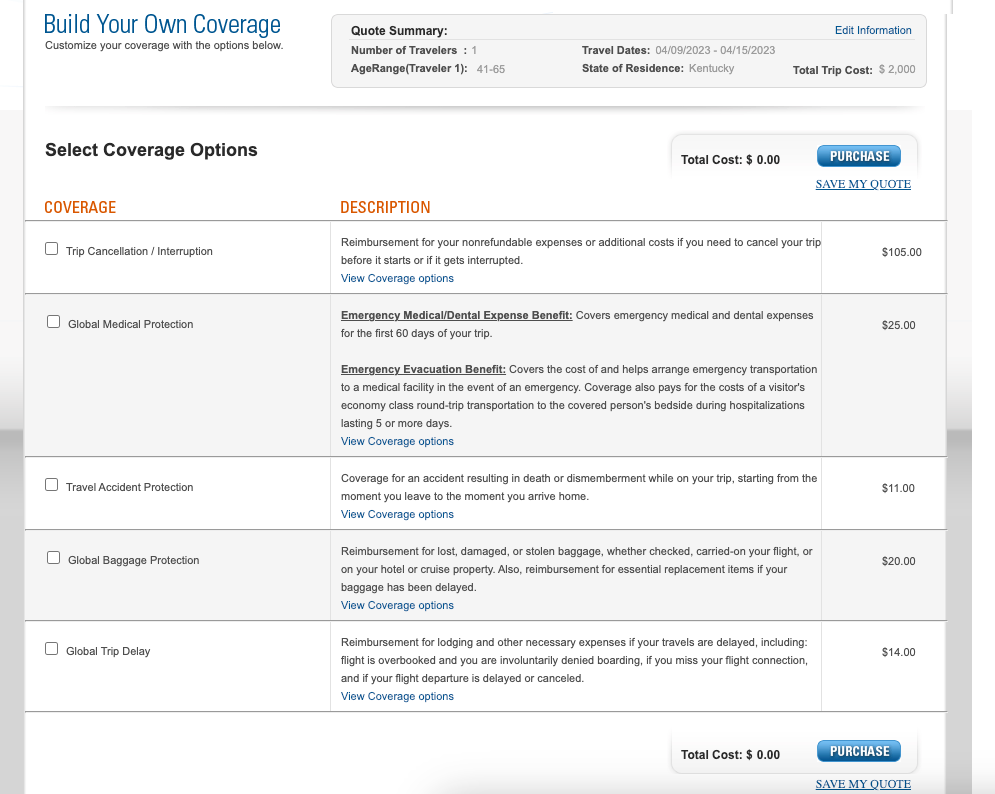

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

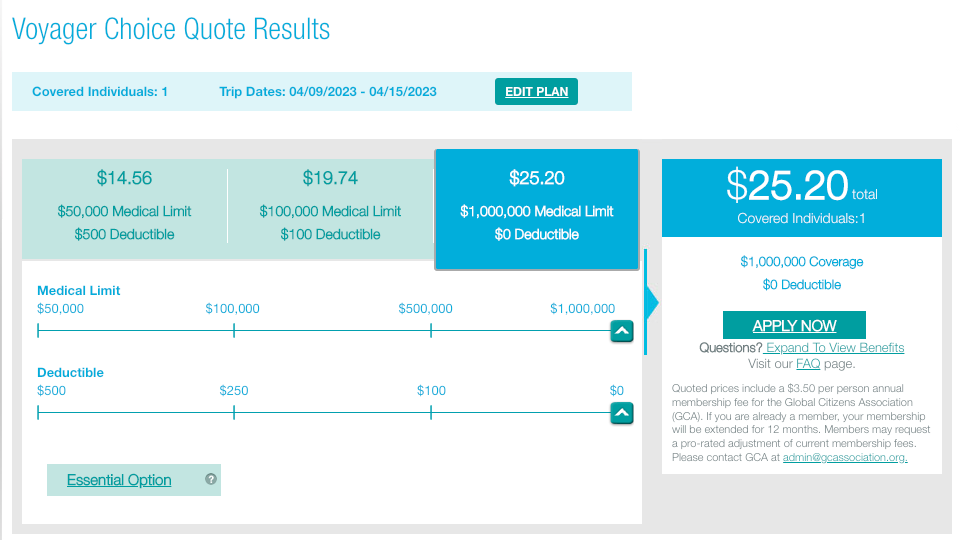

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

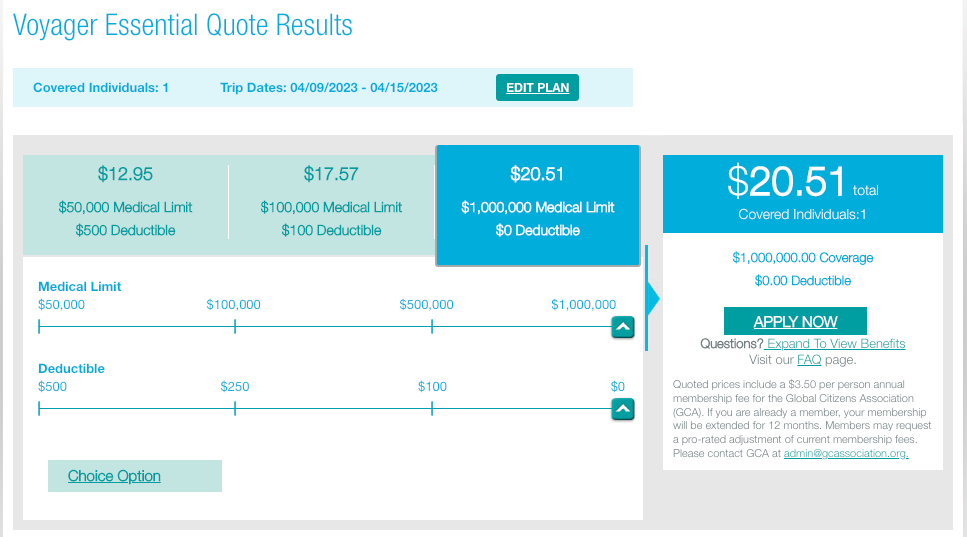

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

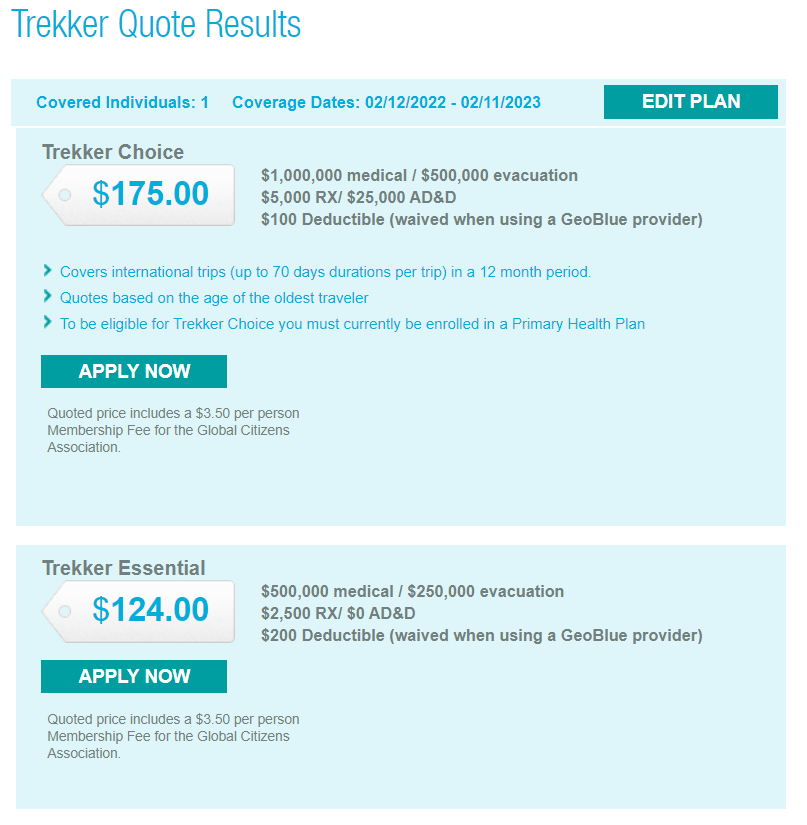

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

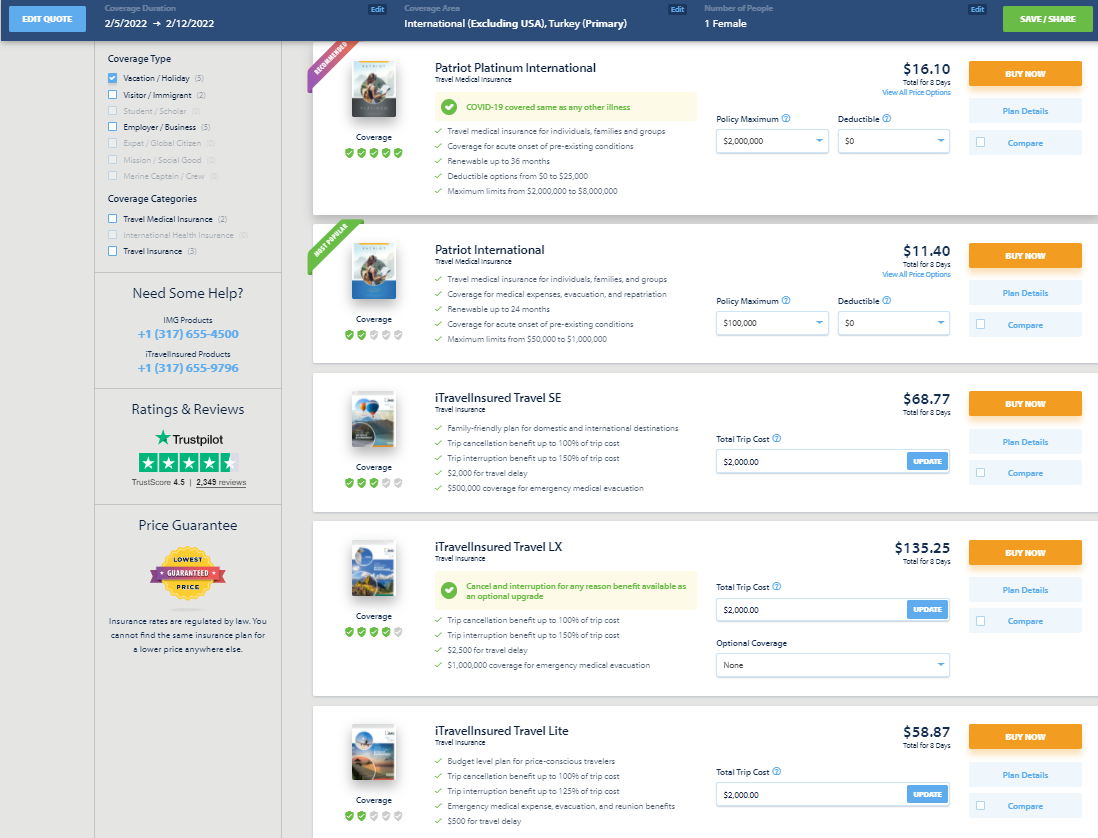

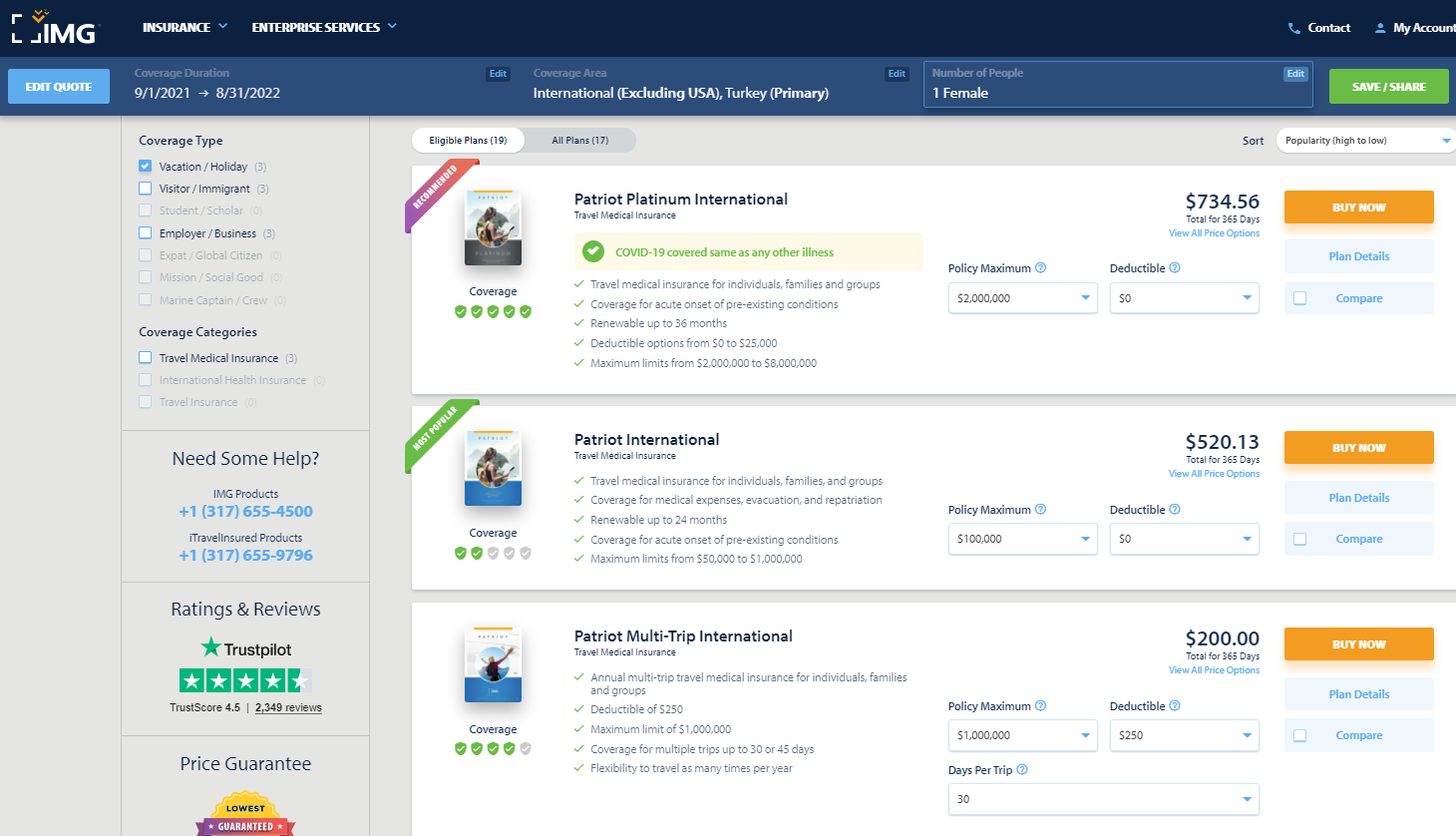

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

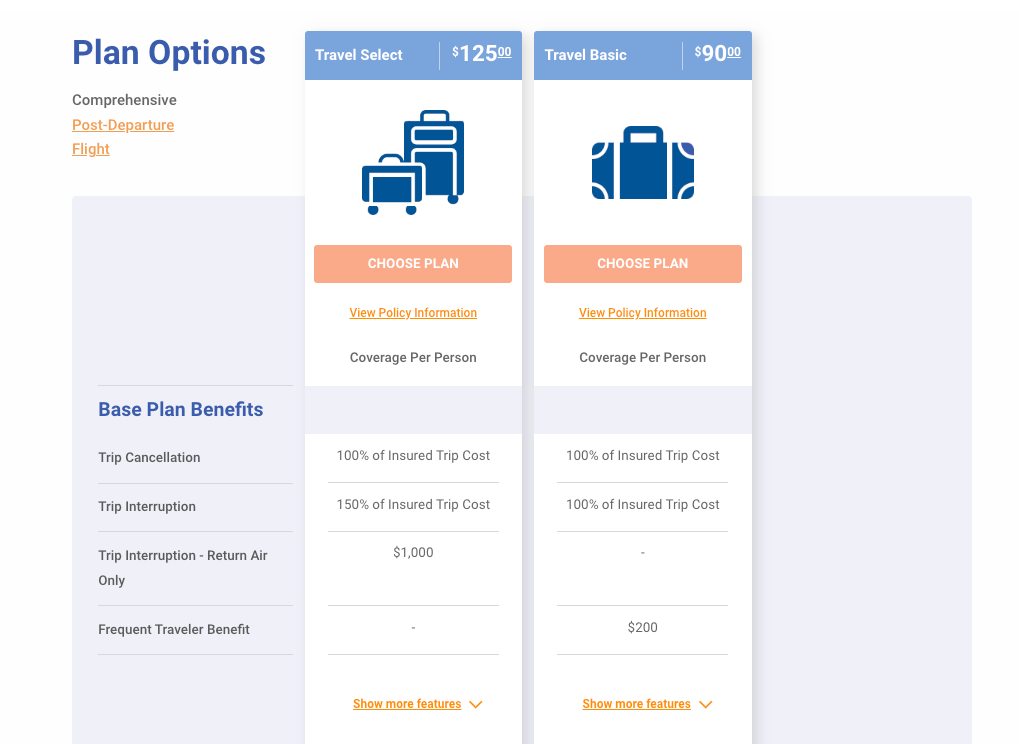

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

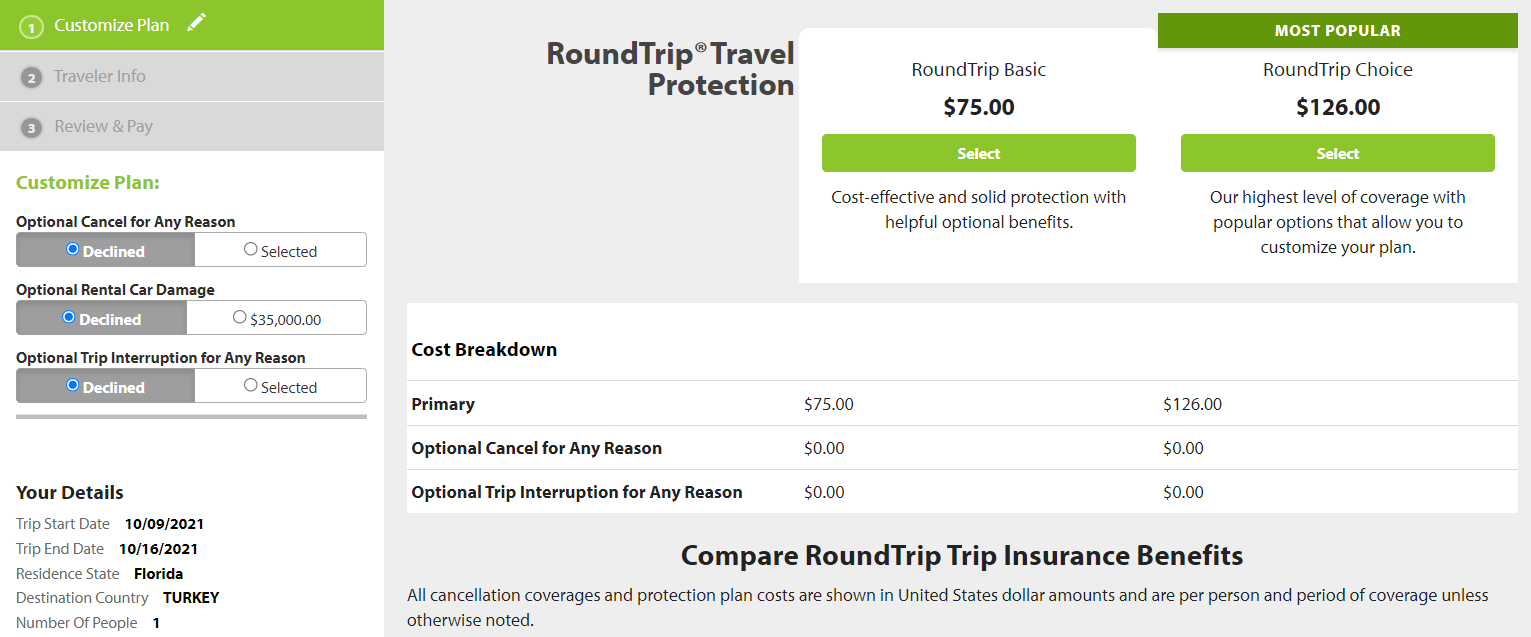

Seven Corners

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

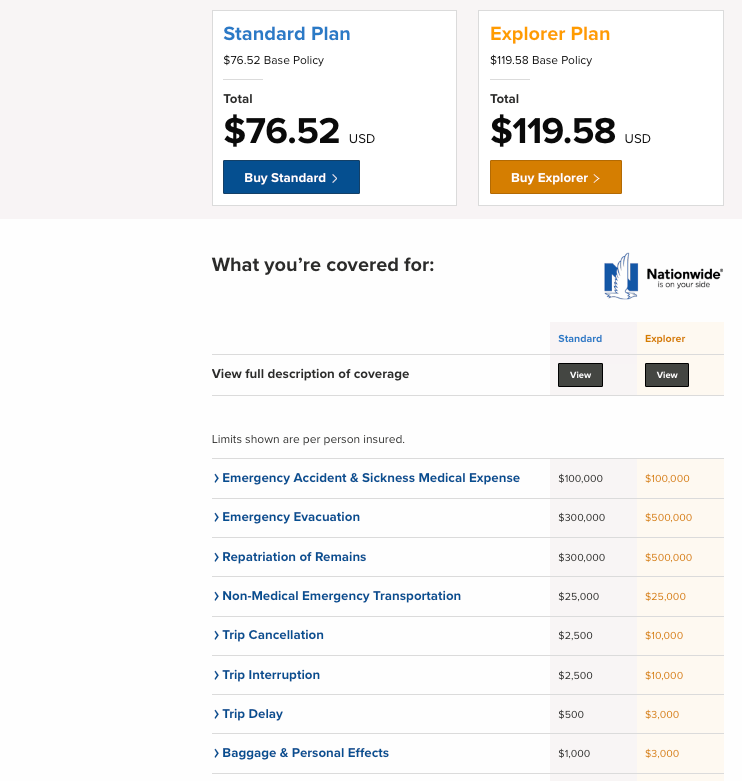

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

The World's Best Travel Insurance for Long-Term Travelers

Updated: Jan 13, 2023 • by Thomas K. Running

While there are many types of insurance you might buy as a digital nomad or long-term traveler, the most essential is usually travel insurance—specifically a comprehensive “travel health insurance” policy.

