Compare Cheap Travel Insurance Quotes

Peace of mind while you travel.

For such an important product, travel insurance is often all too easy to overlook. As with most kinds of insurance, you always hope to not need it, but on the off chance that you do fall ill or injure yourself on your travels, you could find yourself facing huge bills if you don't have adequate cover.

Travel insurance is for more than just medical bills though - the right policy will also pay out if your flight is delayed, or if your baggage goes missing, for example.

Arguably the most important thing you'll need travel insurance for is to cover you should you fall ill or injure yourself while abroad. Medical treatment can be very expensive in other countries, as can travel in ambulances should you need to be transported to a hospital from far away. Travel insurance policies will typically cover you for a huge amount of expenditure on medical bills for a relatively low up front cost.

It's not just for medical bills though. Many policies will also cover you for:

Often, travel insurance providers will refuse to cover you for treatment related to any pre-existing medical conditions. This includes anything that you've had treatment for in the past.

Just Travel are different. They have a large panel of specialist insurers so that they can get you a tailored policy that gives you exactly the kind of cover you need, regardless of your medical history.

The following quotation is offered in partnership with ME Expert LTD and SEOPA LTD, in order to effectively offer this service information may be passed between both providers, all information in handled in accordance with the General Data Protection Regulation (GDPR) 2016. Both parties act as licenced Data-Controllers as defined by the ICO and act as such. For more information, please see our Privacy Policy and Terms of Service, please be aware that information entered may also be subject to the Privacy Policy and Terms of Service of SEOPA LTD.ME Expert is an appointed representative of Money Expert Limited who are authorised and regulated by the Financial Conduct Authority FRN679652

Ad-free. Influence-free. Powered by consumers.

The payment for your account couldn't be processed or you've canceled your account with us.

We don’t recognize that sign in. Your username maybe be your email address. Passwords are 6-20 characters with at least one number and letter.

We still don’t recognize that sign in. Retrieve your username. Reset your password.

Forgot your username or password ?

Don’t have an account?

- Account Settings

- My Benefits

- My Products

- Donate Donate

Save products you love, products you own and much more!

Other Membership Benefits:

Suggested Searches

- Become a Member

Car Ratings & Reviews

2024 Top Picks

Car Buying & Pricing

Which Car Brands Make the Best Vehicles?

Car Maintenance & Repair

Car Reliability Guide

Key Topics & News

Listen to the Talking Cars Podcast

Home & Garden

Bed & Bath

Top Picks From CR

Best Mattresses

Lawn & Garden

TOP PICKS FROM CR

Best Lawn Mowers and Tractors

Home Improvement

Home Improvement Essential

Best Wood Stains

Home Safety & Security

HOME SAFETY

Best DIY Home Security Systems

REPAIR OR REPLACE?

What to Do With a Broken Appliance

Small Appliances

Best Small Kitchen Appliances

Laundry & Cleaning

Best Washing Machines

Heating, Cooling & Air

Most Reliable Central Air-Conditioning Systems

Electronics

Home Entertainment

FIND YOUR NEW TV

Home Office

Cheapest Printers for Ink Costs

Smartphones & Wearables

BEST SMARTPHONES

Find the Right Phone for You

Digital Security & Privacy

MEMBER BENEFIT

CR Security Planner

Take Action

Money-Saving Strategies for Buying Travel Insurance

5 tips for navigating to the right choice for your trip, sharing is nice.

We respect your privacy . All email addresses you provide will be used just for sending this story.

If you're planning a summer vacation , thinking about what could go wrong is probably the last thing you want to do.

But travel insurance could come in handy if your trip is canceled or interrupted due to a medical emergency, a natural disaster, or another unforeseen event. And deciding whether you need it—and if so, what kind—means planning for the worst.

The first question is whether you need a policy at all. The answer? Not always, according to Jeffrey Miller, a travel law attorney and professor at Florida Atlantic University, who says that much depends on your personal situation as well as the type of trip.

"The millennial going to Las Vegas doesn't need travel insurance," he says. "But if you're in your 40s and have elderly parents who might fall ill and cause you to cut short your holiday, then yes, you should definitely get coverage."

In general, it's probably prudent to protect any trip that's valued at more than a few thousand dollars. Beyond that, other factors to consider might be the age and health of the travelers and whether your itinerary takes you into remote or risky territory.

"Our No. 1 claim type is trip cancellation," says Berkshire Hathaway Travel Protection vice president Carol Mueller. So bear in mind that you don't always need a Cadillac plan that covers everything from lost baggage to medical evacuation costs.

There are, of course, a multitude of plans to choose from, and you can narrow it down with the help of a travel agent or an online aggregator. Generally, policies fall into three categories—basic, midlevel, and premium—with coverage and prices rising accordingly.

Typically, premiums for comprehensive coverage range from 4 to 10 percent of the total tab of your trip. In recent years, however, travel insurers have come out with tailored policies at lower prices. For example, Berkshire Hathaway has a no-frills "Air Care" plan that just covers flight mishaps like delays or lost bags, starting at $26 for a simple round trip.

If you do decide you need to cover all bases, however, you might want a broad-based policy. Just bear in mind that it's important to know exactly what's covered.

Inquiries to travel insurance companies typically soar after high-profile events like acts of terrorism, or an outbreak of a disease like the Zika virus. For example, calls to insurers spiked after the recent grounding of the Boeing 737 Max , according to the comparison site Insure My Trip. But as anxiety-provoking as events like these may be, under most travel insurance plans, they're not considered valid grounds to get a full refund if you cancel your trip.

Here, five guidelines to make sure you get what you need without overpaying.

Check Your Existing Insurance Coverage

You may already have some travel insurance as a perk of your credit card, but you'll need to check.

Some credit card issuers offer coverage for car rental damage, lost luggage , or trip cancellation, but any protection they do offer is likely to come with some limits on the ultimate payout. For rental cars, your personal auto insurance may cover you, too.

Nonetheless, if you have credit card coverage, you may be able to get by with a less expensive general trip protection plan. And when it comes to baggage , know that coverage from travel insurers is typically considered secondary, meaning it will pay only for anything in excess of what you're entitled to if you file a claim with your airline .

It's also worthwhile to look into your health insurance and whether it will cover you when you're on the road. Medicare, for example, won't help if you're not in the U.S., but other insurers might.

Aetna, for instance, covers policyholders on international trips, but the care is reimbursed as "out of network," which means higher out-of-pocket costs. And if you have an accident and need to be airlifted to a hospital, the costs of care can skyrocket .

If you're buying travel medical insurance, be aware, too, that some policies won't cover pre-existing conditions. Even when they do, they're often dependent on your purchasing the policy close to the date when you bought the trip. (Some have a "look back" clause that can search your health records for as long as a year prior.)

Comparison Shop

If your trip planning begins with booking an airplane ticket, you'll almost certainly be prompted to buy trip protection from the airline before you hit the purchase button. Don't rise to the bait, says Miller. "It's better to seek out all the options before you buy."

Whether or not you buy through them, websites like InsureMyTrip and SquareMouth provide free quotes from multiple insurers and make it easy to filter search results by your customized needs.

In many states, travel agents who sell trip insurance are licensed for that purpose, and their knowledge and experience can also help narrow your choices appropriately. Whatever source you use, think carefully about what benefits you actually need before putting your money down.

Be Aware of Timing Provisions

Perhaps it's hurricane season, and you're having second thoughts about having paid in full for that upcoming beach holiday in the tropics. Can you take out an insurance policy to ease your worries?

You might be able to, but don't wait until a particular storm threatening your vacation is powerful enough to have been christened, advises Berkshire Hathaway's Mueller.

"When a hurricane is named, it is no longer an unknown event and no longer covered as a reason for cancellation" if you haven't already purchased the policy, she says.