Some of us may also need global primary health insurance (often called expat health insurance).

To help you determine the right type of insurance for your situation, I’ve created a short, interactive quiz. No personal data or contact details required!

In short, as long as you’re covered for long-term health care in your “home country” or somewhere else where you have the legal right to live indefinitely, a travel health insurance plan that covers medical costs in case of accidents and serious illness abroad is what you’ll need. And that’s what I’ll cover in this article.

Coronavirus update 🦠 Due to the novel coronavirus and the resulting COVID-19 pandemic, I want to provide some resources related to travel, insurance coverage, and how to stay safe and avoid disruptions to your travel plans. Insurance coverage of COVID-19: It’s very common for insurance policies to contain general exclusions regarding epidemics and pandemics, meaning it’s not a given that expenses related to the coronavirus outbreak will be covered by your policy. Check with your insurance provider to be certain what’s covered. SafetyWing now fully covers COVID-19 related illness as of August 1, 2020. They even cover PCR tests if deemed medically necessary by a doctor. Read more here . World Nomads do not cover anything related to the COVID-19 (or any other) pandemic for customers from most countries (their insurance policies vary depending on where you’re from). US residents are the one exception to the rule that I spotted. Read more in their FAQ (make sure to select the same country of residence you used when signing up). Changed travel plans It also varies what insurance providers will cover if your travel plans were affected by the pandemic (so check with them). However, many airlines (as well as hotels, cruise companies, car rental agencies, etc) are allowing you to make changes to your reservations free of charge. In many cases, they’ll even refund tickets you no longer need, want, or can use. Helpful resources: Worldwide travel restrictions (IATA) Information on country-specific measures (US State Department) WHO’s COVID-19 pages CDC’s coronavirus pages

Table of Contents ↺ Coronavirus update Should you insure your stuff? The alternative: Self-insure for the little things Getting the right insurance Travel Health Insurance Emergency Evacuation Travel Insurance Things to note when picking your policy The Showdown SafetyWing World Nomads True Traveller IMG Travel Health Insurance Other insurance providers worth looking into Common questions (FAQ)

Should you insure your stuff? 🎒

While some insurance is important, I’d recommend against getting too much insurance. Keep in mind that, on average, getting insurance doesn’t pay off financially. The insurance companies need to collect enough in premiums to cover not only claims (legit and fraudulent) but also their own staff, marketing, and profit margins.

My personal policy is to insure against the unlikely events that would ruin me financially.

Yes, it sucks having to pony up $2000 for a new MacBook Pro if it were to get stolen or destroyed. But is it worth paying $500 dollars for certain every year, just in case? Only if you cannot possibly manage to save up a few thousand dollars as a buffer or make do with a less expensive laptop for a while in case it breaks and can’t be fixed at a reasonable price.

If someone stole all the belongings that I travel with—including the clothes I was wearing and the phone in my pocket—it would cost me about $6000 to replace it all with brand new items.

While painful, I have enough of a buffer that it wouldn’t put me in debt. And the likelihood of it happening in the first place is quite slim. Hence, I won’t waste any money insuring my possessions.

The alternative: Self-insure for the little things 💰

Most people are paying way too much in insurance premiums. I can appreciate that you might value the extra peace of mind that comes with knowing that you’re covered no matter what happens.

But if you start doing even rudimentary back-of-the-envelope calculations, it becomes clear that you’re throwing money out the window.

Instead, consider this approach.