That's not the only timing factor to consider. A terrorist attack in your intended destination could be grounds to cancel under some policies with a terrorism clause. But usually that coverage applies only if you're traveling within 30 days of the event. If your trip is still six months away, the insurance won't pay out simply because you no longer want to go.

In general, you may be able to buy some types of trip protection up to 24 hours before your departure, but waiting until that point might mean you can get only basic coverage like baggage loss or damage protection and emergency medical coverage, according to Allianz Travel Insurance .

For more comprehensive coverage that includes benefits like a pre-existing medical condition waiver or protection if a trip is canceled because of a terrorist attack or an airline bankruptcy, a policy typically must be purchased within 14 days of making the initial trip deposit.

Look Into Annual Plans

If you're taking more than two major trips per year, an annual plan could be a better deal than paying as you go with single-trip policies, according to Stan Sandberg, co-founder of TravelInsurance.com . Both types of plan can cover the same occurrences (trip cancellation, medical emergencies), but the year-long coverage could bring your pro-rated costs down.

For example, insurance provider April Travel Protection recently launched a customizable annual plan that covers an unlimited number of trips per year, both in the U.S. and abroad. Customers can choose their level of coverage for trip cancellation or interruption, medical care, evacuation, and other events.

Prices start at $75 for those under 30, rising up to $179 for those 60 years or older. This policy isn't sold in all states, however, and the state of Washington doesn't permit annual plans of any type to be sold there.

Be Careful About CFAR Insurance

Every insurance policy has sits own specific rules about what triggers coverage. That's why you should be skeptical of "cancel for any reason" (CFAR) insurance, which sounds appealing but is pricey, frequently running 40 percent more than basic insurance. What's more, this coverage often pays out only from 50 percent to 75 percent of your total expenses vs. the full cost paid by regular travel insurance.

Some states, such as New York, may limit or prohibit sales of CFAR policies. (The New York Department of Financial Services explains that because insurance is intended to protect against unforeseen events, CFAR can't be considered real insurance since it allows the buyer to control the reasons for filing a claim.)

So keep in mind that trip insurance, like all other protection policies, is subject to state regulation, which can vary widely around the country. Check with your own state's regulator if you're concerned whether you can buy a particular type of coverage.

Be the first to comment

- Auto Insurance Best Car Insurance Cheapest Car Insurance Compare Car Insurance Quotes Best Car Insurance For Young Drivers Best Auto & Home Bundles Cheapest Cars To Insure

- Home Insurance Best Home Insurance Best Renters Insurance Cheapest Homeowners Insurance Types Of Homeowners Insurance

- Life Insurance Best Life Insurance Best Term Life Insurance Best Senior Life Insurance Best Whole Life Insurance Best No Exam Life Insurance

- Pet Insurance Best Pet Insurance Cheap Pet Insurance Pet Insurance Costs Compare Pet Insurance Quotes

- Travel Insurance Best Travel Insurance Cancel For Any Reason Travel Insurance Best Cruise Travel Insurance Best Senior Travel Insurance

- Health Insurance Best Health Insurance Plans Best Affordable Health Insurance Best Dental Insurance Best Vision Insurance Best Disability Insurance

- Credit Cards Best Credit Cards 2024 Best Balance Transfer Credit Cards Best Rewards Credit Cards Best Cash Back Credit Cards Best Travel Rewards Credit Cards Best 0% APR Credit Cards Best Business Credit Cards Best Credit Cards for Startups Best Credit Cards For Bad Credit Best Cards for Students without Credit

- Credit Card Reviews Chase Sapphire Preferred Wells Fargo Active Cash® Chase Sapphire Reserve Citi Double Cash Citi Diamond Preferred Chase Ink Business Unlimited American Express Blue Business Plus

- Credit Card by Issuer Best Chase Credit Cards Best American Express Credit Cards Best Bank of America Credit Cards Best Visa Credit Cards

- Credit Score Best Credit Monitoring Services Best Identity Theft Protection

- CDs Best CD Rates Best No Penalty CDs Best Jumbo CD Rates Best 3 Month CD Rates Best 6 Month CD Rates Best 9 Month CD Rates Best 1 Year CD Rates Best 2 Year CD Rates Best 5 Year CD Rates

- Checking Best High-Yield Checking Accounts Best Checking Accounts Best No Fee Checking Accounts Best Teen Checking Accounts Best Student Checking Accounts Best Joint Checking Accounts Best Business Checking Accounts Best Free Checking Accounts

- Savings Best High-Yield Savings Accounts Best Free No-Fee Savings Accounts Simple Savings Calculator Monthly Budget Calculator: 50/30/20

- Mortgages Best Mortgage Lenders Best Online Mortgage Lenders Current Mortgage Rates Best HELOC Rates Best Mortgage Refinance Lenders Best Home Equity Loan Lenders Best VA Mortgage Lenders Mortgage Refinance Rates Mortgage Interest Rate Forecast

- Personal Loans Best Personal Loans Best Debt Consolidation Loans Best Emergency Loans Best Home Improvement Loans Best Bad Credit Loans Best Installment Loans For Bad Credit Best Personal Loans For Fair Credit Best Low Interest Personal Loans

- Student Loans Best Student Loans Best Student Loan Refinance Best Student Loans for Bad or No Credit Best Low-Interest Student Loans

- Business Loans Best Business Loans Best Business Lines of Credit Apply For A Business Loan Business Loan vs. Business Line Of Credit What Is An SBA Loan?

- Investing Best Online Brokers Top 10 Cryptocurrencies Best Low-Risk Investments Best Cheap Stocks To Buy Now Best S&P 500 Index Funds Best Stocks For Beginners How To Make Money From Investing In Stocks

- Retirement Best Gold IRAs Best Investments for a Roth IRA Best Bitcoin IRAs Protecting Your 401(k) In a Recession Types of IRAs Roth vs Traditional IRA How To Open A Roth IRA

- Business Formation Best LLC Services Best Registered Agent Services How To Start An LLC How To Start A Business

- Web Design & Hosting Best Website Builders Best E-commerce Platforms Best Domain Registrar

- HR & Payroll Best Payroll Software Best HR Software Best HRIS Systems Best Recruiting Software Best Applicant Tracking Systems

- Payment Processing Best Credit Card Processing Companies Best POS Systems Best Merchant Services Best Credit Card Readers How To Accept Credit Cards

- More Business Solutions Best VPNs Best VoIP Services Best Project Management Software Best CRM Software Best Accounting Software

- Manage Topics

- Investigations

- Visual Explainers

- Newsletters

- Abortion news

- Coronavirus

- Climate Change

- Vertical Storytelling

- Corrections Policy

- College Football

- High School Sports

- H.S. Sports Awards

- Sports Betting

- College Basketball (M)

- College Basketball (W)

- For The Win

- Sports Pulse

- Weekly Pulse

- Buy Tickets

- Sports Seriously

- Sports+ States

- Celebrities

- Entertainment This!

- Celebrity Deaths

- American Influencer Awards

- Women of the Century

- Problem Solved

- Personal Finance

- Small Business

- Consumer Recalls

- Video Games

- Product Reviews

- Destinations

- Airline News

- Experience America

- Today's Debate

- Suzette Hackney

- Policing the USA

- Meet the Editorial Board

- How to Submit Content

- Hidden Common Ground

- Race in America

Personal Loans

Best Personal Loans

Auto Insurance

Best Auto Insurance

Best High-Yields Savings Accounts

CREDIT CARDS

Best Credit Cards

Advertiser Disclosure

Blueprint is an independent, advertising-supported comparison service focused on helping readers make smarter decisions. We receive compensation from the companies that advertise on Blueprint which may impact how and where products appear on this site. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Blueprint. Blueprint does not include all companies, products or offers that may be available to you within the market. A list of selected affiliate partners is available here .