Get quotes for insuring everything you instinctively want to insure. Missed flight connections. That camera you bring along but almost never use. Your smartphone. Your laptop. Baggage delays. Petty theft. And, of course, emergency travel health insurance.

Get quotes for everything with zero deductibles if possible.

Let’s say your total yearly premium comes to $3000.

Then look at what you would be paying if you only get insurance for the stuff that would ruin you financially. In other words, probably only emergency health insurance.

Pick the highest deductible you’re comfortable with. At the very least a couple of hundred dollars per year. Remember, your goal is to never actually have to use the insurance, so it’s better to pay less every year and potentially a bit more in the year where you actually need to rely on your policy.

Say you end up with a premium of about $500 per year. As you’ll see later, that’s a very easily attainable number.

Now, buy the cheap insurance with the high deductible. Every year, put the money you saved ($2500 in this example) on a high interest savings account (or even better, a low-cost index fund or ETF ) earmarked for situations where you would have relied on the expensive, all inclusive insurance.

Now sit back and watch your own personal insurance fund grow ever larger year by year. Whenever you need to pay for something that would have been covered by the more expensive insurance (including deductibles), just withdraw the money to cover it from your own insurance fund.

As an added bonus, you don’t even have to fill out lengthy claims forms, go hunting for old receipts for your valuables, and fight with claims agents that are trying their very best to find loopholes to avoid paying you what you’re rightfully owed.

Getting the right insurance

Let’s take a look at the different types of insurance you should consider getting for your trip.

Travel Health Insurance 🏥

Even if you’re covered for health expenses in your home country, it’s important to be covered for emergencies abroad.

What would happen if you’re in the US, or Japan, or Australia (or even countries where health care is cheaper), and you get a debilitating disease or end up in an accident that has to be treated locally?

You’ll very quickly end up with medical bills in the tens if not hundreds of thousands. Unless you have insurance, that is.

A good emergency medical travel insurance will take care of any costs of any life-threatening treatment you get locally.

It’s important to note that most travel health insurance policies are not “primary” health insurance policies. They rely on you being entitled to treatment somewhere and will ship you there if needed for long-term care.

So even if you get travel health insurance, it’s important that you make sure you’re covered for long-term treatment at “home”.

If that’s not the case, you should check out our article on worldwide primary health insurance .

Emergency Evacuation 🚁

Many travel health insurance policies come with built in emergency medical transportation or emergency medical evacuation as it’s often called. There are also standalone evacuation memberships, which tend to be quite a bit more expensive for similar coverage.

What exactly is covered by such policies, what limit is sufficient for your needs, and do you actually need it?

Usually, an emergency evacuation policy will kick in when the initial hospital or medical facility is not suited to provide the appropriate care for your medical emergency.

The decision to move you elsewhere will usually be made by the local doctor and your insurance company’s medical advisor.

While the policy will cover transportation to a suitable hospital, the medical costs on arrival are not covered—unless part of a travel health insurance policy . In other words, the standalone evacuation memberships usually only cover you until you’ve reached the hospital.

Due to their nature, emergency evacuation policies are most essential if you’re often hiking in remote areas, traveling or staying long-term in less developed countries, etc. If you’re spending most of your time in large cities in developed countries, it’s less important. In that case you should just make sure you’re covered for individual trips you make where it can come in handy.

The policy limits usually range from $25,000 up to millions or even unlimited . Since evacuation costs can get really high in extreme cases, I’d recommend a policy with at least a $100,000 limit. Perhaps even more if you’re traveling in very remote and underdeveloped areas.

Travel Insurance 🛫

Although all the different types of policies we have covered so far could fit under the umbrella term travel insurance , in this section I am referring to things like delayed or lost baggage, missed flight connections, car rental insurance, and so on.

If you have it included in a credit card or similar for free, then of course it’s worth having. Rental Car insurance can save you some money as well, but make sure to read the fine print.

Many travel health insurance policies include some coverage for these things as well, so if you’re anyway getting that kind of insurance (which you should) and the price differential is small, it can be worth to get it bundled. As you’ll see below, my recommended all-in-one insurance (SafetyWing) is actually cheaper than the already affordable health-only insurance from IMG.

If on the other hand you’re not covered through your credit cards or other insurance you already have, spending money on a dedicated travel insurance is usually a terrible deal bordering on pointless. There are a few reasons why this is the case:

- It’s very unlikely that anything will happen, and if it does the insurance policy probably has an exclusion

- If something happens, it will be relatively cheap to deal with on your own

- In many cases you can get compensation from airlines or others, even without insurance

Let’s take one example; missed flight connection insurance . Most policies require from two to four (!) hours in between flights to be valid.

Ask yourself, how often are you traveling with connecting flights on separate tickets? Perhaps some times, but likely not that often.

And how many flights are more than two to four hours delayed? Only about 0.1% to 1.5% of flights, depending on airlines (US airlines generally coming out behind).

Assuming you mostly fly on through tickets and only have a handful of risky connections on separate airlines per year, that’s a very slim chance (perhaps 1-2%) that you will miss a flight connection on separate tickets in a given year. And even if you did, the expected cost of an average replacement ticket is only a few hundred dollars.

That means, even with as much travel as most nomads do, the expected financial loss of missed connections is only a few dollars per year. So skip the insurance, and put the money saved into your own self-insurance fund .

Things to note when picking your policy

- Usually whenever you extend your policy (technically, when you enter a new period of coverage ) any things that happened before the extension will now be treated as pre-existing conditions , and will often no longer be covered.

- You’re a legal (tax) resident of that country. If you’re traveling long term you might not be.

- For trips of a certain length (often 30 or 60 days, but I’ve also seen 90 days) before you have to return to your home country. Many even require you to have purchased round trip flight tickets before embarking on your trip for your coverage to kick in.

- If it’s a credit card policy, if at least 50% or even 100% of the trip costs have been pre-paid with the card in question.

- Many insurance policies (even some of the ones included in this article) limits the number of visits you might make to your home country during the lifetime of the policy. Say you purchase a typical one-year policy, and you happen to visit your home country for any reason more than once in that period, the rest of your policy will be canceled with no refund given.

- When it comes to deductibles, look out for if the deductible is per incident or per policy period (which can typically extend to a year). The latter is clearly better, since if you already had to pay the deductible once, you don’t have to pay it for the rest of the period/year.

The Showdown 🥊

In the rest of this article I will compare some of the most popular and well-suited insurance policies for digital nomads and long-term travelers who already have some sort of primary health insurance cover at home.

I’ve included policies that meet these basic requirements:

- It should be possible to buy and renew the insurance while already traveling.

- They should be available to the residents of many if not most or all countries.

- There should not be any upper limit for how long you can travel before returning home.

Note that all prices are rounded to the nearest dollar.

This relative newcomer is my personal top choice , and what I’m personally using. And while SafetyWing is still a startup (launching about two years ago), their insurance policy is backed by Tokio Marine, one of the most solid insurance companies in the world. So in the unlikely event that something were to happen to SafetyWing, you would still be taken care of by Tokio Marine.

Their long term goal is to offer a complete suite of products to build a country-independent social safety net for freelancers and digital nomads , which I think is really cool! In addition to the travel health insurance described here, they also recently launched a complete worldwide primary health insurance called Remote Health , so if you don’t have health coverage in your home country, check that out! However, their first product (which is what I describe in this article) is marketed as a “ digital nomad travel insurance ”.

And compared to the alternatives, it is both a really good value and offering some genuinely useful features that I know many of you will appreciate.

In many ways it’s even more comprehensive than the competitors, but still only a fraction of the price.

Some highlights:

- Recurring billing . Pay monthly just like you would for Spotify or Netflix without having to decide upfront for how long you need the policy. Why other companies don’t offer this is to me a complete mystery.

- The lowest cost of any company in this comparison. For a worldwide excluding the US policy you’ll pay about $37 per month, while most comparable companies charge over $100 for a less convenient product.

- A yearly deductible . While most companies charge a deductible for each claim, SafetyWing will cap your deductible at $250 per policy period (which—as long as you keep your subscription running—equals 364 days).

- No deductible at all for many types of claims , including emergency dental, emergency medical evacuation, repatriation of remains, crisis response, emergency reunion, bedside visit, trip interruption, accidental death and dismemberment, lost checked luggage, travel delays, personal liability and a bunch more.

- Home country coverage . While most of the competitors might even void the rest of your policy if you visit your home country, SafetyWing’s policy will even cover you in your home country for up to 30 days per 90 days of insurance.

- The same low daily price no matter how short cover you buy. Perfect for nomads who have other health coverage in the countries they spend most of their time (e.g. EU/EEA residents spending a lot of time in Europe), and only need cover for part of the year while traveling elsewhere.

- Covers private health care . No need to go to a public hospital or doctor in a third world country when there’s a much better private one available.

- They support direct billing to most hospitals and clinics in their extensive, worldwide network (searchable on your online account page). You can still opt for a different medical provider, but you’d generally have to pay out of pocket and be reimbursed later.

Some things to note:

- A bit high price if you order their US inclusive policy for a long time. If you are planning on visiting the US, you’re better off getting the US cover only while you’re in the country and switch back to the non-US cover as soon as you leave.

- After 364 days of coverage, the insurance will lapse if you don’t actively renew it. Luckily that’s as simple as clicking a link in an email that will be sent to you before your current policy expires.

Pricing for a 35 year old nomad who’s already traveling:

For recurring policies longer than 28 days, payment is only due every 4 weeks , so you don’t have to pay for a long policy in advance , unlike virtually any other insurance company.

Full policy wording

World Nomads

They might have been innovative a decade ago, but today I sincerely believe most bloggers are only recommending them due to financial incentives (they pay bloggers—including me—for referrals) or plain ignorance. Or perhaps a combination of both?

What they offer might have been revolutionary 10 years ago (travel insurance that could be purchased and renewed while already traveling), but today there are better alternatives available.

I’m really not sure what World Nomads offer that can justify the more than triple price, but my hunch is that it’s mostly due to brand recognition rather than any tangible benefits to you as a customer.

If you get their most expensive package, you do get pretty good extreme sports cover, although they have recently become much more restrictive here than before—without that being reflected in the price.

Highlights:

- They support direct billing , at least in some circumstances. In my only experience being hospitalized while covered by their Explore plan, I still had to pay the hospital myself and got the settlement about 6 weeks later. But they do claim that they can arrange direct billing, so I assume they would help out if the claim was a bit bigger (mine was only about $1300).

- Decent extreme sports cover in their most expensive package (although not as good as it used to be).

Things to note:

- Since World Nomads use different insurance providers depending on your country of residence the insurance price, terms, limits and benefits vary from one country to another . Be extra careful to read the full policy wording for your country of residence.