Travel Insurance

Best travel insurance companies of April 2024

Amy Fontinelle

Heidi Gollub

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

Updated 3:40 a.m. UTC April 1, 2024

- path]:fill-[#49619B]" alt="Facebook" width="18" height="18" viewBox="0 0 18 18" fill="none" xmlns="http://www.w3.org/2000/svg">

- path]:fill-[#202020]" alt="Email" width="19" height="14" viewBox="0 0 19 14" fill="none" xmlns="http://www.w3.org/2000/svg">

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy .

WorldTrips is the best travel insurance company of 2024, based on our analysis of cost and coverage options. Use this rating to compare top travel insurance plans and find the best match for your next trip.

Best travel insurance companies of 2024

- WorldTrips: Best travel insurance .

- Travel Insured: Best for emergency evacuation .

- TravelSafe: Best for missed connections .

- Aegis: Best for traveling with a pet .

- Travelex: Best for traveling with kids .

- AIG: Best for add-on coverage options .

- Nationwide: Best for cruise itinerary changes .

Why trust our travel insurance experts

Our travel insurance experts evaluate hundreds of insurance products and analyzes thousands of data points to help you find the best product for your situation. We use a data-driven methodology to determine each rating. Advertisers do not influence our editorial content. You can read more about our methodology below.

- 1,855 coverage details evaluated.

- 567 rates reviewed.

- 5 levels of fact-checking.

Travel insurance quotes comparison

Top-rated travel insurance companies , best travel insurance.

Top-scoring plans

Medical limit per person, medical evacuation limit per person, what you should know.

Two WorldTrips plans top our rating of the best travel insurance: Atlas Journey Preferred and Atlas Journey Premier.

The Preferred plan is more affordable and provides $100,000 per person in emergency medical benefits as secondary coverage, with an optional upgrade to primary coverage. Atlas Journey Preferred is also the best travel insurance for cruises .

For a little extra, you can buy the Premier plan, which gives you $150,000 in travel medical insurance with primary coverage. This is a good option if health insurance for international travel is a priority.

Pros and cons

- Atlas Journey Preferred is the cheapest of the 5-star travel insurance plans.

- Atlas Journey Premier has $150,000 in primary medical coverage.

- Both plans have top-notch $1 million per person in medical evacuation coverage.

- Each plan includes travel inconvenience coverage of $750 per person.

- 12 optional upgrades, including destination wedding and rental car damage and theft.

- No non-medical evacuation coverage.

Best for emergency evacuation

Travel insured.

Top-scoring plan

Travel Insured Worldwide Trip Protector travel insurance offers $1 million in emergency evacuation coverage per person and $150,000 in non-medical evacuation per person. It also has primary coverage for travel medical insurance benefits. If you’re looking for the best travel insurance for international travel, consider the Worldwide Trip Protector plan.

- Only plan in our rating that offers $150,000 in non-medical evacuation coverage.

- $500 per person baggage delay benefit only requires a 3-hour delay.

- Optional rental car damage benefit up to $50,000.

- Missed connection benefit of $500 per person only available for cruises and tours.

Best for missed connections

If you’re worried that missed connections could disrupt your trip, it’s worth considering TravelSafe. Some travel insurance companies only provide missed connection coverage for cruises and tours, but TravelSafe doesn’t impose that restriction.

- Best-in-class $2,500 per person in missed connection coverage.

- $1 million per person in medical evacuation and $25,000 in non-medical evacuation coverage.

- Generous $2,500 per person baggage and personal items loss benefit.

- Most expensive of the top-scoring travel insurance plans.

- No “interruption for any reason” coverage available.

- Weak baggage delay coverage of $250 per person after 12 hours.

Best for traveling with a pet

Go Ready Choice by Aegis has the most affordable travel insurance of the top-scoring companies in our rating. It offers basic coverage limits with optional add-ons, such as a Pet Bundle that includes pet medical, pet kennel and pet return benefits.

- Cheapest of the top-scoring travel insurance plans.

- Optional pet bundle adds pet medical expense and pet return benefits.

- Low emergency medical and evacuation limits.

- Low missed connection benefit of $500 per person for cruises and tours only.

- Low baggage and personal items loss benefit of $500 per person.

Best for traveling with kids

If you’re traveling with children age 17 or younger, you’ll appreciate not having to pay extra for their coverage when you buy a Travel Select plan from Travelex Insurance Services.

- Free coverage for children 17 and under on the same policy.

- Robust travel delay coverage of $2,000 per person ($250 per day) after 5 hours.

- Hurricane and weather coverage after a common carrier delay of any amount of time.

- Low emergency medical coverage of $50,000 per person.

- Non-medical evacuation is not included.

- Low baggage delay coverage of $200 requires a 12-hour delay.

Best for add-on coverage options

Travel Guard Preferred from AIG allows you to customize your policy with a host of optional upgrades. These include “cancel for any reason” (CFAR) coverage , rental vehicle damage coverage and bundles that offer additional benefits for adventure sports, travel inconvenience, quarantine, pets, security and weddings.

There’s also a medical bundle that increases the travel medical benefit to $100,000 and emergency evacuation to $1 million. This is a good option if you’re looking for foreign travel health insurance.

- Bundle upgrades allow you to customize your travel insurance policy.

- Emergency medical and evacuation limits can be doubled with optional upgrade.

- Base travel insurance policy has relatively low medical limits.

- $300 baggage delay benefit requires a 12-hour delay.

- Optional CFAR upgrade only reimburses up to 50% of trip cost.

Best for cruise itinerary changes

Evacuation limit per person

Nationwide’s Cruise Choice plan has a $500 per person benefit if a cruise itinerary change causes you to miss a prepaid excursion. It also has a missed connections benefit of $1,500 per person after only a 3-hour delay, when you’re taking a cruise or tour. But note that this coverage is secondary coverage to any compensation provided by a common carrier.

- Benefits for cruise itinerary changes, ship-based mechanical breakdowns and covered shipboard service disruptions.

- Non-medical evacuation benefit of $25,000 per person.

- Missed connection coverage of $1,500 per person for tours and cruises, after a 3-hour delay.

- Baggage loss benefits of $2,500 per person.

- Travel medical coverage is secondary.

- Trip cancellation benefit for losing your job requires three years of continuous employment.

- No “cancel for any reason” upgrade available.

Compare the best travel insurance companies of 2024

Methodology

Our travel insurance experts reviewed 1,855 coverage details and 567 rates to determine the best travel insurance of 2024. For companies with more than one travel insurance plan, we shared information about the highest-scoring plan.

Insurers could score up to 100 points based on the following factors:

- Cost: 40 points. We scored the average cost of each travel insurance policy for a variety of trips and traveler profiles.

- Medical expenses: 10 points. We scored travel medical insurance by the coverage amount available. Travel insurance policies with emergency medical expense benefits of $250,000 or more per person were given the highest score of 10 points.

- Medical evacuation: 10 points. We scored each plan’s emergency medical evacuation coverage by coverage amount. Travel insurance policies with medical evacuation expense benefits of $500,000 or more per person were given the highest score of 10 points.

- Pre-existing medical condition exclusion waiver: 10 points. We gave full points to travel insurance policies that cover pre-existing medical conditions if certain conditions are met.

- Missed connection: 10 points. Travel insurance plans with missed connection benefits of $1,000 per person or more received full points.

- “Cancel for any reason” upgrade: 5 points. We gave points to travel insurance plans with optional “cancel for any reason” coverage that reimburses up to 75%.

- Travel delay required waiting time: 5 points. We gave 5 points to travel insurance policies with travel delay benefits that kick in after a delay of 6 hours or less.

- Cancel for work reasons: 5 points. If a travel insurance plan allows you to cancel your trip for work reasons, such as your boss requiring you to stay and work, we gave it 5 points.

- Hurricane and severe weather: 5 points. Travel insurance plans that have a required waiting period for hurricane and weather coverage of 12 hours or less received 5 points.

Some travel insurance companies may offer plans with additional benefits or lower prices than the plans that scored the highest, so make sure to compare travel insurance quotes to see your full range of options.

What does travel insurance cover?

Travel insurance covers your prepaid, nonrefundable trip costs — as well as extra money you may need to spend due to unforeseen circumstances and emergencies — both before and during your trip.

Travel insurance coverage varies by plan, but in general travel insurance covers costs associated with these problems:

- Bankruptcy of a travel company, such as your airline or tour operator.

- Dangerous weather conditions .

- Delayed and lost luggage.

- Illness or death in your family that requires you to stay home or cut your trip short.

- Illness that needs medical attention.

- Injury requiring medical evacuation.

- Jury duty.

- Travel delays and missed connections.

- Theft of your personal belongings while traveling.

- Unexpected job loss.

A comprehensive travel insurance plan bundles several types of travel insurance coverage, each with its own limits. To ensure you have adequate financial protection for your trip, your travel insurance policy should include the following travel insurance coverages.

Trip cancellation insurance

As soon as you buy a travel insurance plan that includes trip cancellation insurance , you’re covered if you need to call off your trip because of a reason listed in your policy. These reasons generally include unexpected illness, injury or death of you, a family member or a travel companion, severe weather, jury duty and your travel supplier going out of business.

If you cancel your trip for a covered reason, you can expect to be reimbursed for 100% of your prepaid, nonrefundable travel expenses.

For even greater flexibility, some travel insurance plans offer a “ cancel for any reason ” (CFAR) upgrade. This optional coverage allows you to pull the plug on your trip for any reason at all, as long as you do so at least 48 hours before your scheduled departure.

Adding CFAR coverage will increase the cost of your plan and it’s important to note that this coverage typically only reimburses 50% or 75% of your expenses, depending on the policy.

Travel delay insurance

Once your trip is underway, inconvenient delays can be expensive. Travel delay insurance reimburses you for unexpected expenses you incur after a certain waiting period, such as five hours. If your travel is delayed longer than that time because of a reason in your policy, such as severe weather, your benefits can cover needs like airport meals, transportation and even overnight accommodation.

This coverage usually has daily limits as well as a maximum limit. For example, a travel insurance plan may provide trip delay coverage of up to $150 per day with a $2,000 maximum.

Trip interruption insurance

If you need to end your trip early — again, for a reason listed in your policy — trip interruption insurance comes into play.

Say a close family member back home is involved in an accident and you need to rush back to be by their side. Trip interruption benefits can reimburse you for any prepaid, nonrefundable payments you’ll lose by leaving early. It can also pay for a last-minute one-way ticket home.

Travel medical insurance

Emergency medical benefits are especially important if you need international health insurance for travel outside of the country. Your domestic health insurance may provide limited coverage once you leave the U.S.

The best senior travel insurance provides ample travel medical coverage because Medicare does not cover health care outside of the U.S., except in very limited circumstances.

The best travel medical insurance pays for ambulance service, doctor visits, hospital stays, X-rays, lab work and prescription medication you may require while traveling.

Many travel insurance plans cover medical treatment for COVID-19, but not all do. The best COVID travel insurance has generous emergency medical and emergency medical evacuation benefits.

When comparing plans to find the best medical travel insurance for international trips, check to see if the coverage is primary. If the travel medical insurance coverage is secondary, you will need to file a claim with your health insurance before you can file a travel insurance claim.

Emergency medical evacuation

If you’re traveling to a remote area, or planning excursions such as boating to an island, emergency medical evacuation coverage is a good idea. This coverage pays to transport you to the nearest adequate medical facility if you are injured or sick while traveling.

Depending on your location and medical condition, emergency transportation could cost tens of thousands of dollars. Our top-scoring travel insurance plans all offer coverage of $1 million.

Baggage delay coverage

If you arrive safely at your destination but your bags do not, this coverage can help. After a certain waiting period, such as six or 12 hours, this coverage will reimburse you for necessities you may need while waiting for your bags to arrive. Be sure to save your receipts and look at your coverage limit, as some caps are low, like $200.

Baggage loss and personal effects coverage

Baggage insurance can reimburse you if your bag never arrives, or if your personal belongings are stolen during your travels. Coverage limits apply here, as well as exclusions for certain items such as electronics. If you’ll be traveling with your laptop or other valuables, read your policy carefully to make sure they’re covered.

What travel insurance doesn't cover

Travel insurance policies often exclude or limit “foreseeable” losses. Typical travel insurance exclusions include:

- Accidents or injuries caused by drinking or drug use.

- Canceling your trip because you changed your mind.

- Ending your trip early because you changed your mind.

- Losses caused by intentional self harm, including suicide.

- Losses due to war, civil disorder or riots.

- Medical tourism.

- Medical treatment for pre-existing conditions.

- Mental health care.

- Natural disasters that begin before you buy travel insurance.

- Non-medical evacuation.

- Normal pregnancy.

- Medical treatment related to high-risk activities.

- Routine medical care, such as physicals or dental care.

- Search and rescue.

Most travel insurance companies offer a free look period when you buy a policy. Take this time — which might be anywhere from 10 to 21 days — to carefully review the plan’s coverages and exclusions, and request a full refund if it doesn’t meet your needs.

“For trip cancellation coverage, travel insurance plans will only cover you for very specific covered reasons listed in a plan’s description of coverage,” said Stan Sandberg, co-founder and CEO of TravelInsurance.com. “If an event is not listed as a covered reason, it won’t be covered unless the consumer opts for a ‘cancel for any reason’ policy.”

“Cancel for any reason travel insurance” upgrade

For the greatest flexibility to cancel, consider adding “cancel for any reason” (CFAR) coverage to your travel insurance plan. This will increase the cost of your policy, but will typically reimburse you for 75% of your trip expenses if you decide to cancel your trip.

A CFAR upgrade also usually has a number of requirements, such as buying it within seven to 14 days of making your first trip payment and insuring the full amount of your travel costs. But, it will give you the freedom to cancel your trip for any reason, as long as you do so at least two days before your scheduled departure.

Adding CFAR coverage typically increases the cost of your travel insurance plan by 50%.

Make sure you’re covered: Best COVID travel insurance

How much travel insurance should I buy?

Travel insurance companies typically offer several plans with varying maximum limits. The higher the coverage limits, the more you’ll pay for travel insurance.

Squaremouth recommends the following coverage limits for international travel:

- Emergency medical coverage: At least $50,000.

- Medical evacuation coverage: At least $100,000.

If you’re going on a cruise, or to a remote location, Squaremouth recommends:

- Emergency medical coverage: At least $100,000.

- Medical evacuation coverage: At least $250,000.

When evaluating travel insurance plans, our team of insurance analysts considered the best medical travel insurance to be policies with at least $250,000 in emergency medical coverage and at least $500,000 in medical evacuation coverage.

What is the best travel insurance?

The best travel insurance for international travel is sold by WorldTrips , according to our analysis. Two WorldTrips plans — Atlas Journey Preferred and Atlas Journey Premier — top our rating of the best travel insurance. But the best travel insurance for you depends on the trip you are planning and the coverage areas that are most important to you.

Make sure you’re covered: WorldTrips travel insurance review

Best travel insurance for cruises

The best cruise travel insurance is WorldTrips Atlas Journey Preferred. This plan offers solid travel insurance for cruises for a low rate.