- Extensions are expensive . Say you take out and pre-pay for a long-term policy, you would pay about $75 to extend your policy with a mere week (assuming you’re from the US and on the Explorer plan).

- You’re only allowed return home once during the entire duration of your policy. If you’re a nomad with a home base, or you tend to return home to visit friends or family on occasion, you’re effectively not able to buy a long term policy to save money. Instead you’ll have to buy a series of short and expensive policies.

I’ve used World Nomads a bit in the past (with BUPA Global as the insurance provider) and while the claims involved lots of paperwork they usually were handled fairly. Payouts aren’t super quick, and I had to send them a few reminders before the claims were settled.

The only time I had an issue (which was at least partly my fault) was when I waited until only a few days before the expiry of my current insurance policy before extending it. In that brief time window a close relative first got very ill and later passed away. Since the relative became ill before I had ordered the extension (even though I was unaware of it until a few days after and she only passed away into my new policy period, since it was no longer “unexpected”), they refused to cover my round trip tickets back to Europe so I could attend the funeral.

According to the policy wording they were of course in the right, although someone more understanding could have used their discretion to decide otherwise. Anyway, with the auto-renewal feature that SafetyWing offers this would have been a non-issue.

Note that pricing for World Nomads depend on your country of residence. To get the long term discounts you have to order and pay for the whole period in advance . Extensions are charged at non-discounted prices and will start a new policy period. If you’re at all unsure about how long you need your policy, you’re much better off using SafetyWing’s subscription feature or another insurance provider with cheap extensions (also like SafetyWing, and IMG below).

Base price of a Standard/Explorer plan for a 35 year old traveler from the UK (prices converted from GBP at the time of writing):

Base price of a Standard/Explorer plan for a 35 year old traveler from the US :

The policy wording varies depending on your country of residence . To see the full policy wording, you have to request a quote where you enter your country of residence. On the next page look for the section “View full description of coverage,” and click the View button under the heading of the plan you are interested in.

True Traveller

This is a popular provider, particularly in the UK. Their insurance is only available to residents of the UK and other countries in the EEA.

Their cheaper plans are quite affordable—especially if you pre-pay for a year or more—but they are also quite limited and restrictive in what they cover. Adding various extras will quickly increase your premium.

- No limit on home visits , however you are not covered while in your home country .

- They have lots of good reviews on Trustpilot , for what that’s worth.

- They will strive to arrange direct billing for covered medical treatment surpassing £500. Below this you’ll generally pay out of pocket and be reimbursed once your claim is processed.

- Extensions cost a lot . E.g. if you had a 52-week policy (costing $462 with no extras) you would pay a whopping $50 to extend your policy by a mere week.

- Only available to current EEA residents . If you are a full-time nomad or have a base outside of the EEA, you likely won’t qualify even if you’re from the EEA.

- Does not cover private medical treatment unless no public treatment is available. Personally, I was really happy that my insurance covered private hospital stays when I got hospitalized in India a few years ago. Just saying. Update: True Traveller responded below , clarifying what this policy means in practice.

Base price* for a 35 year old nomad who is already traveling (prices converted from GBP at the time of writing):

* Their pricing changes massively depending on which extras you include. A 7 day policy ranges from £34 to £361 depending on your selections. A 52 week plan can get as pricy as £1511 with all extras selected. In this table I’ve included their mid-range package (“Traveller”), with zero extras and a £75 deductible per claim.

Policy wording

IMG Travel Health Insurance

This is an affordable travel health insurance, which does not include any non-health related benefits (unlike the previous options).

IMG is a financially solid company, with some of the best prices out there. For a reasonable health-only policy it’s a popular budget option, but be aware that they have a reputation for slow claims handling and sticking to the letter of the policy wording beyond what some people would find reasonable.

- Flexible deductibles , so you can select a high one and reduce your premiums.

- The deductible is only payable once per 12 months of continuous coverage (like SafetyWing ).

- Extending and renewing your policy is a lot cheaper than e.g. World Nomads and True Traveller, so if you find yourself needing your policy a bit longer than expected, it won’t break the bank. Extending this way will start a new policy period, however, (unlike SafetyWing’s subscription) which means issues that already arose while traveling will be treated as pre-existing and no longer covered.

- This is a travel health only policy , and will not cover things like trip interruption, travel delays, lost luggage, etc. It is still more expensive than the SafetyWing insurance , which includes those things. Also note that it’s still not primary health insurance , so you still need to be covered in your home country.

- Your insurance will be terminated if you return to your home country for more than 14 days, or at all if your home country is the United States or you returned home for medical reasons.

- They generally don’t support direct billing (i.e. the hospital or doctor billing them directly), which mean you might have to pay pretty hefty medical bills out of pocket and then wait for your claim to be processed before you will be reimbursed.

- The plan which includes travel in the US is not available to US residents .

Pricing for a 35 year old single traveler ( travel health only , $500,000 limit, $250 deductible):

Policy documents:

- Patriot International (excluding travel to the US)

- Patriot America (including travel to the US)

Other insurance providers worth looking into

While not available everywhere, Allianz is an insurance company with a good reputation and (sadly also) premium prices. They tend to be a bit pricier than the options we’ve looked at so far.

Click here to see if they offer their travel insurance product in your home country.