Best travel insurance for COVID

The best COVID travel insurance is the Trip Protection Basic plan sold by Seven Corners . It is a relatively low cost travel insurance plan with optional “cancel for any reason” coverage that reimburses up to 75% of your prepaid, nonrefundable trip expenses.

Best travel insurance for “cancel for any reason”

The best cancel for any reason (CFAR) travel insurance is Seven Corners Trip Protection Basic. Adding CFAR coverage to a RoundTrip Basic plan only increases the cost by about 40%, which is lower than other plans we analyzed. For the extra cost, you get coverage of 75% of your prepaid, nonrefundable trip expenses, as long as you cancel at least 48 hours before your scheduled departure.

Best travel insurance for seniors

The best senior travel insurance is the Gold plan sold by Tin Leg . It is an affordable plan with travel medical primary coverage of $500,000 and a pre-existing conditions waiver if you insure the full amount of your trip within 14 days of your first trip deposit.

How much is travel insurance?

The average travel insurance cost is 5% to 6% of your trip costs.

How much you pay for travel insurance will depend on how expensive your trip is, how many benefits the insurance provides and the age of the covered travelers.

Here are average costs per trip by travel insurance plan, based on our analysis of rates.

Travel insurance cost examples

Average travel insurance costs are based on rates for seven trips with a variety of traveler ages, trip costs and destinations. Travel insurance plans have different levels of included benefits, which can account for price differences.

What affects travel insurance costs?

How much you pay for travel insurance will depend on:

- The cost of your trip.

- Your destination.

- The length of your trip.

- The ages of travelers being insured.

- Your state of residence.

- The travel insurance policy you choose.

- The total coverage amounts in your policy.

- Any travel insurance add-ons you select.

How travel insurance works

“Typically, travelers are expected to pay their expenses out of pocket, and then file a claim for reimbursement,” said Clark. “However, there are medical situations in which a provider may be required to pre-authorize payment to make sure the policyholder receives the treatment they need.”

According to Clark, “Providers can pre-authorize payment for medical care and emergency evacuations. With that said, every circumstance is unique, and providers will handle each situation on a case-by-case basis.”

How to get travel insurance

To buy travel insurance, you’ll need to submit an online application with information about yourself and your trip, such as your name, age, permanent address, destination, travel dates and total trip cost per person. Since the application is simple, you can easily get quotes from multiple companies on your own.

Even easier, you can get multiple quotes by submitting a single application online through a travel insurance comparison site like Squaremouth.

How to choose which travel insurance is best for you

When shopping for travel insurance, consider the coverages that are most important to you. For example:

- Travel medical insurance. If you need travel health insurance for international travel, you’ll want a high limit for medical expenses, such as doctor and hospital bills, ambulance, X-rays and medicine. The best travel insurance for seniors includes ample travel medical insurance because Medicare generally does not pay for health care outside of the U.S.

- Emergency medical evacuation. If you’re planning a trip to a remote destination, make sure your travel insurance plan has high limits for emergency evacuation. Squaremouth suggests $50,000 to $100,000 of medical evacuation coverage for most trips but recommends $250,000 for travel to remote locations.

You’ll also want to consider common exclusions , such as:

- Adventure sports. Many travel insurance plans exclude coverage for risky activities such as skiing and scuba diving. Read the fine print of a policy to see what is excluded, or look for a travel insurance company that specializes in covering adventure sports trips, such as World Nomads.

- Named storms. If a hurricane is named before you buy travel insurance, it’s too late to buy coverage and cancel your trip because of the storm.

- Normal pregnancy. Normal pregnancy typically isn’t covered by travel insurance. If you get pregnant after you buy travel insurance, you may be covered for pregnancy-related reasons, but you’ll need to provide medical proof that pregnancy started after your purchased travel insurance.

- Pre-existing medical conditions. If you have dealt with a health issue — even allergies or asthma — look closely at this common exclusion. Travel insurance plans typically have look-back periods, which could be 60, 90 or 180 days before you bought the policy. If you had symptoms during that time, your claim could be denied if your condition flares up while you’re traveling. If you’re shopping for the best travel insurance for pre-existing conditions, look for plans that offer a pre-existing medical condition waiver. You’ll be eligible for this waiver if you meet specific terms, such as buying travel insurance within days of making your first trip deposit and insuring the full value of your trip.

When to buy travel insurance

The best time to buy travel insurance is immediately after making your first nonrefundable travel payment, whether it’s for a plane ticket, hotel stay, cruise or excursion. Like other types of insurance, your policy needs to be in place before something goes wrong. It won’t cost you any extra to buy travel insurance far in advance of your trip, and it will cover a longer period of time.

“Purchasing a travel insurance policy at the time of making an initial trip payment offers travelers the most peace of mind,” said James Clark, spokesperson for Squaremouth.

“Knowing they are protected if unforeseen events such as medical emergencies, inclement weather, natural disasters and other trip disruptions occur allows travelers to approach their trip with less worry and more confidence.”

You’d have a hard time buying travel insurance before booking anything because you’d have nothing to insure, Clark said. “With that said, travelers are able to purchase a policy and make modifications, such as updating travel dates or adding expenses to the insurance policy, as they continue to make their travel arrangements.”

You can buy travel insurance up to the day before you leave on your trip, but waiting may cost you the opportunity to qualify for a pre-existing condition waiver or to buy a “cancel for any reason” upgrade.

Where to buy travel insurance

You can buy a travel insurance plan:

- Online. Visit a travel insurance company’s website to buy a policy directly or use a comparison website like Squaremouth to see your options and compare plans. You may also be able to purchase travel insurance online through an airline, cruise, hotel, rental car company or other provider you book a ticket with.

- In person. A travel agent or insurance agent may be able to assist you in buying travel insurance.

Using a travel insurance marketplace that will give you quotes for multiple policies is a great way to compare coverage options and pricing to find the best policy for your trip. Buying a policy directly from a travel provider is convenient and might be fine, but it might not meet your needs.

“If a traveler is heading to the Caribbean with the intention of going scuba diving, it’s unlikely that the policy offered by the airline would cover that activity,” Clark said. “Shopping around for insurance opens the door to other policy providers that may offer a policy that checks all of a traveler’s boxes.”

In addition, while flight insurance , which may be offered through a partnership with a travel insurance provider like AIG or Allianz, may cover travel delays and cancellations, it might not protect you if you get sick during your trip, Clark said. “We highly recommend travelers read the policy’s fine print before making a purchase so they know what’s covered,” he added.

Top 10 travel destinations

Americans are changing the way they travel and this includes buying travel insurance when they might have skipped it in the past.

Here are the top destinations travel insurance customers are traveling to — and how much they’re spending on these trips — according to Feb. 2024 data from Squaremouth.

Source: Squaremouth. Based on travel insurance purchased from Jan. 14 to Feb. 13, 2024.

Travel insurance trends in 2024

Here are some key travel insurance trends in 2024:

- As spending on trips continues to rise , so will the price of travel insurance policies.

- People are planning trips further in advance and purchasing 2024 travel insurance earlier, making them eligible for perks like cancel for any reason (CFAR) coverage and a pre-existing conditions exclusion waiver.

- Emergency evacuation, medical coverage and trip interruption remain top concerns for travelers, increasing the search for comprehensive travel insurance plans with more robust coverage — even if it costs more.

“As Americans continue to spend more on vacations, they have more to lose if they need to cancel or return home early. A travel insurance policy is an efficient and cost-effective way to protect that financial investment for trips in 2024,” said InsureMyTrip senior vice president Suzanne Morrow.

Best travel insurance FAQs

WorldTrips has the best trip insurance, according to our analysis. Two of its plans — Atlas Journey Preferred and Atlas Journey Premier — get 5 stars in our rating.

The best travel insurance policy for you will depend on what type of coverage you need. With so many different policies and carriers, the policy that was best for your friend’s trip to California might not be ideal for your trip to Japan. If you’re looking for the best travel insurance for international travel, you may be willing to pay more for higher coverage levels.

Your U.S. health insurance may provide little or no coverage in foreign countries. Check with your health insurance company to see if you have any global benefits and ask how they work. If your health care does extend across the border, the benefits it provides abroad may not be the same benefits it provides domestically.

Medicare usually won’t pay for health care outside of the United States and its territories, so older travelers planning an international trip should look into the best senior travel insurance with robust medical benefits.

The best time to buy travel insurance is immediately after booking your trip and making a nonrefundable payment — in other words, as soon as you’re at risk of losing money. This way, you’ll know the total cost that you need to insure and you’ll have the longest window to take advantage of your policy’s benefits if something goes wrong.

You can’t wait until something goes wrong and then buy travel insurance to get reimbursed for your loss. Travel insurance only covers unexpected losses.

Travel insurance companies can decline to cover travel to certain countries. For example, you may find that some trip insurance companies don’t offer coverage to countries with a Level 4: Do Not Travel advisory from the U.S. State Department.

Travel insurance policies also frequently exclude certain risks that you’re more likely to encounter in Level 4 or Level 3 countries. For example, your policy may not cover losses related to declared or undeclared wars or acts of war or losses related to known or foreseeable conditions or events.

Some credit cards , such as the Chase Sapphire Preferred® Card , offer benefits such as trip cancellation and interruption insurance, baggage delay insurance and trip delay reimbursement when you use your card to pay for your trip.

Ask your credit card issuer for your card’s benefits guide to see what coverage you may have. Keep in mind that it may not cover all the risks you want to protect against, such as the cost of international health care or emergency medical evacuation .

Business travel insurance makes sense if you are self-employed and paying for your own travel expenses, or if you are traveling internationally and want medical coverage abroad.

You might also consider buying travel insurance for a business trip if your company won’t cover extra expenses if your flight is delayed or you need to head home early.

Cruise travel insurance can help protect you financially if you need emergency medical care in a remote location, or if a delayed flight causes you to miss embarkation and you need to pay extra to catch up to your cruise.

Experts caution that travel insurance you buy through a cruise line may not be as comprehensive as plans you can buy directly from travel insurance companies.

Some travel insurance plans cover rental cars as an optional upgrade, for an additional cost. The 5-star rated travel insurance companies in our rating offer these optional rental car benefits:

- Travel Insured International — Rental car damage and theft coverage of $50,000.

- WorldTrips — Rental car damage and theft coverage of $50,000 with a $250 deductible.

Travel insurance typically only covers a single trip, although your insured trip can have multiple destinations.

If you’re looking to insure several trips in the same year, annual travel insurance may be a good option for you.

Editor’s Note: This article contains updated information from previously published stories:

- Spirit Airlines scrubs 60% of its Wednesday flights, says cancellations will drop ‘in the days to come.’

- ‘Just a parade of incompetency’: Spirit Airlines passengers with ‘nightmare’ stories want more than apology, $50 vouchers

- ‘This is not our proudest moment’: Spirit Airlines CEO says more flight cancellations expected this weekend

- Hurricane Irma: Flight cancellations top 12,500; even more expected

- Is an annual travel insurance policy right for you?

- How 2020 and COVID-19 changed travel forever – and what that means for you

- COVID-19 or delta variant have you ready to scrap your trip? Here’s how to cancel like a pro

- Sunday: Snow is over, but flight cancellations top 12,000

- After nearly 13,000 Harvey cancellations, Irma is new threat to airline flights

- What’s the difference between travel insurance and trip ‘protection’?

- How to choose the right travel insurance for your next vacation

- Travel insurance can save the day

- Angry passengers brawl after Spirit cancels flights

- What to do when travel insurance doesn’t work

- How lockdowns, quarantines and COVID-19 testing will change summer travel in 2021

- Travelers will pay and worry more on summer vacation this year. But they won’t cancel

- How to find a hotel with COVID testing and quarantine facilities wherever you travel

- Yearning to travel in 2022? First, figure out your budget – then pick a destination

- Pro tips for surviving a long flight during a pandemic: Get the right mask, bring a pillow

- Want to steer clear of contracting COVID-19 on your next vacation? Follow these guidelines

- Post-pandemic travel: Is it OK to ask another passenger’s vaccine status or request they mask up?

- These days, forgetting these important travel items could cost you thousands of dollars

- International travel hacks: When to book flights and hotels, how to deal with COVID-19 rules

- Traveling post-coronavirus: How do you book your next trip when so much remains uncertain?

- The COVID-19 guide to holiday travel – and the case for why you shouldn’t go this year

- Should you travel during the holidays? Americans struggle with their decision

- ‘There’s still pent-up demand’: What you should know about fall travel

- Planning for life after coronavirus: When will we know it’s safe to travel again?

- ‘Busiest camping season’: Travelers choose outdoor recreation close to home amid COVID-19 pandemic

- Considering a camping trip this summer? Tips to make sure your gear is good to go

- RVing for the first time? 8 tips for newbies I wish I’d known during my first trip

- Five myths about travel agents

- Should I buy travel insurance?

- Is travel insurance stacked against you?

- Five myths about travel insurance and terrorism

- These eight things could get your travel insurance claims rejected

- There’s a good chance that your credit card already gives you some kind of travel insurance coverage

- How to avoid a hotel cancellation penalty

- Change fees and travel insurance continue to rise

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy . The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.

Amy Fontinelle has more than 15 years of experience helping people make informed decisions about their money, whether they’re refinancing a mortgage, buying insurance or choosing a credit card. As a freelance writer trained in journalism and specializing in personal finance, Amy digs into the details to explain the products and strategies that can help (or hurt) people seeking greater financial security and wealth. Her work has been published by Forbes Advisor, Capital One, MassMutual, Investopedia and many other outlets.

Heidi Gollub is the USA TODAY Blueprint managing editor of insurance. She was previously lead editor of insurance at Forbes Advisor and led the insurance team at U.S. News & World Report as assistant managing editor of 360 Reviews. Heidi has an MBA from Emporia State University and is a licensed property and casualty insurance expert.

10 worst US airports for flight cancellations this week

Travel Insurance Heidi Gollub

10 worst US airports for flight cancellations last week

Average flight costs: Travel, airfare and flight statistics 2024

Travel Insurance Timothy Moore

John Hancock travel insurance review 2024

Travel Insurance Jennifer Simonson

HTH Worldwide travel insurance review 2024

Airfare at major airports is up 29% since 2021

USI Affinity travel insurance review 2024

Trawick International travel insurance review 2024

Travel insurance for Canada

Travel Insurance Mandy Sleight

Travelex travel insurance review 2024

Best travel insurance for a Disney World vacation in 2024

World Nomads travel insurance review 2024

Outlook for travel insurance in 2024

Survey: Nearly 85% of Americans avoid family over the holidays

Travel Insurance Kara McGinley

AIG travel insurance review 2024

I'm a financial planner, and I'd recommend annual travel insurance to anyone who loves to travel abroad

Affiliate links for the products on this page are from partners that compensate us (see our advertiser disclosure with our list of partners for more details). However, our opinions are our own. See how we rate insurance products to write unbiased product reviews.

- Frequent and spontaneous travelers will likely benefit from annual travel insurance policies.

- Your credit card may come with some travel protections, but it may not be enough.

- When choosing a policy, look at what it covers, not just what's cheapest.

Summer is just a few months away — and if you're planning a vacation this year, the last thing you want is an unexpected event to derail your plans (and cost you hundreds).

Flights get delayed or canceled constantly. Luggage disappears into the ether. Medical emergencies occur in remote destinations. Yet many jetsetters simply cross their fingers and hope for the best rather than prepare for the worst.

That's why, as a financial planner, I believe it's crucial to consider protecting your trips with the right insurance coverage. One option often overlooked, particularly by frequent travelers, is annual travel insurance .

Annual travel insurance covers all your trips within 365 days. Unlike stand-alone travel insurance, which only covers you for a specific trip, an annual policy covers any trips you take within the year.

That's why I tell clients who travel frequently that an annual policy is a good choice for their needs. By opting for an annual plan, you don't have to go through the hassle of booking multiple policies and potentially save money compared to purchasing individual trip coverage. Here's how it works.

What to look for in a policy

While specifics may vary depending on the insurer and plan tier, most include the following key benefits:

- Trip cancellations or interruptions: You may be able to get reimbursed for expenses (even nonrefundable ones!) related to an illness, injury, or natural disaster that forced you to cancel or cut your trip short.

- Emergency medical and dental care: If you fall ill or get injured while traveling, your insurance can help cover the cost of medical treatment.

- Emergency evacuation: In a serious medical emergency or security situation, your policy will arrange and pay for transportation to a hospital or back to your home country.

- Lost, delayed, or damaged baggage: If your luggage is lost, delayed, or damaged during your trip, you can get financial coverage for essential items while you wait for your stuff to be recovered or replaced.

- Trip delays and missed connections: When your travel plans are disrupted due to issues like mechanical problems or severe weather, you may get reimbursement for additional expenses incurred, like meals, lodging, and transportation.

It's important to note that annual travel insurance plans have limitations. Certain high-risk activities, pre-existing medical conditions, and travel to specific regions may be restricted or require additional coverage.

Some travelers may assume that their credit card's built-in travel protections are enough. While many travel rewards credit cards offer perks like rental car insurance, trip cancellation, and baggage reimbursement, the coverage limits are often much lower than a dedicated annual travel insurance plan.

Credit card coverage for emergency medical care is also particularly limited — capped at a few thousand dollars — which may not be enough in the face of a major international medical emergency.

How much travel justifies an annual plan?

For the occasional traveler who takes one or two trips a year, single-trip policies will probably work for you. But if you fall into any of these buckets, you may want to consider an annual policy:

- Regular international travelers (three or more trips abroad yearly)

- Road warriors frequently away for work

- Adventurers engaging in high-risk activities like heli-skiing, scuba diving, or mountain climbing

- Cruisers and tour group travelers

- Students or retirees taking extended trips throughout the year

- Those visiting developing countries with limited medical care

Annual plans cover all of your trips within a 365-day period after purchasing. They're basically a bundle of multiple policies into one package deal. This means you only have to buy one policy to manage, locking in your coverage for the year.

How to decide if an annual policy makes sense for you

Start by reviewing your travel plans this year — and your risk tolerance. Calculate how much buying individual travel insurance policies would cost you over the next year and compare it to the price of an annual plan.

Don't just focus on the premium — carefully evaluate coverage limits, exclusions, and deductibles to ensure you have enough protection for your needs.

An annual policy gives you the flexibility to take spontaneous trips without the hassle of obtaining last-minute insurance. More importantly, it provides peace of mind, knowing that you're covered for a wide range of travel disruptions and emergencies.

As the busy summer travel season ramps up, definitely explore protecting your trips with insurance, especially if you're jetting off internationally. Spending hours on the phone trying to rebook canceled flights or worrying about affording an overseas medical emergency is no way to vacation.

- Main content

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

Best Travel Insurance for Visiting the U.S.

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

Table of Contents

Travel insurance basics

Best visitors insurance policies, for the lowest price: trawick international, for customizing options: worldtrips, for pre-existing conditions: worldtrips, for highest medical coverage limit: img, other options to consider, the bottom line.

Since health care can be expensive in the U.S., it’s important that visitors have insurance coverage, aka visitors insurance or travel medical insurance, in case something happens that requires medical attention mid-trip.

Whether you have coverage for travel in the U.S. depends on your health care plan in your home country. But if you don't, you'll need to buy a policy from a third-party insurance provider. Several companies sell this kind of visitor insurance, and each company and policy is a bit different. Let’s look at which is best for you.

First, a few basics about visitor insurance. Two kinds are available: travel medical insurance and trip insurance.

Travel medical insurance covers medical expenses that you may incur while traveling internationally, like a visit to the doctor, a trip to the hospital and medical evacuation and repatriation.

Trip insurance usually covers limited medical expenses like emergency care and can compensate you if your trip is delayed, you need to leave the trip early or you have to cancel the trip. It is designed to help you protect the investment you’re making as you prepare to travel.

Standard trip insurance might not cover a visit to the doctor unless it is an emergency.

It’s important to make sure any pre-existing conditions are covered if the visitor has any. Some policies exclude them.

» Learn more: How to find the best travel insurance

With so many kinds of visitors insurance policies, which is the best?

To make comparisons, we got quotes from several companies using Squaremouth , a website to search for different types of travel insurance in one place.

The parameters we set are for a 49-year-old citizen and resident of Spain traveling to the U.S. on May 1-31, 2024.

The quotes don't include cancellation coverage; these examples are for medical coverage only. To get a quote, the hypothetical deposit for the trip was paid on Feb. 15.

Since we’re looking for a policy that will cover medical care for visitors, there are several medical filters to select: emergency medical ($100,000 or more), medical evacuation ($100,000 or more) and coverage for pre-existing medical conditions.

The search came up with nine results ranging in price from $74.40 to $179.18.

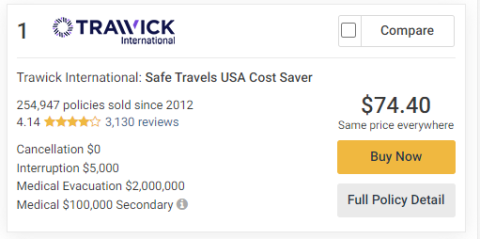

The policy with the lowest cost was the Trawick International 's Safe Travels USA Cost Saver at $74.40.

Trawick policies use the FirstHealth PPO network.

The policy as quoted has a $250 deductible and includes $100,000 in emergency medical, $2 million in medical evacuation and $5,000 in interruption coverage. It has limited coverage for pre-existing conditions.

It is possible to change the deductible to as little as $0 or raise it to $5,000.

The same company has another policy, the Trawick International Safe Travels USA Comprehensive policy, that is better at covering pre-existing conditions and costs a little more — $89.59.

The general coverage is the same as the less expensive policy, and the Safe Travels USA Comprehensive option adds coverage for acute onset of a pre-existing condition. it is possible to change the deductible amount to $0 or go up to $5,000.

» Learn more: The best travel credit cards right now

Some policies are sold as is, while others allow some flexibility depending on what is important to you.

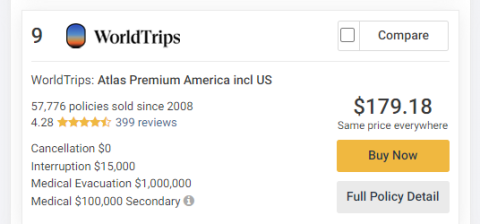

The WorldTrips Atlas Premium America policy for $179.18 allows a lot of customization.

It was also the most expensive of the nine policies Squaremouth suggested.

It’s possible to customize the emergency medical coverage and pre-existing condition coverage and medical deductible. The policy also includes $15,000 in trip interruption coverage, the highest of any of the nine policies available.

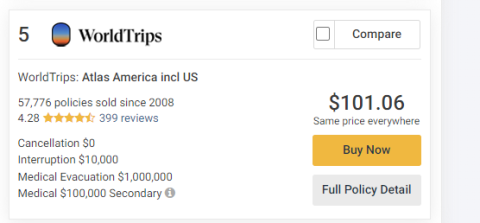

If the traveler has a pre-existing condition, policies from WorldTrips Atlas America are your best bet. The WorldTrips Atlas America policy in our comparison costs $101.06.

The policy as quoted covers $100,000 in emergency medical care and $25,000 in medical evacuation for an unexpected recurrence of a pre-existing condition.

The deductible is also available for customization from $0 to $5,000.

The PPO network for Atlas America Insurance is United Healthcare.

The WorldTrips Atlas Premium America policy mentioned above is also good for pre-existing condition coverage.

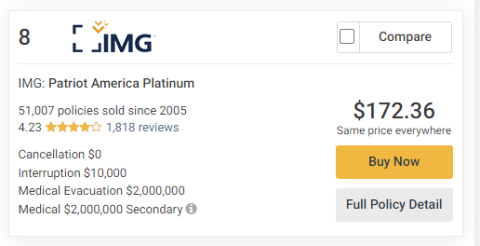

While eight of the nine policies had $100,000 in secondary medical coverage, one had a limit of $2 million.

The IMG Patriot America Platinum policy has a premium of $172.36 along with a high medical evacuation limit of $2 million and interruption coverage of $10,000.

If $2 million in medical coverage is not enough, it’s possible to increase that amount to an $8 million policy limit.

It’s not possible to change the level of coverage for preexisting conditions from the high $1 million limit in emergency medical care and $25,000 in medical evacuation for an unexpected recurrence.

It is possible to change the deductible from $0 all the way up to $25,000.

Our comparison also included policies from two additional companies, Seven Corners and Global Underwriters .

Seven Corners had two policies come up in the results, the Seven Corners Travel Medical Basic for $98.27 and the Seven Corners Travel Medical Choice policy for $136.71. Both of the Seven Corners policies include coverage for hurricane and weather, and the less expensive policy covers acts of terrorism.

Having insurance to cover unexpected medical expenses for anyone visiting the U.S. can be a smart money move.

An illness or accident could cause financial problems for visitors because of potentially having to pay for full health care costs. When planning your travel, be sure to check your current health insurance to find out if it will cover you in the U.S.

For a monthlong stay in the U.S., the lowest-priced visitors insurance policy was around $75 (Trawick International Safe Travels USA Cost Saver) and the highest was about $180 (WorldTrips Atlas Premium America). That’s about $2.42 or $5.81 a day, depending on the policy.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024 , including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-10x Earn 5x total points on flights and 10x total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3x points on other travel and dining & 1 point per $1 spent on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $900 toward travel when you redeem through Chase Travel℠.

1x-5x 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $750 when you redeem through Chase Travel℠.

1x-2x Earn 2X points on Southwest® purchases. Earn 2X points on local transit and commuting, including rideshare. Earn 2X points on internet, cable, and phone services, and select streaming. Earn 1X points on all other purchases.

50,000 Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening.

Travel Insurance

Going on holiday? Compare quotes from reputable insurers and see how much you could save with Money Expert.

Compare Travel Insurance Quotes

- Save on your Travel Insurance

- Compare offers from Reputable Insurers

- Get a quote within minutes

Whether you are jetting off for business or pleasure, travel insurance is one thing that should always be on your “to do” list. Visiting a new destination should be exciting and you shouldn’t have to worry about what might happen if your journey goes slightly pear-shaped. Travel insurance will give you peace of mind while you focus on the adventure ahead.

From arriving at your destination and discovering that your luggage has disappeared, to falling critically ill when you are in unfamiliar surroundings, travel insurance will ensure that you have all the funds you need so that a solution to each problem is easily attainable throughout your trip.

- Business Travel Insurance

- Backpacker Travel Insurance

- Group Travel Insurance

- Student Travel Insurance

- Senior Travel Insurance

Finding travel insurance quotes using our comparison tool is easy. All you need to do is provide a few details about yourself, your upcoming trip, and the policy you're after, and we'll show you a list of quotes.

To avoid the unnecessary stress of sourcing additional money up front to pay for unforeseen expenses, do your homework and compare benefits in accordance with the product price - this should be the first step towards applying for any type of insurance.

Frequently Asked Questions

What is travel insurance.

Travel insurance assists travellers by covering medical expenses and financial losses that may be incurred whilst you're away. Essentially, it allows travellers to procure good health care and other travel-related benefits while abroad. The benefits of travel insurance are typically not covered by domestic insurance plans - and this is why it is a unique product.

The length of your policy's term will typically coincide with the beginning and end of a journey i.e. from the moment you board the plane on your way to your destination to the moment you arrive back on home ground. Alternatively, continuous insurance can also be purchased that lasts a set period (e.g. a year). These policies are ideal for frequent travellers.

In South Africa, travel insurance can be purchased from travel insurance companies, banks, travel agents or directly from travel suppliers (such as cruise operators or airline companies).

Why Do I Need Travel Insurance?

If you travel without insurance, you expose yourself to the risk of amassing crippling expenses. This especially applies when you are travelling to a country with a stronger currency than your own. While you may have budgeted for your holiday, the costs that can be incurred due to medical visits can far exceed what you are capable of paying for.

Travel Insurance can provide financial protection in unexpected events where:

- Your flight is cancelled and you need to make alternative arrangements

- You become ill or injured while travelling and you need to settle foreign medical bills

- Your luggage and valuable belongings go missing or are stolen

- You need personal liability (in case you are held accountable for damaging property or causing injury)

- You need to pay for legal counsel

- You or a family member pass on and funeral expenses need to be covered

Travel insurance will allow you to travel with a greater sense of security and it addresses the gaps of your domestic insurance plan. It is a safety net that you can rely on, especially when travelling to a foreign country that has unfamiliar customs, medical facilities that you are not sure of, and you are unable to speak the language to communicate your needs effectively.

What Does Travel Insurance Cover?

Travel Insurance providers offer different benefits and features but each policy will typically cover one, more, or all of the following.

This product will keep you covered no matter where you travel in the world. You can decide whether you want your policy to cover just the basic benefits (like medical cover) or you can apply for a more comprehensive plan.

This type of cover will promise you a full or partial refund of your trip expenses if your trip is cancelled or interrupted. The reasons for cancellation must be listed in your policy and can include:

- Illness, injury or death of you or a listed family member or friend

- Hazardous weather that will prevent you from travelling

- A terrorist attack at your destination

- Flight cancellations made by the airline (you may have to rearrange accommodation if you can only get a seat on an earlier or later flight)

Most medical aids and medical insurance policies do not offer to cover the medical expenses that are incurred in a foreign country. Medical benefits are, however, built into most travel insurance policies. This means that you will have cover for the following as you journey through multiple foreign destinations:

- Fees related to illness and injury

- Ambulance services

- Medical evacuation (where you can be brought back home if the hospital determines it’s necessary)

Travel insurance will offer coverage in the event that any of your personal belongings are lost, stolen, or misplaced. If your luggage is delayed, then you will be refunded up to the policy’s benefit limit so that you can purchase the essentials you will need until your luggage arrives. If your belongings are lost or stolen, then you will be reimbursed to replace the lost items.

Personal liability offers the policyholder protection in the event that he or she damages any property whilst in a foreign country. It can be used to cover the likes of rental car damage excess, to replace a third party’s belongings if you were responsible for losing or damaging them, and it can pay for legal fees in the scenario where you will need a lawyer.

Basically, travel insurance will give you the financial aid that you will need when you do not have the budget to cover any mishaps that “may” occur during your trip.

What Types of Travel Insurance Are Available?

With so many different reasons for traveling and with a seemingly endless number of destinations to travel to, insurance companies have adapted travel insurance policies so that they can accommodate the niche types of travel. This allows individuals to get the best form of cover for each trip.